info@biz4group.com

info@biz4group.com

Imagine a digital system that doesn’t wait for instructions but instead, understands your business goals, learns from real-time feedback, and takes independent actions to get the job done.

Read More

Fintech startups looking to build an AI wealth management app in 2026 are entering a market that no longer rewards generic robo-advisor products. Users now expect conversational financial guidance, personalized portfolio intelligence, and real-time decision support instead of static ETF allocation tools. That shift is creating new opportunities for founders, CTOs, and product teams exploring AI wealth platforms for the US market.

But building a serious wealthtech product is far more complicated than attaching an LLM to an investment dashboard.

Teams trying to launch modern AI financial platforms must think through portfolio logic, compliance workflows, AI hallucination risk, auditability, human oversight, and SEC exposure from the beginning. This is especially true in fintech in wealth management, where personalized investment recommendations can quickly move a product into regulated territory.

The good news is that infrastructure barriers are lower than they were even a few years ago. APIs for brokerage access, KYC verification, custody, portfolio execution, and open banking now make it possible to develop AI wealth management app for fintech startups without building every financial system internally. Modern platforms increasingly combine conversational AI, portfolio rebalancing algorithms, machine learning wealth management systems, and retrieval-grounded financial workflows into a single product experience.

This broader AI transformation is also influencing adjacent sectors like the AI in payments industry, where fintech companies are redesigning customer interaction, fraud monitoring, and financial automation around AI-native workflows.

This guide is written specifically for:

Through this guide, you will learn:

Yes, but not for another generic robo-advisor.

The biggest opportunity in 2026 is building personalized wealth platforms for users that traditional advisors and older robo-advisors still fail to serve properly. Most legacy platforms automated investing. New AI-native products are competing on financial guidance, personalization, and real-time decision support.

That shift is creating strong opportunities in fintech startup wealth management, especially for founders building products around user behavior instead of only portfolio allocation.

“I am a startup founder who has been inspired by the success of companies like Betterment and Wealthfront but I believe there is a significant market opportunity for an AI wealth management app that serves specific underserved demographics with more personalized investment strategies and I need to understand the complete development requirements regulatory obligations and capital requirements before pursuing this opportunity?”

That question is becoming more common because the infrastructure required for wealth management app development for startups is now far easier to access. Startups no longer need to build every financial system internally to launch AI-powered wealth products.

Most robo-advisors were designed for scale, not personalization. They automated investing efficiently, but many still struggle to support users with different financial habits, goals, and communication preferences.

Some of the largest underserved segments include:

This is one reason many startups now build AI fintech app platforms focused on engagement and financial guidance instead of passive portfolio management alone.

The opportunity is no longer just better investing automation. It is building financial products that users actually want to interact with regularly.

Over the next two decades, trillions of dollars will move from older generations to younger investors. Traditional wealth firms were not built for how younger users manage money today. Many younger investors:

This creates strong demand for an AI investment app for millennials that combines investing, financial planning, and personalized support inside one experience.

The next generation of wealth platforms will likely compete more on user experience and guidance quality than on portfolio allocation alone.

Large wealth firms still dominate brand trust and assets under management. Smaller startups compete by moving faster and focusing on problems incumbents solve poorly.

Most traditional platforms focus heavily on portfolio performance. Few help users improve long-term financial behavior or decision-making consistency.

Startups can target specific groups such as freelancers, startup employees, creators, or younger investors instead of competing for the entire retail investing market.

Many incumbents are still layering AI features onto older systems. Startups can build around conversational workflows, AI agent implementation, and adaptive financial planning from the beginning.

Smaller teams can test onboarding flows, recommendation systems, and personalization features much faster than large financial institutions. This is where experienced teams offering AI consulting services can help reduce development mistakes early.

Modern wealth apps increasingly combine investing, budgeting, savings, tax planning, and payments into one experience. Similar shifts are also happening in embedded finance and money transfer app development.

The market is still open for startups that understand how modern users want financial products to behave. The strongest opportunities now come from building systems that feel intelligent, adaptive, and easier to trust than traditional robo-advisors.

Traditional robo-advisors mainly automate investing using fixed portfolio rules and risk questionnaires. An AI financial advisor app does much more. It combines personalized financial guidance, conversational support, portfolio insights, and real-time recommendations inside one platform. The main difference is that AI-native wealth apps are designed for ongoing interaction, not just automated investing.

Traditional robo-advisors focus mainly on automating portfolio allocation. AI-native wealth platforms focus on helping users make better financial decisions continuously.

|

Traditional Robo-Advisor |

AI Wealth Management App |

|---|---|

|

Fixed onboarding questionnaires |

Dynamic risk profiling |

|

Portfolio-focused experience |

Financial guidance + portfolio insights |

|

Rule-based investing |

AI-assisted personalization |

|

Limited interaction |

Conversational financial support |

|

Periodic updates |

Real-time monitoring and recommendations |

|

Reactive investing tools |

Proactive financial insights |

This is why many startups are now investing in AI robo advisor app development instead of traditional robo products. The market is shifting from passive investing tools to intelligent financial platforms users interact with regularly.

A chatbot answers questions after the user asks something. Agentic AI systems monitor financial activity, identify changes, and trigger actions automatically.

|

AI Chatbot |

Agentic AI Wealth System |

|---|---|

|

Responds to prompts |

Initiates actions automatically |

|

Handles isolated questions |

Manages multi-step workflows |

|

Limited context memory |

Tracks ongoing financial context |

|

Mainly informational |

Decision-support oriented |

|

Static interactions |

Adaptive workflow execution |

For example, a chatbot may explain why a portfolio dropped in value. An agentic system may detect unusual portfolio drift, identify tax-loss harvesting opportunities, and recommend rebalancing automatically.

This shift is becoming a major part of AI driven wealth management app platform development, especially for startups building adaptive financial products around long-term user engagement. Many teams also use AI integration services to connect AI systems with brokerage APIs, recommendation engines, and financial data infrastructure.

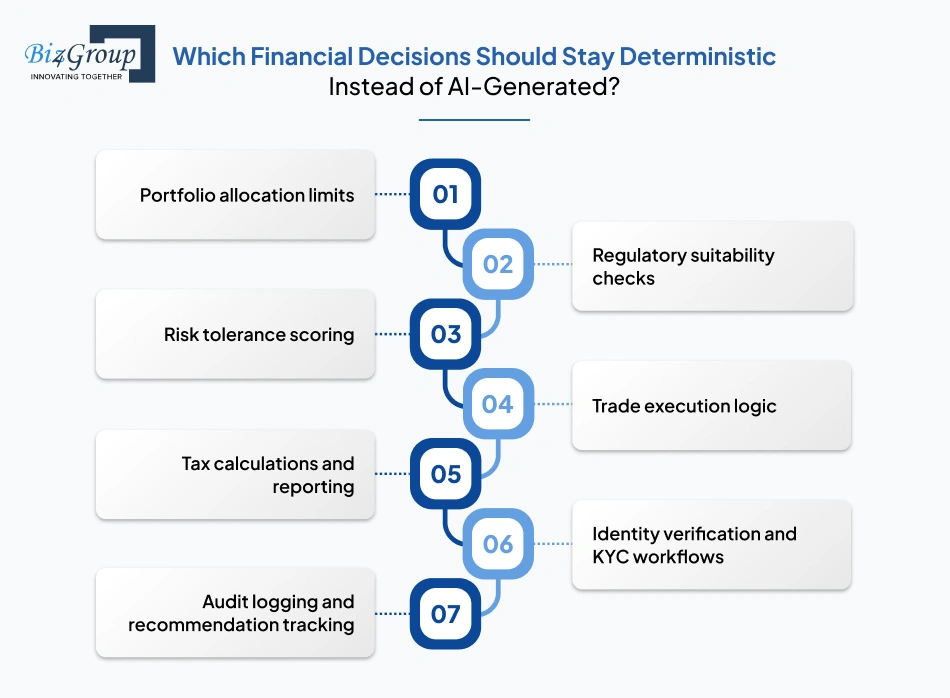

Not every financial process should rely on AI-generated decisions. Some areas still require fixed rules and deterministic logic to reduce compliance and operational risk.

The following functions should usually remain deterministic:

Many startups entering AI financial advisory app development make the mistake of using generative AI in areas where consistency and explainability matter more than flexibility.

This is one reason companies often hire fintech software developers with experience in both AI systems and financial infrastructure instead of relying only on general AI engineering teams.

The strongest AI wealth platforms combine AI-driven personalization with rule-based financial systems instead of replacing core financial logic completely.

Portfolio Spotlight

Worth Advisors is a modern financial planning platform built to simplify how advisors collect client information, generate reports, and manage investment planning workflows. The platform combines smart questionnaires, modular financial reporting, and financial data integrations to reduce manual operational overhead for advisors. Projects like this reflect how AI wealth management platforms are increasingly moving beyond simple robo-advising into scalable, workflow-driven financial guidance systems.

Build a scalable AI wealth management app with personalized guidance, portfolio intelligence, and compliance-ready infrastructure.

Start Your WealthTech Project

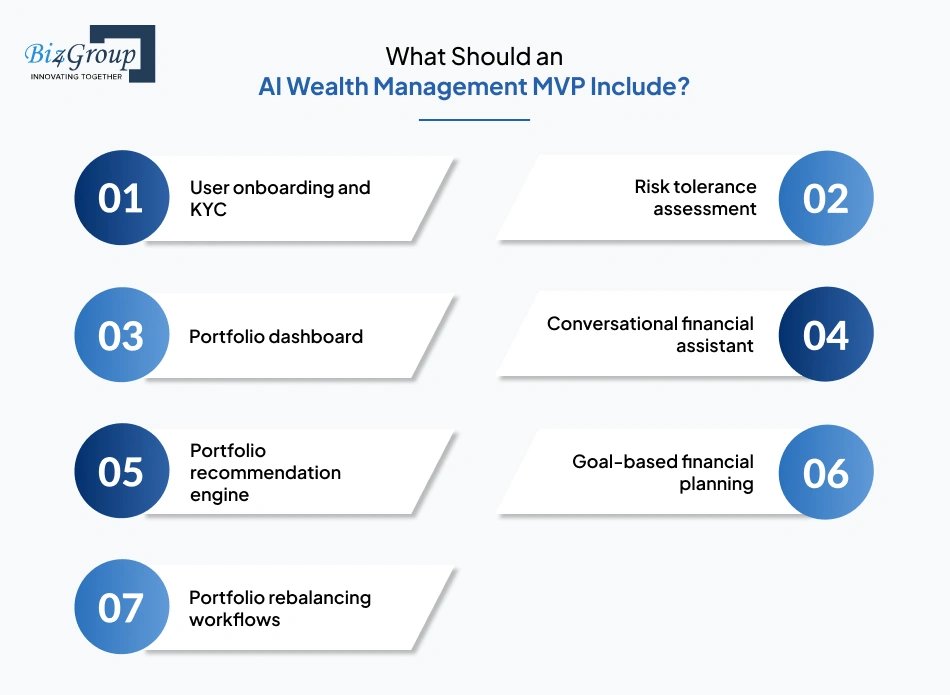

An AI wealth management MVP should focus on a few core financial workflows instead of trying to become a full-featured brokerage platform immediately. Most successful startups begin with onboarding, portfolio tracking, conversational financial guidance, and basic recommendation systems before adding advanced automation features.

Many founders entering wealthtech today are asking variations of the same question:

“I am a fintech entrepreneur who wants to build an AI wealth management app and I need a comprehensive step by step development roadmap that explains exactly what needs to be built how long it will take how much it will cost and what regulatory approvals are required before launching in the US market?”

That concern is valid because AI wealth platforms become complex very quickly once compliance systems, brokerage integrations, portfolio logic, and AI workflows are added.

For startups trying to build AI wealth management application products, the goal of an MVP is simple: launch something useful, trustworthy, and operationally stable before expanding the feature set.

Most AI wealth startups begin with features that support onboarding, portfolio visibility, financial guidance, and user engagement.

|

MVP Feature |

Why It Matters |

|---|---|

|

User onboarding and KYC |

Required for account setup and compliance |

|

Risk tolerance assessment |

Supports personalized recommendations |

|

Portfolio dashboard |

Shows holdings and performance |

|

Conversational financial assistant |

Makes the platform easier to use |

|

Portfolio recommendation engine |

Suggests portfolio allocations |

|

Goal-based financial planning |

Connects investing to financial goals |

|

Portfolio rebalancing workflows |

Keeps allocations aligned over time |

Many teams entering fintech MVP development now prioritize conversational workflows because users expect financial products to feel interactive instead of static.

The best MVPs focus on solving one clear problem well before expanding into additional workflows.

Many startups add too many complex features too early, which increases infrastructure costs and compliance risk.

|

Features to Delay |

Why Teams Usually Delay Them |

|---|---|

|

Autonomous trade execution |

Higher operational and compliance risk |

|

Tax-loss harvesting automation |

Requires advanced portfolio infrastructure |

|

Multi-asset investing support |

Adds regulatory complexity |

|

Advanced AI agents |

Difficult to monitor early |

|

International investing support |

Creates legal and compliance overhead |

|

Social investing systems |

Moderation and suitability challenges |

|

High-frequency portfolio analytics |

Expensive market data infrastructure |

This is where many teams struggle during custom AI wealth management app development because they focus on feature quantity instead of usability and reliability.

A smaller and more stable MVP usually performs better than a platform overloaded with unfinished features.

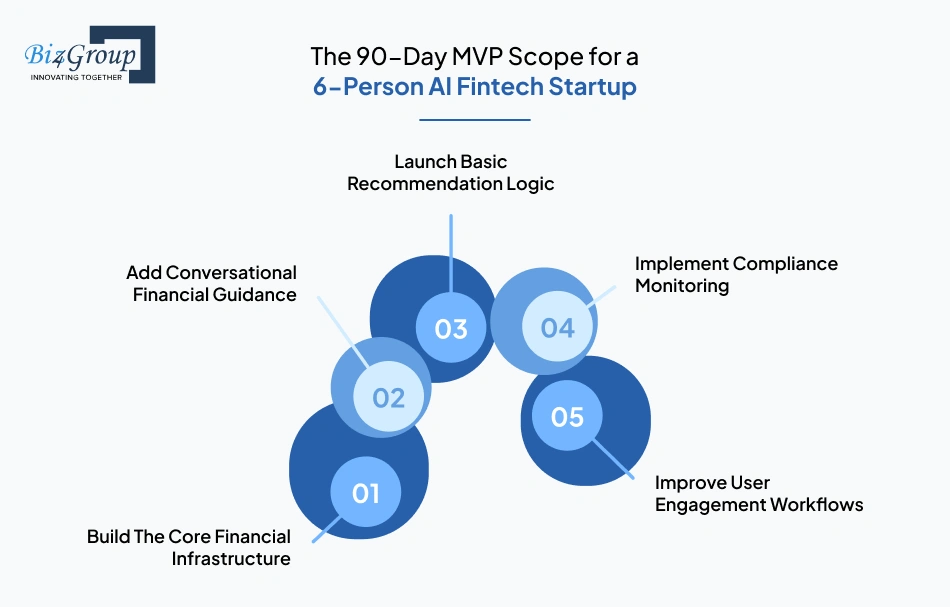

A small fintech team can realistically launch a functional MVP within 90 days if the scope remains controlled.

The first phase usually includes onboarding, KYC workflows, brokerage API integration, portfolio dashboards, and financial data pipelines.

The second phase focuses on portfolio explanations, recommendation workflows, and conversational support powered by LLM systems and retrieval pipelines.

Early recommendation systems should remain partially deterministic instead of fully AI-generated to reduce compliance and explainability risks.

Before launch, teams should add audit logging, recommendation tracking, consent systems, and escalation workflows.

Once the platform becomes stable, teams can improve notifications, onboarding flows, and personalization systems. This is also where startups often begin exploring AI model development for advanced recommendation systems and behavioral analysis.

Most early-stage wealthtech failures happen because the product scope grows faster than the team’s operational capacity.

Building an AI-native wealth platform requires experience with financial infrastructure, AI systems, compliance workflows, and scalable backend architecture.

|

Biz4Group LLC Capability |

Why It Matters for Wealthtech Startups |

|---|---|

|

AI-powered fintech development |

Supports intelligent financial workflows |

|

Wealthtech platform architecture |

Helps reduce scalability problems |

|

Brokerage and API integrations |

Speeds up infrastructure setup |

|

Conversational AI implementation |

Improves onboarding and engagement |

|

Compliance-aware system design |

Reduces operational risk |

|

MVP-focused development approach |

Helps startups launch faster |

As a software development company in Florida, Biz4Group LLC works with startups building modern wealth platforms focused on personalization and AI-native financial experiences.

For founders planning to develop an intelligent AI wealth management app, choosing the right development partner can reduce infrastructure mistakes, compliance gaps, and expensive rebuilds later.

Modern AI wealth platforms are built using multiple connected systems, not just a mobile app and a chatbot. A typical architecture includes frontend applications, backend financial infrastructure, AI orchestration layers, brokerage integrations, compliance systems, and financial data pipelines working together in real time.

Many founders entering wealthtech ask questions similar to this:

“I want to build an AI wealth management app for the US market and I need a development partner that understands both the technical requirements of AI powered investment advisory platforms and the SEC FINRA and fiduciary compliance obligations that apply to apps providing personalized investment recommendations?”

That concern is valid because AI wealth management software development requires much more than connecting an LLM to a portfolio dashboard. The platform architecture must support security, compliance, personalization, scalability, and explainability from the beginning.

Most AI wealth apps use modular architectures where different layers handle different responsibilities.

|

Infrastructure Layer |

Common Technologies and Functions |

|---|---|

|

Frontend Layer |

ReactJS development and NextJS development for dashboards, onboarding, and portfolio interfaces |

|

Backend Layer |

NodeJS development for APIs, authentication, workflows, and real-time processing |

|

AI and Data Layer |

Python development for recommendation systems, analytics, and AI pipelines |

|

Database Layer |

PostgreSQL, MongoDB, Redis, and vector databases |

|

Cloud Infrastructure |

AWS, Azure, or Google Cloud |

|

DevOps and Monitoring |

Docker, Kubernetes, CI/CD pipelines, logging, and monitoring tools |

Most teams entering fintech wealth management software development now prefer cloud-native infrastructure because it allows recommendation systems, brokerage APIs, and financial workflows to scale independently instead of becoming tightly coupled.

Good architecture decisions early usually reduce technical debt later.

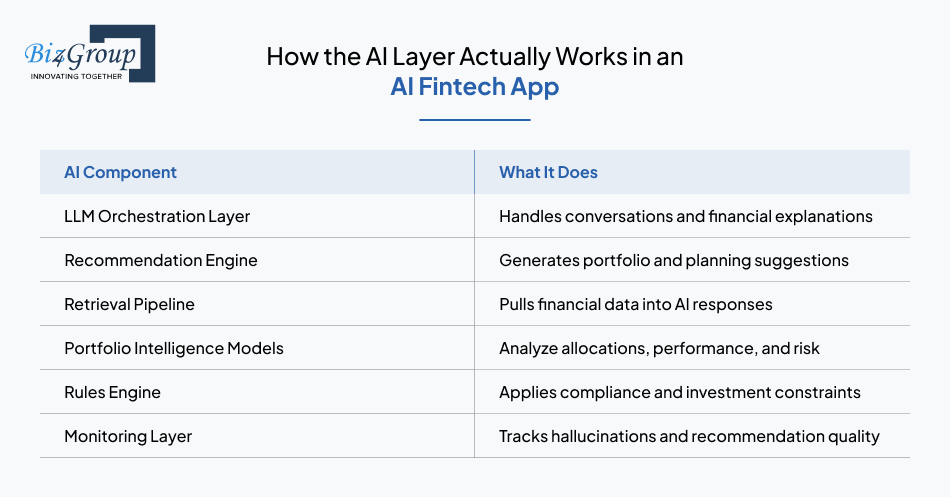

The AI layer inside a wealth platform is usually a combination of systems working together instead of one standalone model.

|

AI Component |

What It Does |

|---|---|

|

LLM Orchestration Layer |

Handles conversations and financial explanations |

|

Recommendation Engine |

Generates portfolio and planning suggestions |

|

Retrieval Pipeline |

Pulls financial data into AI responses |

|

Portfolio Intelligence Models |

Analyze allocations, performance, and risk |

|

Rules Engine |

Applies compliance and investment constraints |

|

Monitoring Layer |

Tracks hallucinations and recommendation quality |

This setup is becoming standard in AI investment management app development because financial AI systems must remain explainable, stable, and easy to monitor.

Some startups outsource parts of their orchestration and infrastructure work early while validating product-market fit. That is one reason demand for AI automation services has increased across AI-native fintech products over the last few years.

The strongest wealth platforms combine AI-generated insights with deterministic financial logic instead of relying completely on generative AI outputs.

RAG systems are important in wealth management because financial AI models need access to current and verified financial data during conversations.

RAG pipelines pull live portfolio data, transaction history, market information, and financial documents during user interactions.

AI responses become more reliable when the system retrieves portfolio-specific information before generating recommendations.

RAG systems reduce inaccurate financial responses by grounding outputs in verified financial data sources.

Retrieved financial sources can be logged and reviewed during audits or compliance checks.

RAG pipelines help generate personalized insights using user portfolios, financial goals, and investment behavior.

This is becoming a core part of smart wealth management app development, especially for platforms focused on conversational financial guidance and adaptive portfolio intelligence.

Most AI wealth startups rely heavily on APIs instead of building every financial service internally.

Common API categories include:

As wealth platforms become more proactive, many startups are also experimenting with AI agent implementation for tasks like portfolio monitoring, alert generation, recommendation workflows, and user engagement automation.

Modern wealth platforms increasingly behave like connected financial ecosystems instead of standalone investing tools.

The moment an AI wealth app starts giving personalized financial guidance, compliance becomes part of the product itself. Founders building AI wealth platforms need to think about recommendation accuracy, auditability, regulatory exposure, and user safety much earlier than most software startups. In wealth management, bad AI outputs can quickly turn into legal and financial problems.

An AI wealth app usually enters regulated territory when it starts giving personalized investment recommendations instead of general financial education. If the platform analyzes a user’s portfolio, income, goals, or risk tolerance to suggest financial actions, regulators may classify it as an investment advisory product.

In many cases, yes. If the platform provides personalized investment advice in exchange for money, the company may need to register as a Registered Investment Advisor (RIA) at the state or federal level. Some startups try to position their platforms as educational tools, but that becomes harder once AI systems begin recommending specific investments or allocation changes.

Develop an AI financial advisor app with conversational workflows, portfolio automation, and real-time financial insights.

Talk to Our Fintech AI TeamThe SEC focuses on fiduciary responsibility, disclosure transparency, and recommendation oversight. FINRA rules become important when broker-dealer infrastructure is involved. Reg BI requires financial recommendations to align with the customer’s best interest. This is why many startups bring in compliance specialists before they integrate AI into an app handling portfolio recommendations or financial planning.

Hallucination risk happens when AI systems generate inaccurate, outdated, misleading, or fabricated financial information. In wealth management, this can affect portfolio explanations, retirement projections, tax guidance, or investment recommendations. Several recent use cases of AI chatbot in banking and financial services have shown how quickly inaccurate financial outputs can damage user trust and create compliance problems.

Most serious wealth platforms do not allow unrestricted AI outputs inside critical financial workflows. Instead, they use controlled systems that combine retrieval pipelines, rule-based portfolio logic, compliance filters, recommendation limits, and escalation workflows. This is one reason enterprise AI solutions in fintech require much stricter controls than normal consumer AI apps.

Financial AI systems need traceability. Platforms should log prompts, recommendations, retrieved data sources, user actions, and model outputs so teams can review decisions during audits or disputes. Human escalation also matters because some financial situations should automatically move from AI systems to licensed professionals. Many startups overlook this when they hire AI developers without experience in regulated financial systems.

SOC 2 becomes important very early because wealth platforms handle sensitive financial and identity data from the start. Brokerages, banking partners, and enterprise clients increasingly expect SOC 2 readiness before approving integrations or partnerships. This is especially common in fintech products connected to investing, payments, and money transfer infrastructure.

In AI wealth management, compliance is not something added after launch. It directly affects product architecture, recommendation systems, onboarding flows, and operational workflows from the beginning.

Fintech startups using intelligent automation can reduce manual advisory workflows by up to 60% with modern AI wealth management software development.

Explore AI Wealth Infrastructure

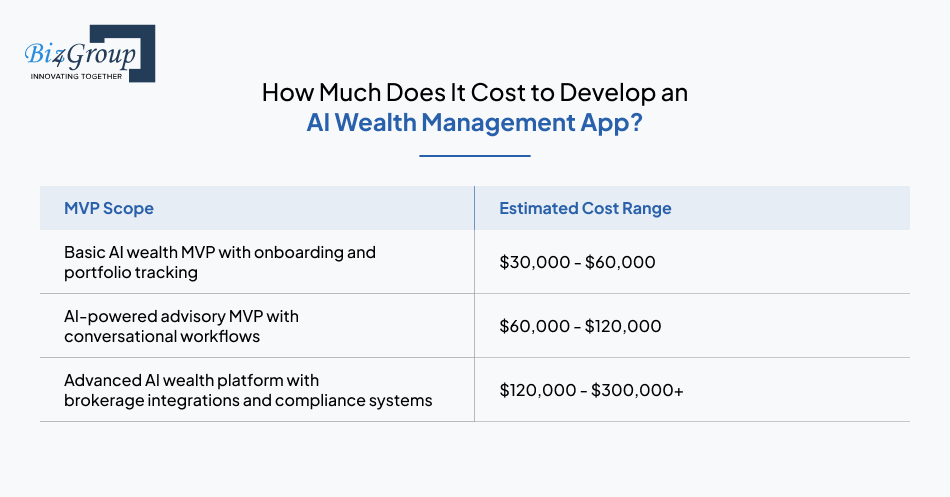

The cost to develop an AI wealth management app usually falls between $30,000 and $300,000 depending on the feature set, AI complexity, compliance requirements, and third-party integrations involved. This is only a rough estimate. A simple MVP costs far less than a production-ready platform with brokerage integrations, AI recommendation systems, and compliance infrastructure.

Most startups begin with a focused MVP instead of building a complete investment platform from day one.

|

MVP Scope |

Estimated Cost Range |

|---|---|

|

Basic AI wealth MVP with onboarding and portfolio tracking |

$30,000 - $60,000 |

|

AI-powered advisory MVP with conversational workflows |

$60,000 - $120,000 |

|

Advanced AI wealth platform with brokerage integrations and compliance systems |

$120,000 - $300,000+ |

The biggest cost factors are usually brokerage integrations, recommendation systems, compliance tooling, and financial data infrastructure.

This is why many founders evaluate AI fintech app development cost early instead of waiting until development starts.

A smaller MVP with a clear use case is usually easier and cheaper to validate than a large platform with too many unfinished features.

Most founders expect to spend money on frontend and backend development. What surprises many teams are the ongoing infrastructure and operational costs after launch.

Some commonly underestimated expenses include:

Many teams also underestimate how expensive conversational financial systems become at scale. Maintaining an AI conversation app becomes much more complex once personalized recommendations, compliance checks, and financial workflows are added.

For most wealthtech startups, infrastructure costs grow much faster than frontend development costs.

AI-native wealth platforms come with recurring costs that traditional fintech apps often do not have.

Every portfolio explanation, recommendation, or AI-generated response increases LLM usage costs. These costs grow quickly as user activity increases.

Audit logging, recommendation tracking, consent management, and monitoring systems all require ongoing infrastructure and operational support.

Market data feeds, brokerage APIs, portfolio analytics, and aggregation services usually operate on recurring subscription models.

AI pipelines, vector databases, orchestration systems, and analytics workflows increase compute and storage costs as the platform scales.

SOC 2 preparation, penetration testing, encryption systems, and audit readiness become necessary very early in fintech products.

Many startups reduce costs by launching in phases instead of building every advanced feature immediately.

Most early-stage AI wealth startups operate with small cross-functional teams instead of large engineering departments.

A typical team structure includes:

Some startups also outsource parts of their infrastructure and automation work during early product validation. This is becoming increasingly common in business app development using AI, especially for teams trying to validate product-market fit before expanding internal hiring.

In most cases, wealthtech startups scale more successfully by controlling product scope early instead of building too many systems at once.

Accelerate wealth management app development with brokerage integrations, AI guardrails, and scalable cloud architecture.

Schedule a Strategy Call With Our AI ExpertsMillennials are becoming one of the biggest growth markets in wealthtech because they expect financial guidance to work like modern software, not traditional advisory firms.

Many are inheriting wealth, managing multiple income sources, investing on their own, and making financial decisions through apps long before talking to an advisor. That shift is creating strong demand for AI-native wealth platforms built around accessibility, personalization, and continuous guidance.

A growing number of founders are now asking questions like:

“We are a fintech startup team with a seed funding round of 1.5 million dollars and we want to build an AI wealth management app targeting millennial investors who are underserved by both traditional financial advisors and existing robo advisor platforms and we need a comprehensive development guide that tells us exactly what to build how much it will cost how long it will take and what regulatory approvals we need?”

Traditional wealth platforms mostly focused on portfolio management. Younger investors increasingly want financial guidance that feels interactive, flexible, and easier to understand.

Most millennials are not searching for “better ETF allocation.”

They are trying to answer practical questions like:

Traditional robo-advisors automated investing, but they did not help users understand financial decisions in everyday life. Younger investors also manage financial situations many older wealth products were not designed around:

That is why many startups are building products focused on ongoing financial guidance instead of static portfolio management. The real wealthtech startup opportunity is building systems that continuously explain, guide, and adapt to user behavior.

This is also making democratizing wealth management more realistic because AI reduces the cost of delivering personalized financial guidance at scale.

People trust financial AI when the system feels predictable, transparent, and easy to verify.

|

What Builds Trust |

What Reduces Trust |

|---|---|

|

Clear recommendation explanations |

Overconfident AI responses |

|

Consistent platform behavior |

Constantly changing advice |

|

Visibility into portfolio logic |

Black-box recommendations |

This becomes especially important when building AI personal wealth management app experiences for younger investors who are comfortable using AI tools but still skeptical of financial institutions.

Many users are more comfortable using AI guidance when:

That shift is changing how younger users evaluate financial products.

The market is slowly moving away from the idea that AI should fully replace financial advisors. Instead, many successful platforms are combining AI systems with human oversight.

AI works well for onboarding, portfolio monitoring, financial education, notifications, and ongoing guidance.

Users still want human support during retirement planning, inheritance decisions, tax situations, or market volatility.

Human review layers help reduce operational and compliance risks around financial recommendations.

Even younger investors who use AI tools regularly often want the option to speak with a licensed professional when needed.

This hybrid model is becoming common in products positioned as an AI investment app for millennials, especially platforms focused on long-term financial engagement instead of passive investing automation.

Some startups are also experimenting with AI-first pricing models combined with optional human advisory upgrades. That shift is influencing how founders think about how to monetize AI app ecosystems in wealthtech.

The next generation of wealth platforms will likely compete more on trust, guidance quality, and user experience than portfolio automation alone.

Create a modern AI portfolio management platform designed for personalization, compliance, and hybrid advisory experiences.

Build Your AI Wealth Product

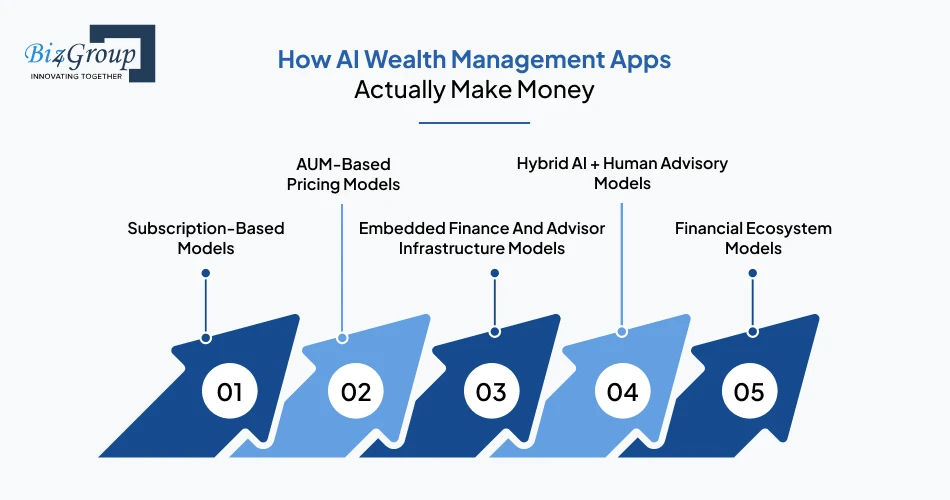

AI wealth management apps usually make money through subscriptions, AUM-based fees, infrastructure licensing, or embedded financial services. The best model depends on who the product is built for, how the platform delivers value, and how involved the company becomes in managing user money.

Many early-stage wealth apps charge monthly or yearly subscription fees instead of taking a percentage of user investments. This model works well for younger investors who may not have large portfolios yet but still want financial guidance, portfolio insights, and planning tools.

Subscription models are also easier for startups because revenue stays more predictable during market volatility.

Many wealth platforms charge a percentage of assets under management (AUM). As user portfolios grow, platform revenue grows automatically.

This model works best for products with strong retention and long-term investing behavior because revenue depends directly on portfolio growth. It is also one of the most common drivers of AUM growth fintech businesses.

Some startups do not sell directly to consumers. Instead, they provide APIs, white-label systems, or advisor infrastructure to banks, fintech companies, and wealth firms.

This approach is becoming more common in embedded finance wealth ecosystems where companies want AI-powered investing and financial guidance features without building the infrastructure internally.

Some platforms combine AI-generated financial guidance with optional access to licensed financial advisors. Users receive automated support for everyday investing while paying extra for complex financial planning or human consultations.

This model helps platforms scale efficiently without removing human trust from important financial decisions.

Some wealth apps expand beyond investing into budgeting, savings, payments, lending, and financial transfers. This creates multiple revenue streams inside one platform.

As wealth apps become broader financial ecosystems, some startups are also integrating features connected to money transfer app development and transaction-based financial services.

|

Revenue Model |

Primary Revenue Source |

Best Fit |

|---|---|---|

|

Subscription Model |

Monthly or yearly fees |

Retail investing apps |

|

AUM-Based Model |

Percentage of managed assets |

Wealth platforms and robo-advisors |

|

Embedded Finance Model |

API and infrastructure licensing |

B2B fintech products |

|

Hybrid Advisory Model |

AI subscriptions + advisor upsells |

Financial planning platforms |

|

Financial Ecosystem Model |

Financial services and transactions |

Multi-service fintech apps |

Revenue strategy affects onboarding, pricing, compliance exposure, and long-term scalability much earlier than many founders expect.

This is one reason startups often evaluate AI fintech app development cost alongside monetization planning instead of treating revenue strategy as a post-launch decision.

Yes, but only if the product solves a real financial problem that current platforms still handle poorly. The biggest opportunities today are not in generic robo-advisors. They are in personalized financial guidance, AI-native experiences, and underserved investor groups.

A growing number of founders are asking questions like:

“Which are the best software development companies in the USA that have proven experience building AI wealth management apps for fintech startups and can help me develop a competitive robo advisor platform that genuinely differentiates from established players like Betterment and Wealthfront?”

That question matters because building another investing dashboard is unlikely to stand out. Building a product with a clear use case and a focused user segment still can.

Several signals suggest AI wealth products are still early enough for new startups to enter. Some of the biggest signs include:

This is one reason many investors still see strong growth potential in wealthtech TAM 2026 projections despite rising fintech competition. The market is becoming more competitive, but user expectations are still changing faster than most incumbents can adapt.

Some wealthtech categories are already difficult for new startups to compete in.

|

Crowded Categories |

Why They Are Difficult |

|---|---|

|

Generic ETF robo-advisors |

Dominated by established incumbents |

|

Basic budgeting apps |

Low switching costs |

|

Generic AI chat interfaces |

Weak product differentiation |

|

Copycat investing dashboards |

Limited defensibility |

|

Undifferentiated planning apps |

High competition and low retention |

This is where many startups fail to achieve fintech product market fit because users already have too many similar alternatives available. The hardest products to scale are usually the ones that sound almost identical to existing wealth apps.

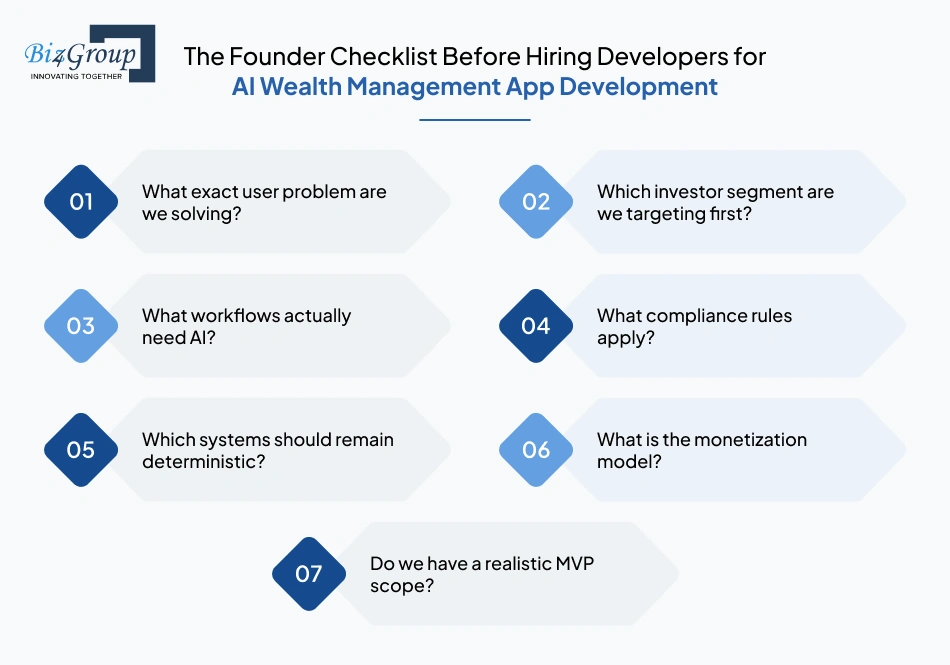

Before building anything, founders should validate the market problem, product positioning, and compliance assumptions first.

|

Founder Question |

Why It Matters |

|---|---|

|

What exact user problem are we solving? |

Strong positioning improves retention |

|

Which investor segment are we targeting first? |

Narrow focus improves product clarity |

|

What workflows actually need AI? |

Prevents unnecessary complexity |

|

What compliance rules apply? |

Affects architecture and operations early |

|

Which systems should remain deterministic? |

Reduces hallucination and audit risks |

|

What is the monetization model? |

Shapes onboarding and pricing |

|

Do we have a realistic MVP scope? |

Prevents overbuilding |

Many founders spend too much time asking how to build a custom AI powered wealth management application for fintech startups entering the investment advisory market before validating whether the actual user problem is strong enough to support a business.

This is also why some startups use AI automation services early instead of hiring large engineering teams before validating product demand.

The strongest AI wealth startups usually begin with a focused problem, a narrow MVP scope, and a clear understanding of compliance and infrastructure requirements.

Build an intelligent AI robo advisor app development roadmap with financial planning workflows, portfolio tracking, and secure fintech APIs.

Start Building With AI Fintech SpecialistsAI wealth management is becoming one of the biggest product shifts in fintech because users increasingly want financial guidance that feels personalized, accessible, and continuously adaptive.

For startups, the opportunity is still wide open across:

At the same time, this is no longer a lightweight fintech build.

Teams entering this space now need to think seriously about compliance architecture, recommendation accuracy, brokerage integrations, AI guardrails, infrastructure scalability, and long-term user trust from the beginning.

The strongest products over the next few years will likely come from founders who treat AI wealth platforms as real financial systems, not experimental chatbot products.

If you plan to build AI software in wealthtech, execution quality matters far more than feature quantity.

Working with an experienced custom software development company can also help reduce costly mistakes around infrastructure, compliance, scalability, and AI implementation early in the product journey.

Building an AI Wealth App? Let’s Validate the Product Before You Burn Through Engineering Budget.

Most AI wealth management MVPs take around 3 to 6 months to build depending on the feature scope, AI complexity, brokerage integrations, and compliance requirements. Production-grade platforms with advanced recommendation systems, portfolio automation, and regulatory infrastructure can take significantly longer.

The development cost for an AI wealth management app usually ranges between $30,000 and $300,000. Smaller MVPs with basic onboarding and portfolio tracking sit on the lower end, while platforms with AI-driven financial guidance, brokerage integrations, compliance systems, and advanced infrastructure move toward the higher end.

Most AI wealth platforms use APIs for banking connectivity, brokerage infrastructure, KYC verification, market data, payments, and portfolio management. Common integrations include Plaid APIs, brokerage APIs, market data providers, authentication services, and compliance monitoring systems.

AI systems can support financial guidance workflows, but regulatory obligations depend on how the platform operates. If the app generates personalized investment recommendations, the company may fall under investment advisor regulations and need to comply with SEC, FINRA, and fiduciary requirements.

The hardest part is usually not the AI model itself. Most technical complexity comes from combining AI systems with financial infrastructure, compliance monitoring, portfolio logic, auditability, brokerage integrations, and real-time financial data pipelines in a secure and scalable way.

Most platforms are moving toward hybrid models instead of fully replacing advisors. AI systems are highly effective for onboarding, portfolio monitoring, financial education, and continuous guidance, while human advisors still play an important role in complex financial planning and emotionally sensitive decisions.

with Biz4Group today!

Our website require some cookies to function properly. Read our privacy policy to know more.