info@biz4group.com

info@biz4group.com

Imagine a digital system that doesn’t wait for instructions but instead, understands your business goals, learns from real-time feedback, and takes independent actions to get the job done.

Read More

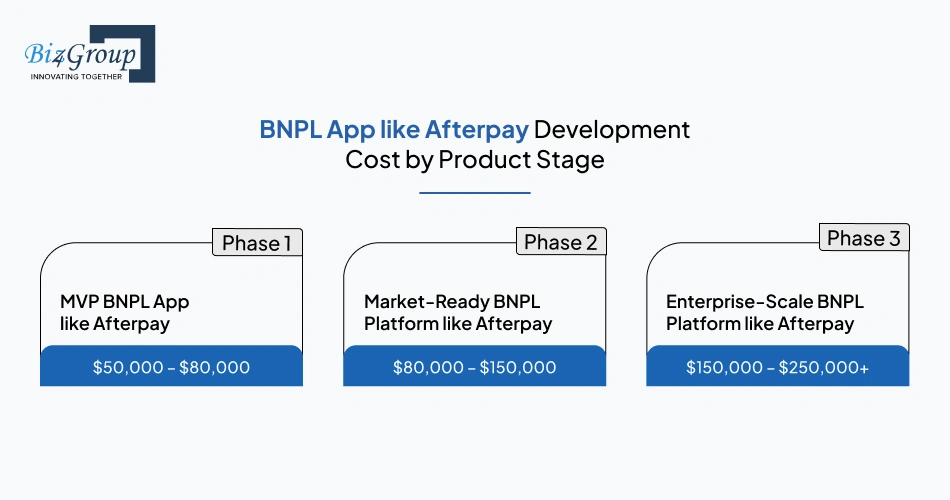

The Cost to Develop a BNPL App Like Afterpay usually ranges between $50,000 and $250,000+, depending on the product scope, feature set, compliance requirements, and backend infrastructure.

A simple MVP with basic installment payments and limited integrations costs much less than a full-scale BNPL platform with credit assessment, fraud detection, merchant dashboards, repayment automation, and financial reconciliation systems.

This is why the BNPL app development cost like Afterpay is often higher than standard payment or eCommerce apps. BNPL platforms do not just process transactions. They also manage lending workflows, risk evaluation, user verification, payment scheduling, and merchant settlements in real time.

Many founders researching the buy now pay later app development cost like Afterpay focus mainly on customer-facing features. In reality, a large part of the development budget goes into backend systems such as:

The cost of payment app development like Afterpay also depends on how the platform is built. Some startups choose custom development, while others reduce costs by using fintech APIs or white-label infrastructure for payments, identity verification, and risk management.

The growing use of AI in payments industry platforms is also changing how BNPL apps are developed. Many companies now use AI models for fraud detection, repayment prediction, and customer risk scoring, which adds another layer of technical complexity.

At the same time, scalability and compliance expectations across fintech products continue to rise, similar to what is happening in fintech in wealth management platforms.

This blog is for:

In this guide, we will break down:

The Cost to Develop a BNPL App Like Afterpay usually ranges from $50,000 to $250,000+, depending on the features, integrations, compliance requirements, and platform complexity.

A simple MVP with basic installment payments and limited integrations costs much less than a full-scale BNPL platform with credit assessment, fraud detection, merchant management, repayment automation, and financial reconciliation systems.

For most fintech startups, the BNPL app development cost like Afterpay depends on:

Many founders researching the buy now pay later app development cost like Afterpay often ask: we are building a Buy Now Pay Later app and need to estimate how much it costs to develop a scalable BNPL solution like Afterpay. In most cases, scalability requirements, repayment infrastructure, and compliance systems have a bigger impact on pricing than frontend app features alone.

Another common question businesses ask during budgeting is: I am looking to create a BNPL payment app like Afterpay and want to know the budget required for development. The answer usually depends on whether the product is being built as a lean MVP, a market-ready platform, or a large-scale enterprise BNPL ecosystem.

The buy now pay later app development cost like Afterpay changes based on the type of platform you want to build.

|

Development Stage |

Estimated Cost |

Typical Features |

Best For |

|---|---|---|---|

|

MVP BNPL App like Afterpay |

$50,000 – $80,000 |

User onboarding, installment payments, payment gateway integration, basic merchant dashboard |

Startups testing the market |

|

Market-Ready BNPL Platform like Afterpay |

$80,000 – $150,000 |

KYC/AML verification, fraud detection, merchant settlement, repayment tracking, analytics |

Fintech startups preparing for launch |

|

Enterprise-Scale BNPL Platform like Afterpay |

$150,000 – $250,000+ |

Advanced underwriting, AI-based fraud detection, financial reconciliation, multi-merchant infrastructure |

Large-scale fintech platforms |

An MVP focuses on launching core BNPL features quickly with lower development costs. A market-ready platform includes stronger compliance systems, merchant operations, and scalable backend infrastructure. Enterprise platforms require advanced risk management, real-time financial tracking, and high-volume transaction processing, which significantly increases the overall cost.

Many BNPL platforms now use AI models for fraud detection, repayment prediction, and automated risk scoring. As a result, demand for AI integration services in fintech products has increased, especially among startups building scalable lending infrastructure.

The cost of payment app development like Afterpay does not stop after launch. BNPL platforms require continuous spending on infrastructure, compliance, maintenance, and transaction monitoring.

Common monthly operational costs include:

Most startups spend between $5,000 and $30,000+ per month to maintain and scale a BNPL platform after launch. Some fintech startups outsource post-launch maintenance and infrastructure scaling to specialized engineering partners or a software development company in Florida with experience in payment systems and compliance-heavy applications.

Building a BNPL app like Afterpay is expensive because the platform combines payments, lending, compliance, risk management, and merchant operations in one system. Costs increase further when you add underwriting, fraud prevention, repayment automation, financial reconciliation, and real-time transaction monitoring.

A standard payment app mainly processes transactions. A BNPL platform also handles credit approval, installment repayment, merchant settlements, compliance workflows, and financial tracking.

Key areas that increase complexity include:

The buy now pay later app development cost like Afterpay increases because these systems must work together in real time without payment failures or reconciliation errors.

Founders researching BNPL infrastructure are effectively asking: we are exploring fintech payment solutions and want to know the cost of building a BNPL app with credit assessment and installment features. In most cases, underwriting systems and repayment infrastructure are among the largest contributors to development cost.

Many fintech startups also work with providers offering AI consulting services to improve fraud detection and repayment risk analysis in scalable BNPL platforms.

The largest share of the BNPL app development cost like Afterpay usually comes from backend infrastructure, integrations, and compliance systems rather than frontend design.

The biggest cost drivers include:

Costs increase further when companies want automation and predictive analytics features. Businesses that plan to integrate AI into an app for fraud analysis, repayment prediction, or customer risk scoring usually need additional engineering and infrastructure investment.

Business owners entering the lending space also commonly ask: I want to build a fintech lending app with installment payment features and need cost estimation for development. The answer usually depends on repayment workflows, compliance scope, underwriting complexity, and merchant integration requirements.

The development budget of BNPL app like Afterpay becomes significantly higher for enterprise-scale platforms handling large transaction volumes and multi-merchant operations.

Many estimates for the cost of payment app development like Afterpay only cover basic app development and ignore the infrastructure needed to run a real BNPL platform.

Most online estimates exclude:

This is why a basic MVP may cost around $50,000, while a scalable BNPL platform with compliance, risk management, and merchant infrastructure can exceed $250,000+.

Before estimating the building cost of BNPL app like Afterpay, founders should define the full platform scope, not just the mobile app features.

Reduce the Cost to Develop a BNPL App Like Afterpay with scalable fintech architecture and faster MVP execution.

Get a Custom Cost EstimateThe development approach you choose has a major impact on the cost, scalability, launch timeline, and long-term flexibility of a BNPL platform. Startups building a Buy Now Pay Later app like Afterpay usually choose between three options: custom development, API-based infrastructure, or white-label solutions.

The right development model depends on your budget, product goals, compliance strategy, and technical requirements.

|

Approach |

Estimated Cost |

Development Speed |

Customization Level |

Best For |

|---|---|---|---|---|

|

White-Label BNPL Platform like Afterpay |

$50,000 – $80,000 |

Fast |

Low |

Startups launching quickly with limited customization |

|

API-Based BNPL Development like Afterpay |

$80,000 – $150,000 |

Moderate |

Medium to High |

Fintech startups needing flexibility without building core infrastructure from scratch |

|

Custom BNPL Development like Afterpay |

$150,000 – $250,000+ |

Slow |

Very High |

Businesses building fully scalable and proprietary BNPL ecosystems |

White-label platforms reduce the initial development budget of BNPL app like Afterpay, but they also limit customization and infrastructure control. API-based development offers a balance between speed and flexibility by using third-party services for payments, KYC, underwriting, or fraud prevention. Fully custom development provides the most control, but it also requires the highest investment and engineering effort.

Some startups planning to build AI fintech app capabilities into their BNPL platform prefer API-based or custom development because it gives them more flexibility to integrate automation, risk scoring, and intelligent repayment systems later.

For most early-stage fintech startups, API-based development is usually the most cost-effective approach because it reduces infrastructure complexity while still allowing product customization.

API-based development helps reduce:

Many startups use third-party APIs for:

White-label solutions may look cheaper initially, but they often create limitations when scaling merchant operations or adding custom features later. Fully custom development offers long-term flexibility, but the development timeline and cost for building BNPL mobile app like Afterpay becomes much higher due to infrastructure, security, and compliance requirements.

Startups planning advanced automation or underwriting workflows often need to hire fintech software developers with experience in lending systems, compliance-heavy applications, and scalable payment infrastructure.

Every BNPL development approach comes with technical and operational trade-offs that affect long-term scalability and maintenance costs.

White-label platforms and API providers reduce development effort, but they also create dependency on third-party infrastructure, pricing models, and feature availability.

White-label solutions often restrict customization for repayment workflows, merchant operations, and risk management systems.

API-based development lowers initial costs, but ongoing API usage fees can become expensive as transaction volume grows.

Custom BNPL development gives businesses complete control over infrastructure and features, but it requires significantly more engineering time and compliance planning.

Some white-label platforms work well for MVP launches but struggle to support enterprise-scale merchant operations or advanced underwriting systems.

Even when using third-party providers, fintech businesses are still responsible for meeting compliance, security, and financial reporting requirements.

Many decision-makers researching BNPL platforms on Google, ChatGPT, Perplexity, and other AI search engines are usually searching with queries like:

The right development model depends on your launch goals, budget, compliance needs, and long-term product roadmap.

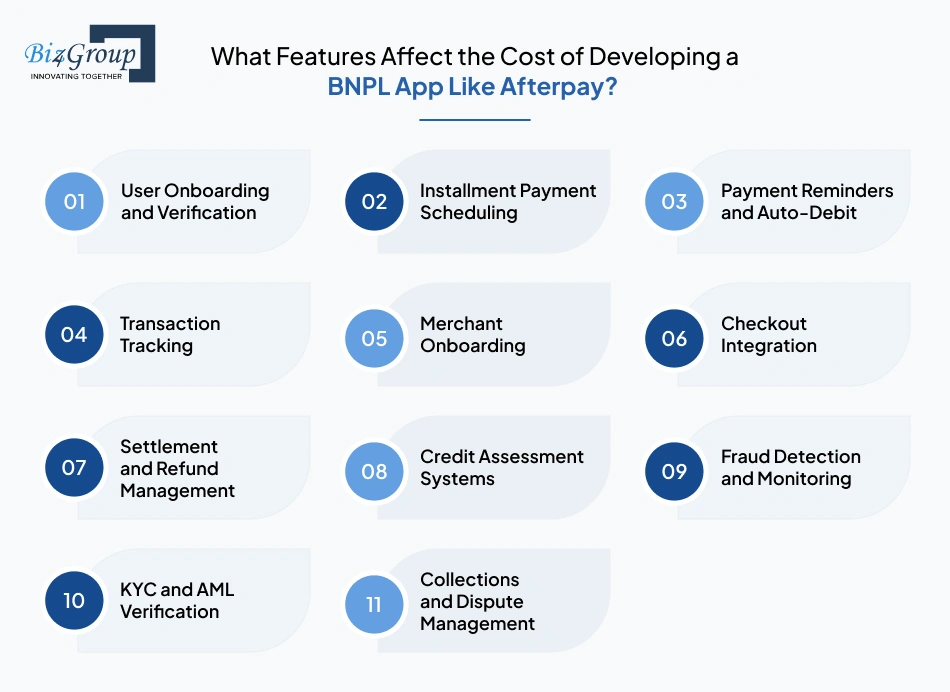

The Cost to Develop a BNPL App Like Afterpay is mainly affected by three feature groups: consumer app features, merchant infrastructure, and risk and compliance systems. Features related to underwriting, fraud detection, repayment automation, and merchant settlement usually add the highest development and infrastructure costs.

Consumer-facing features define the core user experience and repayment flow inside a BNPL platform. The complexity of onboarding, repayment automation, and transaction handling can significantly increase the BNPL app development cost like Afterpay.

|

Feature |

Purpose |

Cost Impact |

|---|---|---|

|

User Onboarding and Verification |

Registers users and validates identity through KYC workflows |

Medium to High |

|

Installment Payment Scheduling |

Splits purchases into multiple repayments |

Medium |

|

Payment Reminders and Auto-Debit |

Automates repayment notifications and recurring payments |

Medium |

|

Transaction Tracking |

Displays repayment history, balances, and transaction details |

Low to Medium |

User onboarding becomes more expensive when the platform supports identity verification, banking integrations, biometric authentication, or advanced compliance checks. Repayment automation also requires backend logic for failed payments, retries, and repayment tracking across multiple billing cycles.

Some startups exploring the buy now pay later app development cost like Afterpay also evaluate whether to add conversational support or repayment assistance features inspired by common use cases of AI chatbot in banking and financial services.

Consumer-side workflows directly affect customer retention, repayment success rates, and support overhead.

Merchant-side infrastructure increases the building cost of BNPL app like Afterpay because the platform must support checkout integrations, settlements, refunds, and merchant operations at scale.

|

Feature |

Purpose |

Cost Impact |

|---|---|---|

|

Merchant Onboarding |

Registers and manages merchant accounts |

Medium |

|

Checkout Integration |

Embeds BNPL payment options into merchant checkout flows |

High |

|

Settlement and Refund Management |

Handles merchant payouts, refunds, and repayment adjustments |

High |

Checkout integration is often one of the most time-consuming parts of development because the BNPL system must work reliably across multiple payment environments, APIs, and eCommerce platforms.

Settlement infrastructure adds another layer of complexity because the platform needs to track repayments, merchant payouts, refunds, and transaction adjustments without reconciliation errors.

Some businesses estimating the development budget of BNPL app like Afterpay also compare whether to build internal merchant tools or partner with teams specializing in AI model development for merchant analytics and repayment behavior forecasting.

Merchant infrastructure becomes increasingly expensive as transaction volume and partner integrations grow.

Risk management and compliance systems are among the most expensive components of BNPL app development because they directly impact lending operations, fraud prevention, and regulatory compliance.

|

Feature |

Purpose |

Cost Impact |

|---|---|---|

|

Credit Assessment Systems |

Evaluates customer eligibility and repayment risk |

High |

|

Fraud Detection and Monitoring |

Detects suspicious transactions and repayment behavior |

High |

|

KYC and AML Verification |

Verifies identity and ensures regulatory compliance |

High |

|

Collections and Dispute Management |

Handles failed payments, disputes, and recovery workflows |

Medium to High |

Afterpay clone app development cost increases significantly when businesses build custom underwriting systems or real-time transaction monitoring infrastructure. Compliance systems also require secure data storage, audit logging, and reporting capabilities.

As the platform scales, admin and risk systems usually require continuous upgrades to support larger transaction volumes, stricter compliance requirements, and more advanced fraud patterns.

The Cost to Develop a BNPL App Like Afterpay is usually spread across multiple stages, including planning, design, frontend development, backend infrastructure, integrations, compliance systems, testing, and deployment. Backend systems and compliance infrastructure often consume a larger share of the budget than the mobile app itself.

Here’s a step by step breakdown of building BNPL app like Afterpay with cost estimation:

|

Development Stage |

Estimated Cost Range |

What’s Included |

|---|---|---|

|

Product Discovery and Technical Planning |

$5,000 – $15,000 |

Product roadmap, feature planning, architecture decisions, compliance scope |

|

UI/UX Design |

$5,000 – $20,000 |

User flows, wireframes, onboarding design, repayment experience, merchant dashboards |

|

Mobile App Development |

$15,000 – $50,000 |

iOS/Android app development, repayment workflows, notifications, transaction tracking |

|

Backend Infrastructure and APIs |

$20,000 – $70,000 |

APIs, databases, repayment logic, merchant systems, cloud infrastructure |

|

Payment Gateway and Banking Integrations |

$10,000 – $30,000 |

Payment processing, banking APIs, settlement systems, transaction handling |

|

Risk Engine and Compliance Systems |

$15,000 – $50,000 |

KYC/AML verification, fraud monitoring, underwriting systems, audit logging |

|

QA Testing, Security Audits, and Deployment |

$5,000 – $20,000 |

Functional testing, penetration testing, bug fixes, cloud deployment |

Development costs are usually highest during backend infrastructure, payment integration, and compliance implementation stages. For most fintech startups, these areas have a bigger impact on the final BNPL app development cost like Afterpay than the mobile app itself.

Some companies that develop BNPL apps like Afterpay in USA in a budget also delay advanced capabilities such as fraud intelligence, automation, or enterprise AI solutions until after the MVP launch to reduce initial development costs.

Portfolio Spotlight

Worth Advisors is a modern financial planning platform built to simplify advisor-client collaboration through smart questionnaires, modular financial reports, data integrations, and centralized planning workflows. The platform reflects the kind of secure financial infrastructure, data handling, and scalable fintech architecture also required when developing a BNPL app like Afterpay, especially for platforms managing sensitive user data and transaction-heavy operations.

Businesses using scalable repayment and settlement systems can improve operational efficiency by up to 40%.

Start Building Your BNPL Platform

Several technical and operational decisions can significantly increase or reduce the cost of building a BNPL app like Afterpay. The biggest cost factors usually include compliance requirements, underwriting complexity, merchant integrations, infrastructure scalability, and the type of development team involved.

Hiring a US-based fintech development team usually costs more than working with offshore developers, but experienced fintech engineers can reduce risks related to compliance, security, and scalability. Many startups evaluating the BNPL app development cost like Afterpay also compare in-house hiring with outsourcing to fintech-focused development agencies.

Native development for iOS and Android provides better platform optimization but increases development time and cost. Cross-platform frameworks help reduce the initial building cost of BNPL app like Afterpay by allowing shared codebases across devices.

KYC, AML, PCI DSS, audit logging, and secure financial data handling all increase the buy now pay later app development cost like Afterpay. Compliance implementation becomes more expensive when the platform operates across multiple regions or financial jurisdictions.

Some BNPL platforms use basic eligibility rules, while others build custom underwriting systems with behavioral scoring and transaction risk analysis. Businesses planning advanced lending automation often evaluate future AI fintech app development cost requirements during this stage.

Integrating with a few merchants is relatively straightforward, but supporting large merchant ecosystems requires more complex checkout infrastructure, settlement workflows, refund handling, and operational management systems.

Platforms designed for high transaction volume usually require stronger database architecture, monitoring systems, and scalable backend infrastructure from the beginning. Some fintech startups also plan future automation capabilities early when they expect to hire AI developers for product expansion later.

For most fintech startups, backend systems, compliance infrastructure, and merchant operations are the biggest factors affecting long-term development cost.

Underwriting and financial reconciliation are some of the most expensive parts of building a BNPL app like Afterpay because they manage lending decisions, repayment tracking, merchant payouts, and financial accuracy in real time.

Credit assessment systems decide whether a user is eligible for installment payments and how much risk the platform can take during checkout.

These systems usually handle:

The buy now pay later app development cost like Afterpay increases when businesses build custom underwriting systems instead of using third-party risk providers.

Some fintech startups also add predictive scoring models to improve approval decisions and reduce repayment risk over time.

BNPL platforms need to track repayments, merchant payouts, refunds, failed transactions, and balance updates without errors.

The system must:

As transaction volume grows, the backend infrastructure becomes more complex and expensive to maintain. Similar financial tracking challenges also exist in money transfer app development, where transaction accuracy is critical.

Even small reconciliation errors can affect merchant payouts, repayment balances, and reporting accuracy.

Many startups reduce the building cost of BNPL app like Afterpay by using third-party APIs for credit checks, fraud detection, identity verification, and transaction monitoring.

Third-party APIs help reduce:

These APIs are commonly used for:

Some startups use external APIs during the MVP stage and move to custom underwriting systems later as the platform scales. For early-stage fintech products, third-party APIs are usually the fastest and most cost-effective way to launch a BNPL platform.

Plan the buy now pay later app development cost like Afterpay with the right APIs, compliance systems, and backend architecture.

Schedule a Product Consultation

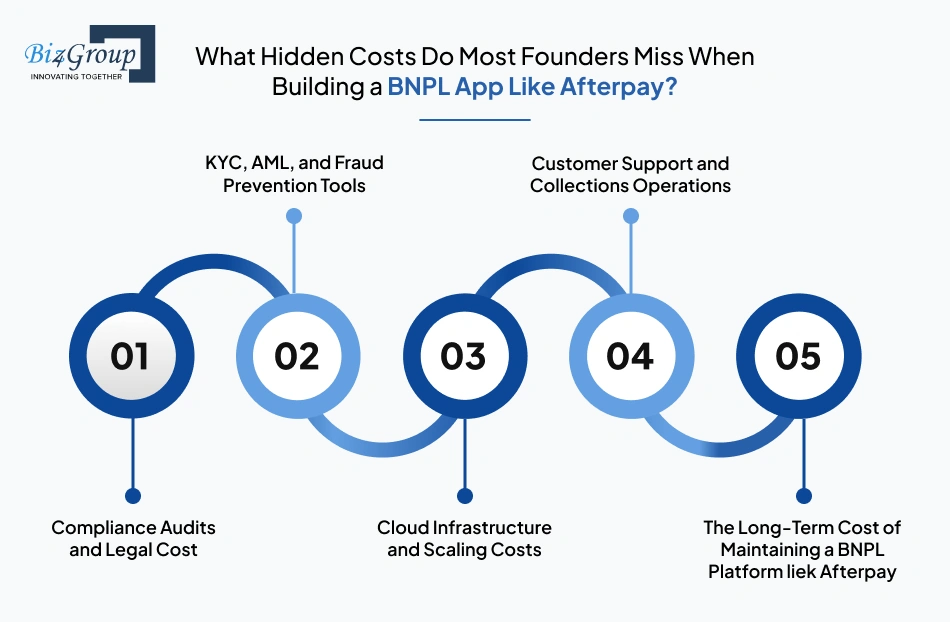

Many founders underestimate recurring expenses such as compliance audits, KYC and AML verification fees, fraud monitoring tools, cloud infrastructure, customer support operations, and long-term platform maintenance. These hidden costs can significantly increase the total cost of running a BNPL platform after launch.

BNPL platforms must comply with lending regulations, financial reporting requirements, and data security standards. Legal reviews, compliance audits, policy updates, and documentation reviews create recurring operational costs even after the product goes live.

Identity verification, fraud monitoring, and transaction screening tools usually work on usage-based pricing models. As transaction volume increases, API costs for KYC, AML, and fraud prevention systems increase as well.

Many founders also underestimate the operational workload created by repayment disputes, failed transactions, and user verification issues once the platform starts scaling.

The building cost of BNPL app like Afterpay continues increasing as transaction volume, merchant integrations, and repayment activity grow. Higher platform usage leads to larger cloud hosting, storage, database, monitoring, and infrastructure management expenses.

Some fintech startups eventually explore broader business app development using AI strategies to reduce operational dependency and improve platform efficiency as repayment operations become more complex.

BNPL platforms require dedicated support and collections workflows to handle repayment delays, disputes, failed auto-debits, refund requests, and chargebacks.

Support costs usually grow faster than expected because installment-based products generate ongoing customer interactions throughout the repayment cycle rather than only during checkout.

Post-launch maintenance includes infrastructure upgrades, security patches, API maintenance, compliance updates, bug fixes, and feature improvements.

Some fintech businesses also invest in automation and conversational workflows over time to improve repayment communication and operational efficiency, especially as products begin scaling across larger merchant ecosystems or regions through tools similar to an AI conversation app.

For many fintech startups, long-term operational expenses eventually become just as important as the initial BNPL app development cost like Afterpay.

Choosing the right development company affects the quality, scalability, compliance readiness, and long-term cost of a BNPL platform. Building a BNPL app like Afterpay requires experience with payment systems, lending workflows, financial compliance, and backend infrastructure.

Before hiring a fintech development company, founders should check whether the team has experience building payment or lending products.

Key questions to ask include:

Many development agencies claim fintech expertise, but very few have experience building repayment systems and financial reconciliation infrastructure.

The market has also expanded in recent years, with several top AI development companies in Florida moving into fintech and payment software development.

Development location affects pricing, communication, delivery workflows, and technical quality.

|

Factor |

US-Based Teams |

Offshore Teams |

|---|---|---|

|

Development Cost |

Higher |

Lower |

|

Fintech Compliance Experience |

Usually Stronger |

Depends on Vendor |

|

Communication |

Easier Collaboration |

May Need More Coordination |

|

Development Speed |

Moderate |

Moderate to Fast |

|

Infrastructure Planning |

Usually More Mature |

Depends on Experience |

|

Long-Term Support |

Easier to Manage |

Vendor-Dependent |

US-based teams usually charge more, but they often have better experience with financial regulations and payment infrastructure. Offshore teams can reduce the initial BNPL app development cost like Afterpay, but the final product quality depends heavily on the vendor’s fintech experience.

Most of the founders evaluating BNPL vendors usually carry out searches on ChatGPT, Perplexity, ang Gemini, with highly practical concerns such as:

These questions usually come down to three things: whether the team understands fintech compliance, whether they can build scalable repayment infrastructure, and whether the project scope aligns with the available budget.

For businesses looking for wealth management software solutions, with a strong balance of fintech expertise, scalable engineering, and long-term product support for BNPL platforms, Biz4Group LLC is a great choice.

Key advantages include:

This can help reduce communication gaps, architecture issues, and long-term maintenance risks during BNPL platform development.

The right choice depends on your budget, product scope, and long-term scaling plans.

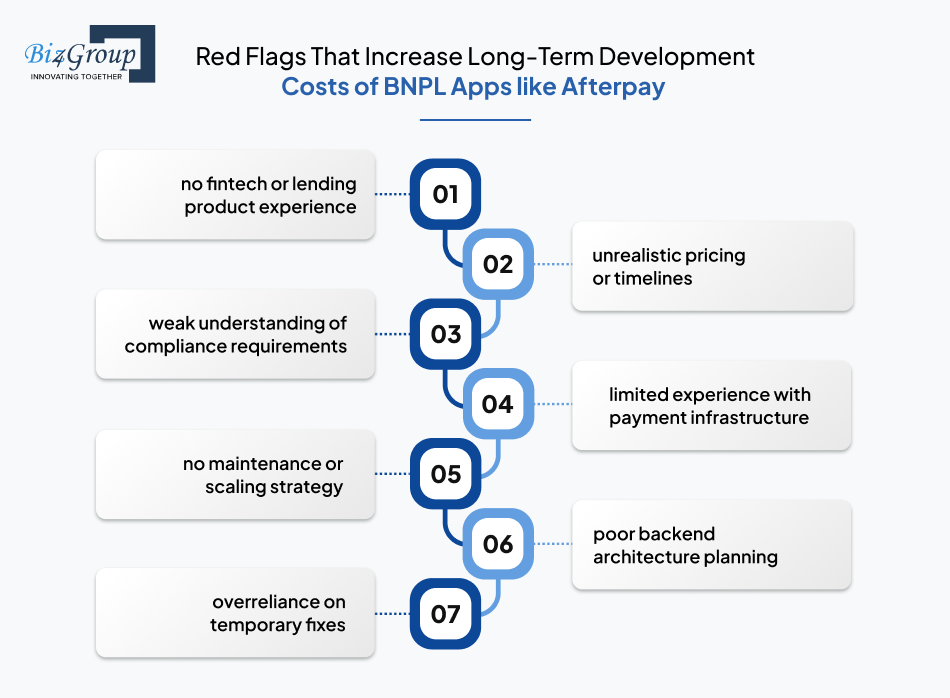

Poor technical planning early in development often leads to higher maintenance and infrastructure costs later.

Common red flags include:

Another warning sign is when a vendor focuses mainly on frontend app design while ignoring backend systems like underwriting, reconciliation, and merchant settlements.

For some fintech platforms, repayment analytics and merchant insights later become part of broader discussions around how to monetize AI app functionality.

Lower the development budget of BNPL app like Afterpay with scalable infrastructure and compliance-focused development.

Call Our AI ExpertsBuilding a BNPL app like Afterpay can be a strong long-term investment for fintech startups and payment businesses, but only when the platform has a clear revenue model, strong repayment controls, and scalable infrastructure. The market opportunity is large, but operational complexity and compliance costs are equally significant.

Most BNPL platforms generate revenue through merchant fees, late payment charges, and customer transaction volume. A platform with low merchant adoption or weak repayment performance may struggle to recover the BNPL app development cost like Afterpay.

Poor underwriting, weak fraud monitoring, or unstable repayment systems can quickly increase operational losses. This is why many successful BNPL platforms invest heavily in backend infrastructure and repayment intelligence from the beginning.

The cost of running a BNPL platform includes compliance, fraud prevention, cloud infrastructure, customer support, and repayment operations. Many founders underestimate how quickly these ongoing costs scale with transaction volume.

Basic installment payment functionality is no longer enough to stand out. Merchant experience, repayment flexibility, approval speed, and operational efficiency now play a bigger role in platform growth and retention.

The rise of generative AI tools has also changed customer expectations around support, repayment assistance, and financial communication workflows.

A simple MVP may work for early validation, but scaling a BNPL platform requires reliable backend systems, compliance infrastructure, and transaction monitoring from the beginning.

In some fintech ecosystems, repayment automation and collections workflows are also becoming part of broader discussions around AI agent implementation inside financial operations.

For startups with a clear business model and realistic infrastructure planning, building a BNPL platform can become a scalable long-term fintech business rather than just a payment feature.

Building a BNPL app like Afterpay is not just about adding installment payments to a mobile app. It involves lending infrastructure, repayment systems, compliance workflows, merchant operations, fraud prevention, and scalable backend architecture, all working together without breaking under transaction pressure.

For most businesses, the real challenge is not understanding the starting cost. It is understanding what happens after launch, when infrastructure, compliance, support operations, and scaling requirements start growing faster than expected.

That said, the opportunity is still significant for businesses with the right product strategy, technical planning, and operational model. Whether you start with a lean MVP or a full-scale platform, choosing the right architecture and development approach early can save a lot of expensive headaches later. Nobody enjoys debugging repayment logic at 2 AM.

Working with an experienced custom software development company can help reduce technical risks, improve scalability planning, and speed up development timelines. And as fintech platforms continue evolving, many businesses also look for ways to build AI software for repayment automation, fraud monitoring, analytics, and operational efficiency inside modern BNPL ecosystems.

Planning to build a scalable BNPL app like Afterpay? Let’s discuss your feature scope, timeline, and development budget.

The Cost to Develop a BNPL App Like Afterpay usually ranges between $50,000 and $250,000+, depending on the platform complexity, integrations, compliance requirements, and scalability goals. A basic MVP costs much less than an enterprise-grade BNPL platform with underwriting, fraud detection, and merchant settlement infrastructure.

Yes, some BNPL platforms use alternative risk assessment methods instead of traditional credit bureau checks. These may include transaction history, repayment behavior, banking data, and spending patterns. However, relying only on internal scoring models can increase lending risk during early-stage operations.

One of the biggest challenges is maintaining accurate repayment tracking and financial reconciliation at scale. BNPL platforms must continuously manage installments, refunds, merchant payouts, and transaction records without inconsistencies.

Yes, many fintech startups begin with a smaller MVP that focuses on core installment payment workflows, basic onboarding, and payment integrations. Advanced features such as custom underwriting, fraud intelligence, and large-scale merchant operations are often added later.

Most BNPL apps use automated repayment retries, payment reminders, late fee workflows, collections systems, and customer support processes to handle failed payments. Some platforms also temporarily reduce spending limits or pause future transactions until repayments are resolved.

Not always. Some platforms manage merchant operations through web dashboards or admin portals instead of dedicated mobile apps. The decision usually depends on merchant onboarding volume, reporting needs, and operational complexity.

with Biz4Group today!

Our website require some cookies to function properly. Read our privacy policy to know more.