info@biz4group.com

info@biz4group.com

Imagine a digital system that doesn’t wait for instructions but instead, understands your business goals, learns from real-time feedback, and takes independent actions to get the job done.

Read More

Have you ever wondered why perfectly valid transactions sometimes get declined? Or how fraudsters manage to slip through when current rules-based systems flag everything under the sun? For many fintech leaders and decision-makers, those questions have become operational headaches on a routine basis.

The reality is that the industry is at a tipping point. The move from legacy payment workflows to AI in payments is no longer optional, it is essential for staying competitive. And the numbers prove it:

In this blog you’ll get to explore about:

Businesses leaders aren’t tackling this shift alone. Some are partnering with an AI development company to embed intelligence directly into their payment flows. Others are rethinking the entire infrastructure with the help of a custom software development company, building platforms that can adapt as quickly as customer expectations evolve.

The future of payments will not be defined by transactions alone, but by intelligence woven into every interaction. Through innovations in Agentic AI Development, financial systems are evolving to anticipate user needs, enhance trust, and personalize engagement at scale. Those who move first will set the bar for trust, speed, and customer experience in the years ahead.

For years, payments ran on rules: approve this, decline that, flag anything that looked unusual. It worked until digital commerce exploded. Today, payments happen in milliseconds across borders and currencies. Fraudsters have grown smarter, customers expect instant approvals, and businesses are bleeding revenue from false declines and failed transactions.

This is where AI in payments steps in. At its core, it is the use of artificial intelligence in digital payments to make smarter, faster, and more adaptive decisions. Instead of relying on static rules, AI systems learn from millions of data points such as purchase history, device patterns, and location to decide whether a transaction is safe, how to route it for success, and how to make the process seamless for the customer.

For business leaders, the value lies in outcomes:

Organizations investing in enterprise AI solutions are already discovering how these capabilities can redefine their payment workflows, cut costs, and deliver a smoother customer experience at scale.

Legacy payment systems were designed for a slower era of commerce, and today they show their limits. Rules-based fraud checks block legitimate customers, manual reviews drain resources, and rigid infrastructures fail to keep up with the speed and scale of modern transactions.

In contrast, AI in payments adapts in real time, learning from patterns to approve genuine purchases, stop fraud instantly, and deliver experiences that feel effortless to customers. Here are the key differences between the two types:

|

Area |

Legacy Digital Payments |

AI in Payments |

|

Fraud Detection |

Rules-based systems that miss new attack patterns |

Adaptive fraud prevention that learns and evolves with every transaction |

|

Customer Experience |

High false decline rates leading to frustration and churn |

Smarter approvals that keep genuine customers happy and loyal |

|

Operational Efficiency |

Manual reviews that slow down teams |

Automated, real-time decision-making powered by AI automation services |

|

Personalization |

One-size-fits-all checkout flows |

Tailored experiences and recommendations driven by insights |

|

Scalability |

Struggles as transaction volumes increase |

Seamlessly handles millions of transactions without compromising speed |

The contrast is clear: legacy systems create friction while AI in payments creates opportunity. And to fully understand that opportunity, it helps to look at how AI actually works inside a payment flow.

Read More: AI Money Transfer App Development—The Complete Guide

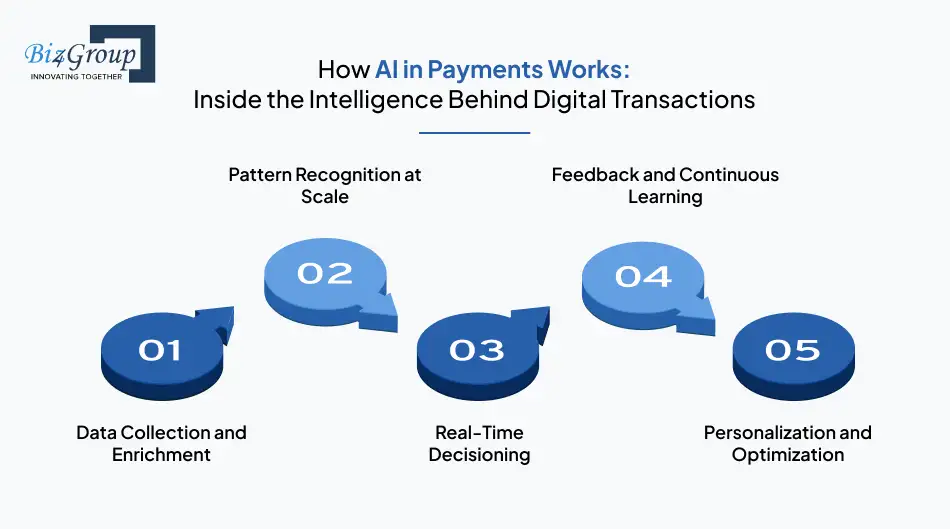

AI in payments is not magic, it is method. Behind every instant approval or fraud block is a set of intelligent steps that transform raw transaction data into real-time business decisions. Understanding this flow matters, not to become a data scientist, but to see how artificial intelligence in payments creates measurable business impact.

How it works, step by step:

Every tap, swipe, and click generates signals such as purchase history, device details, location, and time of day. AI systems capture and enrich these data points to form a 360-degree view of each transaction.

Instead of static rules, machine learning models identify patterns across millions of transactions. They distinguish normal customer behavior from suspicious activity in ways traditional systems could never match.

Within milliseconds, the system approves, declines, or flags a payment. The outcome is not random, it is based on continuously updated models that keep fraud out while maximizing successful payments.

AI in payments does not stand still. Every transaction outcome feeds back into the system, making the models sharper over time and helping businesses stay one step ahead of emerging threats.

Beyond fraud prevention, AI enhances customer experience by tailoring checkout flows, recommending preferred payment methods, and optimizing routing to lower transaction costs.

This workflow often requires more than technology alone. Many enterprises bring in AI consulting services to ensure the models, compliance, and business outcomes align seamlessly.

By demystifying how AI in payments actually works, it becomes easier to see why enterprises across industries are leaning into it. And the best way to illustrate its value is to look at how companies are already applying these capabilities in real-world scenarios.

Unlock the potential of AI in payments with smarter fraud detection, speed, and customer-first design.

Start My AI Journey

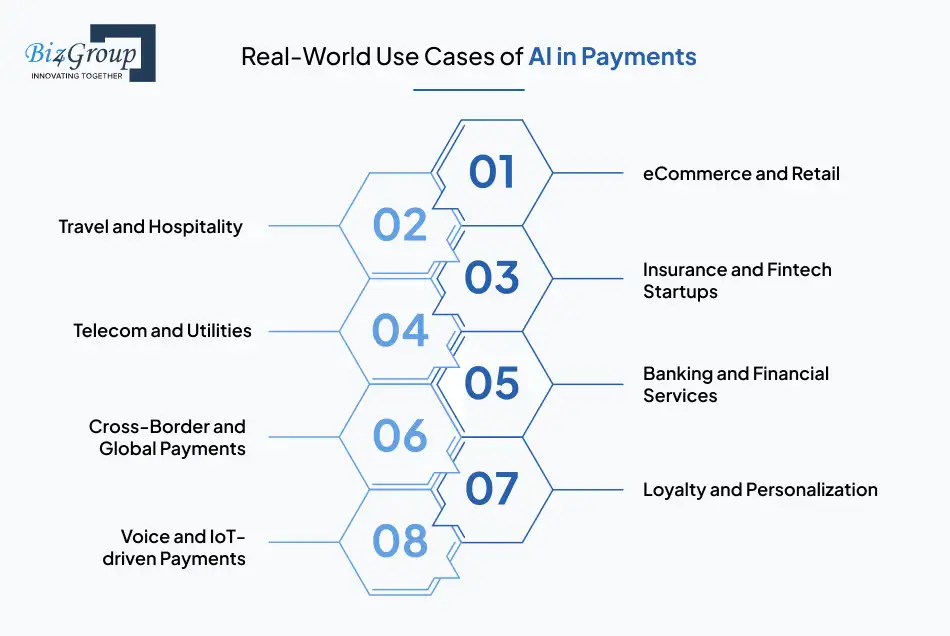

Fraud and failed transactions cost businesses billions, while customers expect payments to be instant and seamless. This is why leaders across industries are turning to AI in payments to secure operations, improve efficiency, and deliver experiences that build loyalty and trust.

Online retailers leverage AI in payment gateways to reduce false declines, optimize routing, and create frictionless checkout flows. This improves approval rates while also enabling personalized offers that keep customers engaged and reduce costly cart abandonment issues across global markets.

Also Read: How does a payment gateway work in the eCommerce sector?

The travel sector faces high cross-border payment risks and complex fraud challenges. AI secures bookings, streamlines international transactions, and powers conversational payment interfaces, ensuring customers enjoy seamless journeys while enterprises protect margins in a highly competitive industry.

Also Read: AI-based Hospitality Software Development

AI validates claims, spots fraudulent activity, and reduces reliance on manual reviews, helping insurers cut operational costs. AI in fintech startups enables secure, scalable payment systems that can handle rapid growth while keeping expenses predictable and customer trust intact.

Telecom and utility companies run on recurring billing, where payment failures drive churn. AI predicts defaults before they happen, retries payments intelligently, and improves collection efficiency, ensuring predictable cash flow and better customer satisfaction across subscription-driven models.

Also Read: Role of AI in Telecommunication

AI in banking and payments automates fraud detection, compliance checks, and dynamic credit scoring at scale. By analyzing millions of data points in real time, banks reduce fraud-related losses, speed up approvals, and maintain stronger compliance without sacrificing customer experience.

Also Read: 7 Ways AI Chatbot Can Improve Banking and Financial Services

International payments are complex, expensive, and prone to fraud. AI helps businesses minimize FX losses, route transactions through the most cost-effective corridors, and secure international transactions, giving enterprises the confidence to expand globally without unnecessary financial risk.

AI transforms payments into a strategic tool by personalizing rewards, checkout experiences, and recommendations. Instead of being just a backend process, payments become part of retention and growth strategies that encourage repeat purchases and deepen customer engagement.

With smart devices and voice assistants, payments are moving into everyday conversations. AI ensures these transactions remain secure and frictionless, whether it is paying through a car dashboard, a wearable device, or a virtual assistant at home.

These examples show that AI in payments is already far beyond theory. It is powering real solutions across industries, improving security, efficiency, and customer loyalty. Next, let's find out how to adopt AI in payments strategically within the organizations.

AI is enabling payments in places where people never expected. From gaming platforms to social apps and smart IoT devices, AI-driven payment systems make transactions faster, safer, and seamless. Embedded payments in non-fintech apps is one of those places.

Key benefits of AI-powered embedded payments:

|

Industry |

Example |

AI Application |

|

Gaming |

In-game purchases |

Predictive spend analytics, instant fraud checks |

|

Social Media |

Peer-to-peer transfers |

Behavioral pattern recognition, automated alerts |

|

IoT Devices |

Smart home purchases |

Edge AI for instant authorization |

Insight: Businesses integrating AI in non-fintech apps often see higher engagement and revenue because payments feel effortless and secure.

Generative AI transforms raw payment data into insights you can act on immediately. It reduces manual work and provides a strategic view across transactions.

Applications include:

Example: A retail platform can use generative AI to detect users likely to abandon carts, then automatically suggest personalized offers. This can improve conversions by 15–20%.

Generative AI moves businesses from reactive to proactive decision-making, improving speed, accuracy, and insight quality.

Microtransactions and loyalty programs handle high volumes of low-value interactions. AI helps automate, personalize, and optimize these processes without overwhelming operations.

Dynamic AI approaches include:

With AI, loyalty programs move beyond static point systems into intelligent, personalized ecosystems, driving better results for both users and businesses.

AI in payments sounds exciting on paper, but adoption is rarely plug-and-play. Leaders have to ask the tough questions: where will AI make the biggest impact, how can it be rolled out responsibly, and what mix of people and technology will make it work? A clear roadmap keeps the process from becoming an expensive experiment and turns it into a real driver of growth.

Every company has a weak spot in its payments stack. For some it is high fraud losses, for others it is endless manual reviews or compliance headaches. Pinpointing these issues first ensures AI is applied where it actually moves the needle.

The learning curve for AI in banking and payments is steep, and getting regulations wrong can be costly. Partnering with experienced teams through AI consulting services brings clarity on compliance, architecture, and measurable outcomes right from day one.

Rolling out AI doesn’t have to mean ripping out existing systems. A smarter approach is piloting AI in one area, like fraud detection or transaction routing, proving its value, and then expanding. This builds confidence without overwhelming the organization.

Even the best AI model will fail if no one knows how to manage it. Bringing in the right people, whether you upskill internally or hire AI developers, ensures your systems keep improving instead of stagnating after launch.

AI works best when it strengthens what is already in place. Businesses that carefully integrate AI into an app or core platform avoid disruption, while still gaining the performance and security benefits customers now expect.

AI in payments is never “done.” Fraudsters evolve, regulations shift, and customer expectations rise. Setting up ongoing measurement and feedback loops makes sure your AI stays sharp and continues delivering value quarter after quarter.

Adoption is really about building confidence step by step. Once those basics are in place, the next question becomes: how do you actually design and integrate AI-enabled payment systems so they work at scale?

AI in payments is shaping the future, position your business at the forefront of this transformation.

Get Started With AI in Payments

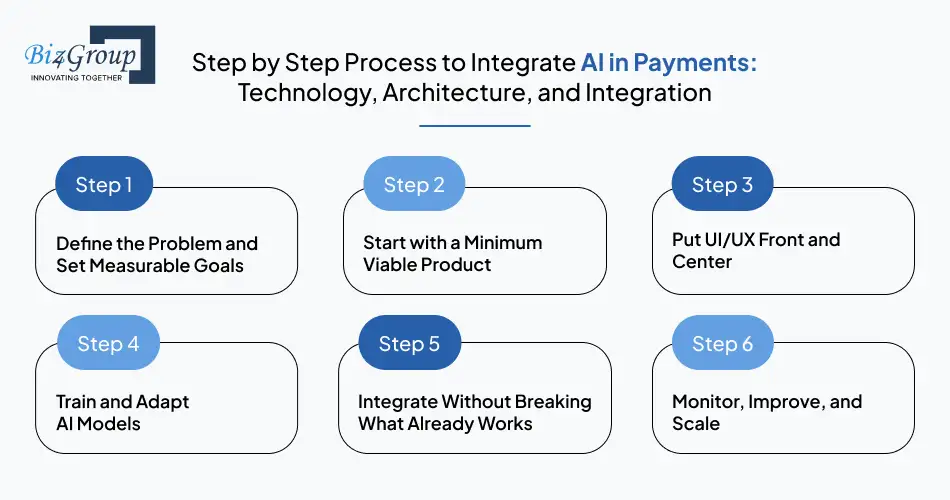

Integrating AI into payments isn’t about throwing tech buzzwords at a problem. It’s about carefully weaving intelligence into systems that millions of people already rely on daily. For business leaders, the real challenge isn’t the code, it’s making sure the rollout drives adoption, compliance, and trust without derailing existing operations. If you want to see how this connects with broader applications, here’s a useful guide:

AI isn’t a magic button. It only works when tied to specific pain points, whether that’s reducing chargebacks, improving fraud detection, or cutting down on false declines. Clear goals help your teams and partners know what “success” actually looks like.

Rolling out AI across your entire payments system is risky and expensive. A smarter move is starting with MVP services, a small, testable version focused on one priority use case like fraud alerts or payment routing.

Also read: Top 12+ MVP Development Companies in USA

Even the smartest payment engine will fail if customers find it clunky. A smooth, intuitive interface from checkout to authentication is what builds trust. That’s where strong UI/UX design experts comes in.

Also read: Top UI/UX design companies in USA

For those wondering about how to train AI models plugging in an algorithm is easy, but keeping it relevant is hard. AI models for payments must be trained on diverse datasets and regularly updated to spot new fraud tactics or spending behaviors. Without this, accuracy drops quickly.

Payments are mission-critical and disruption is not an option. AI needs to sit alongside existing infrastructure, not replace it overnight. Smart integration means layering intelligence onto current gateways and banking systems without slowing them down.

Also Read: Software Testing Companies in USA

Integration doesn’t end at launch. Fraud tactics, customer habits, and compliance rules keep shifting, which means your AI must keep learning. Ongoing monitoring and improvements are what turn AI into a long-term advantage instead of a one-off project.

When businesses take this approach, AI integration in payments feels less like a risky leap and more like a steady climb. Having said that, now it’s time for us to explore the tech stack that you need for building AI capabilities in your payment platform.

If you are deciding where to invest this quarter, it helps to know what actually makes AI in payments work. The winning stacks are practical, secure, and designed for scale. Below are the building blocks that turn artificial intelligence in digital payments from slideware into outcomes:

Classification, anomaly detection, and ensembles score risk in milliseconds. They learn from live outcomes, cutting false declines without opening the door to fraud. This is the engine room for approval lift and loss reduction.

NLP powers dispute chats, refunds, and subscription changes that feel human. It routes intent, summarizes conversations, and speeds resolutions. Thoughtful flows, backed by solid AI assistant app design, reduce handle time and frustration.

Also Read: NLP vs LLM: Choosing the Right Approach for Your AI Strategy

Signals from device, behavior, and history are turned into “what happens next.” Teams forecast chargebacks, payment failures, and cash-flow dips. Decisions shift from reactive fire drills to proactive prevention.

AI only adds value when it snaps cleanly into gateways, cores, and CRMs. Modern APIs orchestrate risk checks, routing, and post-decision workflows. The result is smart AI platforms with AIaaS intelligence without disrupting what already works.

Elastic compute keeps peak traffic smooth and audits tidy. Cloud services support regional data residency and policy controls. That means scale for holiday spikes without sacrificing latency or compliance.

For settlement and reconciliation, shared ledgers remove blind spots between parties. Smart contracts automate release conditions and dispute logic. Transparency improves trust while cutting manual reconciliation cycles.

PANs and PII are replaced with tokens, then protected end to end. Hardware security and key rotation limit blast radius if something goes wrong. Security by design keeps AI in banking and payments audit-ready.

Face, fingerprint, or FIDO-based flows reduce checkout friction. Strong signals feed risk engines without training customers to accept weak security. Better UX and fewer step-ups mean higher conversion.

Lightweight models score risk on the device for speed-critical moments. You cut round trips, preserve privacy, and keep approvals snappy. It is a smart fit for mobile-first markets and high-volume apps.

Versioning, monitoring, and drift alerts keep models honest. Feature stores and automated retraining prevent quiet accuracy decay. Governance aligns AI in payment gateways with policy and regulator expectations.

Since we now know about the ideal technologies that can be used to power your payment systems with AI, it’s time to focus on cost related aspects.

When it comes to integrating AI in payments, the price tag can range anywhere between $10,000 and $100,000. That’s not a random number, it’s a ballpark figure influenced by scope, complexity, and the scale at which your business wants to roll out AI. For decision-makers, the cost is less about sticker shock and more about understanding what you’re paying for, and how it ties back to long-term value.

|

Project Scope |

What It Covers |

Estimated Cost Range |

|

MVP (Minimum Viable Product) |

Basic fraud detection, limited personalization, and core payment processing features. Perfect for testing market fit before scaling. |

$10,000 – $30,000 |

|

Mid-Level Solution |

Advanced fraud analytics, predictive insights, chatbots for customer support, and integration with existing systems. Balanced for SMEs and growing enterprises. |

$30,000 – $60,000 |

|

Enterprise-Grade Solution |

End-to-end AI integration with payment gateways, compliance automation, custom models, and multi-channel customer experiences. Built for scale. |

$60,000 – $100,000+ |

It’s important to remember that cost is a strategic investment. Companies that approach AI in payments as part of their business app development using AI can unlock efficiencies that far outweigh the initial spend.

For those who seek more details regarding the cost aspect, it's recommended that you check out our blog on AI integration cost.

The next big focus is making sure it stands strong against regulatory and compliance demands.

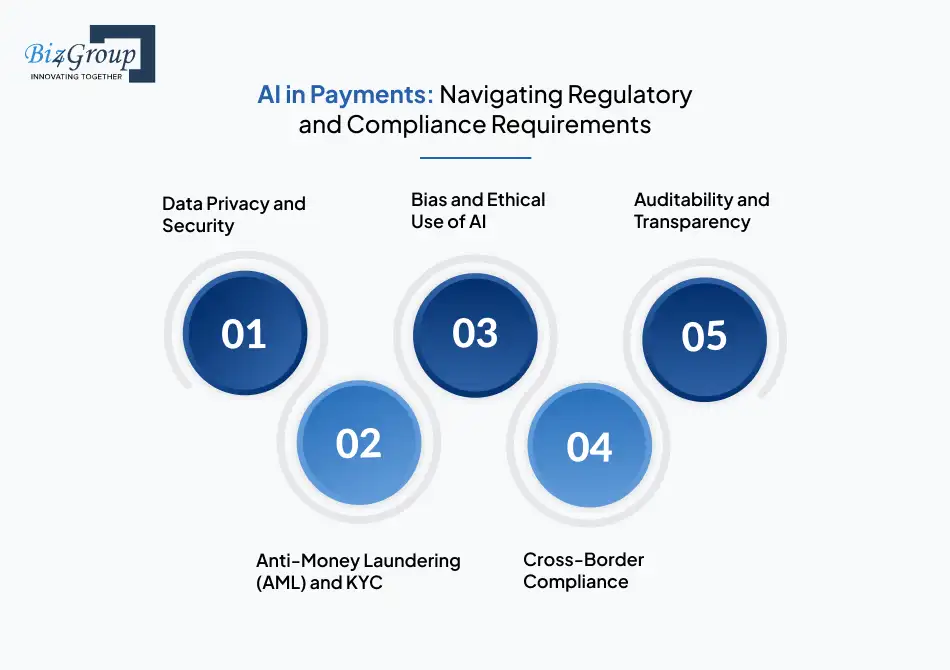

AI in payments doesn’t just make transactions faster, it changes how financial data is collected, analyzed, and stored. That’s where the pressure comes in. Regulators expect companies to innovate responsibly, and customers expect their trust not to be misplaced. For leaders, the balancing act is adopting AI without stumbling into avoidable compliance issues.

Every payment involves sensitive information, and once AI enters the picture, the data volume only grows. Laws like GDPR and CCPA aren’t optional hurdles; they’re the ground rules. During AI model development, leaders need to make sure data is anonymized, encrypted, and handled transparently if they want to keep regulators and customers on their side.

AI can spot patterns humans miss, but regulators will ask: how reliable is it, and can you show your work when questioned? That’s why teams often partner with firms skilled in AI integration services to ensure compliance is embedded at the system level, not bolted on later. AML case management is a key part of tying compliance workflows together, and tools like SEON demonstrate how structured monitoring and reporting of suspicious activity can support both anti-money laundering efforts and broader regulatory adherence without bogging down transaction flows.

If your AI model unfairly blocks payments or approves the wrong ones, regulators won’t look kindly on it. Bias is more than a technical flaw, it’s a compliance and reputation risk. Ethical design has to be part of the strategy from day one, whether you’re refining fraud checks or experimenting with generative AI for customer-facing payment features.

Expanding payments globally adds complexity. What’s acceptable in one country may not fly in another. Integrating AI in payments means designing flexible systems that adapt to local standards without slowing down international transactions.

Regulators want transparency, not black boxes. If a system declines a transaction, someone needs to explain why. AI models that leave a clear audit trail make those conversations easier and keep regulators confident. The added benefit: auditability also gives internal teams the assurance that their systems are working as intended.

Tackling compliance head-on keeps innovation sustainable. And once the rules of the road are clear, the next question for leaders becomes: how do you handle the risks that come with AI in payments while keeping its benefits intact?

Enhance customer confidence with AI-driven security and personalized experiences in digital transactions.

Secure My Payment SystemsAI in payments promises speed, accuracy, and scale, but it also brings challenges leaders can’t afford to ignore. The good news is that with the right strategies, these risks can be managed effectively, turning potential roadblocks into opportunities for building resilience:

|

Common Risks in AI Payments |

How to Prevent Them |

|

Algorithmic Bias - AI models may unintentionally discriminate, leading to unfair transaction declines and reputational damage. |

Work with a trusted AI chatbot development company to ensure regular audits, diverse training datasets, and ethical design to minimize bias. |

|

Over-Reliance on Automation - Fully automated systems can misjudge edge cases, leading to false declines or missed fraud signals. |

Maintain a human-in-the-loop approach where critical transactions are reviewed manually, supported by AI-driven insights. |

|

Regulatory Non-Compliance - Failure to meet standards like GDPR, PSD2, or CCPA can lead to fines and trust erosion. |

Embed compliance into AI system design, with transparent audit trails and ongoing alignment with evolving regulations. |

|

Security Vulnerabilities - AI systems that process massive datasets are prime targets for cyberattacks. |

Use encryption, secure APIs, and continuous monitoring to safeguard sensitive payment data. Regular penetration testing strengthens resilience. |

|

Scalability Issues – Models that work in pilots may fail under peak transaction volumes, slowing down payments. |

Stress-test AI systems before rollout and invest in scalable cloud infrastructure that adapts to demand spikes. |

|

Customer Trust Risks – Lack of transparency in why payments are approved or denied can frustrate users. |

Adopt explainable AI techniques and clear communication strategies that help customers understand decisions without jargon. |

AI in payments is powerful, but unchecked risks can undermine its benefits. Leaders who treat risk mitigation as part of their strategy, not an afterthought, will find themselves building stronger and more trusted systems. From here, the conversation naturally shifts to best practices that ensure implementation delivers consistent value at scale.

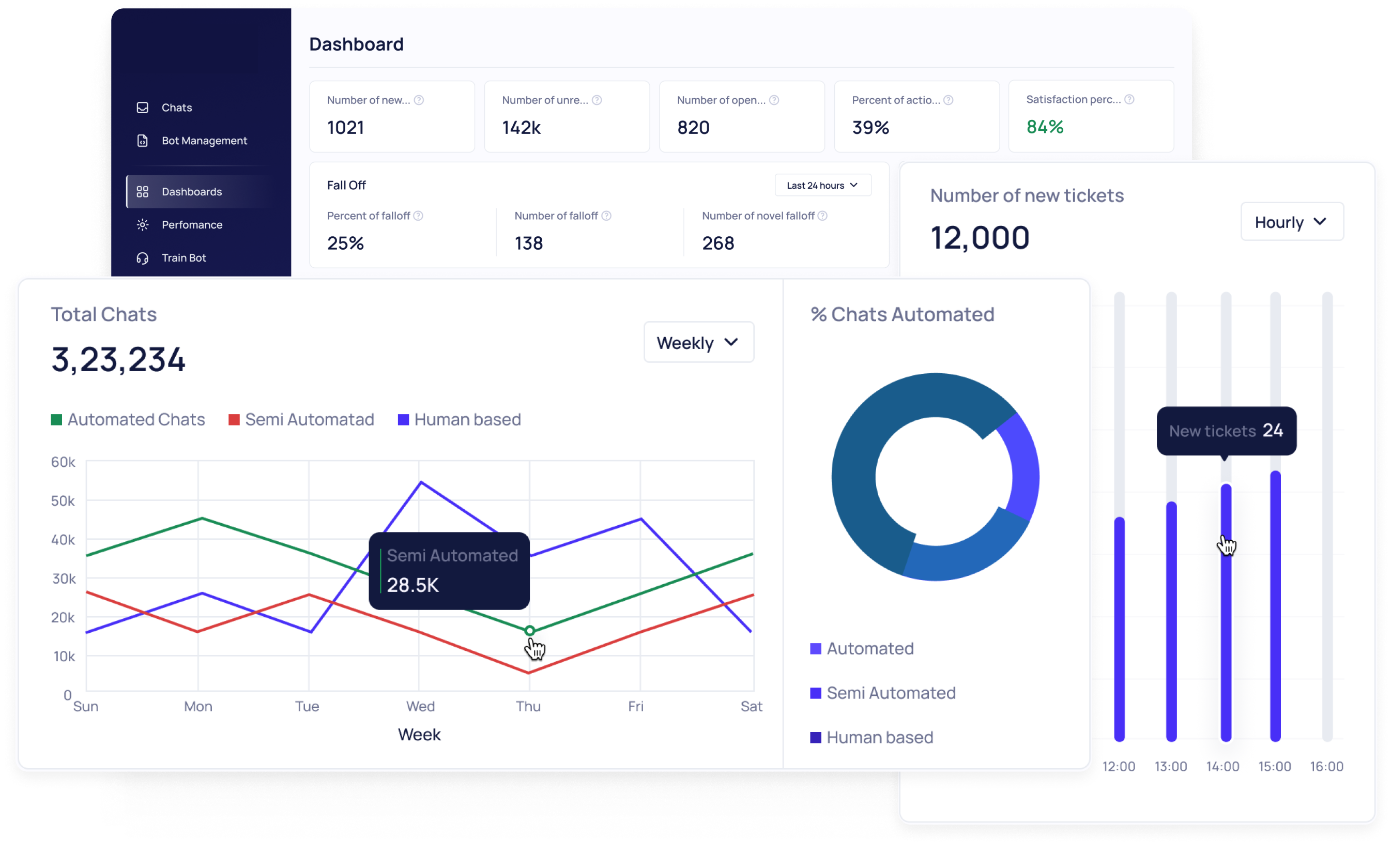

AI in payments is not just a technology upgrade. It delivers measurable results across operations, customer experience, and business performance. Understanding the impact helps organizations optimize investments and achieve strategic advantages.

AI automates payment processing, reduces manual work, and minimizes errors. Metrics like transaction speed, failed payment reduction, and lower manual review requirements help businesses measure efficiency. Organizations using AI often see substantial savings in time and operational costs.

AI improves personalization and creates smoother payment flows. Tracking customer retention, transaction completion, and complaint rates allows businesses to see how AI enhances satisfaction. Faster processing and tailored recommendations build trust and encourage repeat usage.

Continuous monitoring of AI models ensures ongoing value. Metrics such as fraud detection accuracy, revenue impact, and performance across different business units provide insight into ROI. Benchmarking highlights strengths and areas for optimization.

AI in payments achieves maximum value when efficiency, customer experience, and performance tracking are measured and optimized. Businesses that quantify results can refine AI models, scale effectively, and maintain leadership in digital payments.

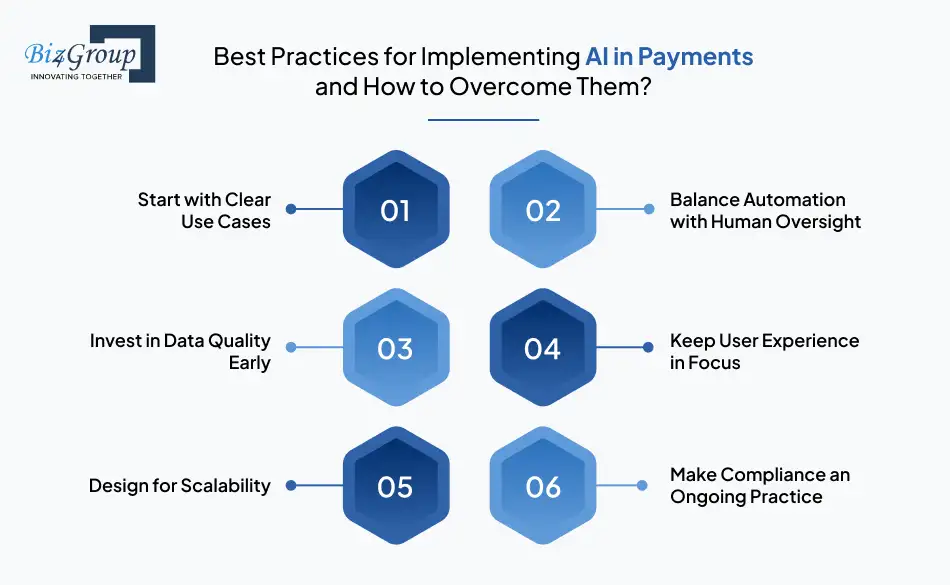

AI in payments is not about quick wins but about building systems that can stand the test of scale, regulation, and customer expectations. Here are the best practices that help you avoid costly setbacks and unlock sustainable value for your business:

Instead of deploying AI everywhere, focus on areas where it makes the biggest impact, such as fraud detection or payment personalization. Prioritizing sharp, measurable goals ensures resources are aligned with outcomes that matter to the business.

AI can catch fraud in milliseconds, but human judgment is still critical for complex or high-risk cases. A hybrid approach builds both efficiency and accountability, giving regulators and customers confidence in the system.

Bad data leads to flawed decisions, no matter how advanced the model. Collecting, cleaning, and enriching datasets should be treated as an upfront investment that powers long-term accuracy and fairness in AI-driven payments.

The smartest system fails if it frustrates customers. Frictionless checkout, clear communication, and even conversational features like an AI conversation app create trust, adoption, and repeat usage.

AI in payments must handle today’s volumes and tomorrow’s growth. Building flexible architecture with cloud-ready components allows organizations to scale smoothly while maintaining speed and reliability under pressure.

Treat regulatory alignment as a continuous effort, not a one-time project. Regular audits, explainability in models, and transparent reporting keep systems compliant while reducing risks of fines or customer trust issues.

The real advantage comes when these best practices turn into habits across the organization. And once the foundation is strong, the next hurdle to overcome is tackling the practical challenges businesses face during AI adoption in payments.

Transform payment insights into business value with AI-powered analytics and predictive intelligence.

Adopt AI in PaymentsThe biggest barriers often lie in the existing infrastructure, the people who need to adapt, and the resources required to make it all work. Addressing these challenges directly can mean the difference between a stalled initiative and a future-ready payment system:

|

Common Challenges |

How to Solve Them |

|

Legacy System Integration |

Older payment infrastructures rarely welcome AI easily. Using modular APIs and modern architecture can smooth the shift, and partnering with a trusted software development company in Florida helps avoid patchwork fixes. |

|

Change Management Resistance |

Teams used to traditional workflows often resist AI. Running small pilot projects, offering clear training, and showing how AI reduces workloads helps employees embrace the change instead of fearing it. |

|

High Implementation Costs |

Upfront investment is often a sticking point. Leaders can reduce pushback by focusing on high-impact use cases like fraud detection first, proving ROI before scaling across the payment ecosystem. |

|

Talent Shortage |

The right mix of AI and payments expertise is rare. Upskilling internal teams while bringing in specialized talent or external partners can bridge the gap and build long-term capability. |

|

Customer Education |

Customers may distrust AI decisions if they don’t understand them. Clear explanations, user-friendly interfaces, and conversational tools like an AI conversation app can ease concerns and improve adoption. |

|

Enterprise Adoption Speed |

Large organizations often move slower due to layers of approval and risk-aversion. Breaking projects into phases and aligning stakeholders early helps avoid delays. |

Organizations that anticipate these hurdles are better prepared to lead, not follow, in the payments industry. Now let’s talk about the emerging AI trends that will define the next chapter of global payments.

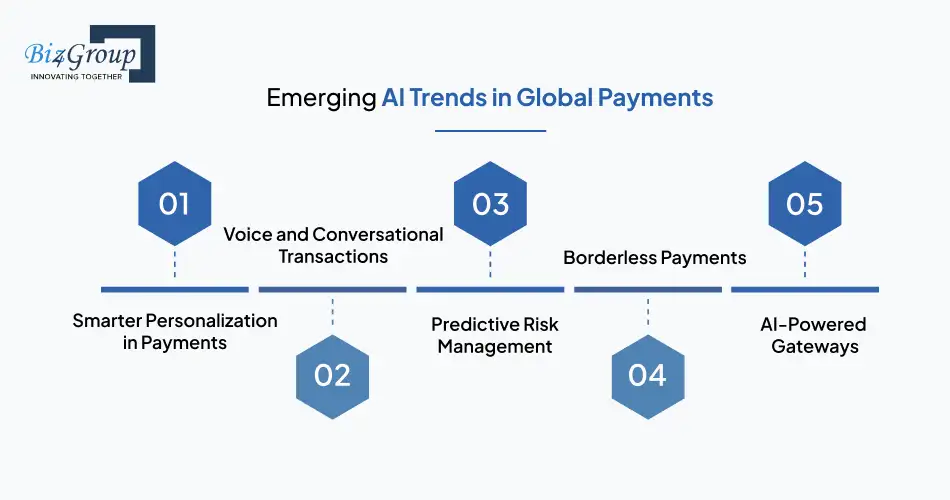

When you look at the payments industry today, one thing stands out - AI is now setting the pace for how money moves. For business leaders, this isn’t about chasing hype. It’s about recognizing the shifts that will separate tomorrow’s winners from everyone else:

AI is moving beyond fraud alerts into shaping how payments feel for the end user. Checkout pages, offers, and even credit approvals are increasingly tailored in real time, creating journeys that feel designed for each individual.

Payments are becoming more human. Whether through smart speakers or chat-based checkout, customers are starting to authorize payments naturally. Advances in AI assistant app design are making this shift more intuitive and widely accepted.

Also Read: AI Voice Chatbot Development

Instead of waiting for fraud to happen, AI systems are now trained to anticipate unusual behavior before it turns into a problem via predictive analytics. That means fewer false declines and stronger protection for both businesses and customers.

Global commerce often stalls at regulations, exchange rates, and delays. AI is helping payment systems adapt on the fly, ensuring that international transactions are faster, cheaper, and less complicated for merchants.

Payment gateways are being rebuilt as intelligence hubs, not just transaction pass-throughs. With AI embedded, they’re evolving into platforms that provide insights, flag risks, and even suggest growth opportunities.

The leaders who stay ahead aren’t the ones tracking AI in payments from a distance, but the ones already aligning operations to ride these shifts as they accelerate.

AI is transforming payments, but automation brings new responsibilities. Ethical practices and risk management are essential to keep AI systems trustworthy, fair, and compliant. Businesses need clear strategies to manage AI decisions while protecting users and operations.

AI models assign risk scores to transactions. Explainable AI ensures that every score can be understood by humans and regulators.

|

Metric |

Before AI |

After AI |

Change |

|

Fraud Detection Accuracy |

82% |

94% |

+12% |

|

Manual Review Time |

10 min |

4 min |

-60% |

|

False Positives |

7% |

2% |

-5% |

This transparency builds confidence in AI decisions and supports regulatory compliance.

Example: A global payment platform discovered geographic bias in approvals. Retraining the AI on a balanced dataset reduced unnecessary declines by 18 percent, improving user satisfaction and fairness.

Reducing bias ensures AI decisions are fair, reliable, and compliant.

Ethical oversight is ongoing. Businesses should:

Tip: Audit logs and alerts make AI actions transparent, accountable, and aligned with business goals.

Ethical AI and strong risk management create a reliable payment ecosystem. Companies that monitor AI, prevent bias, and maintain oversight reduce risks and strengthen customer trust.

When it comes to AI in payments, the real question leaders ask is simple: who can deliver solutions that actually work in high-stakes, customer-facing environments? At Biz4Group, we’ve built products that prove we understand both the technology and the business outcomes that matter. That experience is exactly what makes us a strong partner for enterprises ready to embrace AI-driven payments.

One of the solutions we’re most proud of is an AI chatbot for human-like communication that handles refunds, payment resolutions, and subscription plan changes. By replicating human-like communication, the chatbot shows how AI can smooth out interactions that often frustrate users. In the payments space, that same intelligence translates to fewer disputes, faster resolutions, and stronger relationships with customers.

Biz4Group’s value lies in turning AI from a concept into a working solution that fits seamlessly into business operations. For leaders exploring AI in payments, partnering with an AI app development company like ours means tapping into a team that has already built intelligent systems designed to handle complexity with clarity.

Design Payments That Customers Love

Seamlessly integrate AI into your apps and payment flows for experiences that win loyalty.

Enhance My Payment Experience

AI in payments isn’t just about speeding up transactions; it is redefining how businesses earn customer trust and stay competitive. From predictive fraud checks to smoother global transactions, the change is happening right now. The real decision for leaders isn’t whether to adopt AI, but how quickly they are ready to move.

At Biz4Group, our focus is on building AI that actually delivers value, not just hype. Whether it’s helping you build AI software from the ground up or supporting you as an AI product development company, we specialize in turning complex challenges into scalable solutions.

So as AI continues to transform payments, how far ahead you want to be when everyone else gets on board?

Let’s Talk Payments + AI: See how Biz4Group can help your business make the shift today.

AI in payments can increase trust by making transactions more secure, reducing false declines, and giving customers quicker resolutions to disputes. The more transparent and seamless the process, the more loyalty businesses can build.

Not entirely. While AI automates fraud detection, personalization, and transaction monitoring, human oversight remains critical for complex edge cases, regulatory reviews, and customer disputes. The future is a hybrid of AI speed with human judgment.

AI in payments is valuable across industries, but the biggest impact is in eCommerce, banking, insurance, travel, and telecommunications—sectors with high transaction volumes and a need for fraud prevention and personalized customer journeys.

Yes. By automating fraud detection, compliance checks, and dispute resolution, AI cuts down manual work and operational overhead. It also minimizes revenue leakage caused by false declines, which directly improves margins.

Smaller organizations often struggle with integration costs, lack of in-house AI expertise, and uncertainty around compliance. Starting with scalable, modular solutions helps them adopt AI without the risk of overinvestment.

Payment gateways are evolving into intelligent platforms that not only process transactions but also predict fraud, offer customer insights, and personalize experiences. AI-driven gateways will shift from being a utility to becoming a strategic growth enabler.

with Biz4Group today!

Our website require some cookies to function properly. Read our privacy policy to know more.