info@biz4group.com

info@biz4group.com

Imagine a digital system that doesn’t wait for instructions but instead, understands your business goals, learns from real-time feedback, and takes independent actions to get the job done.

Read More

AI Summary Powered by Biz4AI

AI Summary Powered by Biz4AI

Modern insurance carriers are under pressure to process claims faster, reduce FNOL costs, and improve accuracy right from the first notice of loss (FNOL), the stage where a policyholder first reports an incident, and a claim officially enters the system. The problem is that many FNOL systems still rely on manual entry and rule-based routing, creating delays before claims handling even begins.

That matters because FNOL is no longer just an intake function. It is where claim costs, processing speed, routing accuracy, and fraud risk start taking shape.

The pressure to modernize is hard to ignore:

So what actually changes when agentic AI enters the picture?

Instead of simply collecting and routing claim information, agentic AI can interpret incoming data, identify risk signals, classify claims, validate coverage, and trigger downstream workflows automatically. FNOL starts acting as a decision layer rather than a data-entry step.

From our experience at Biz4Group, the biggest challenge is not the AI itself. It is turning messy FNOL inputs from calls, agents, and digital channels into structured, policy-aware claim events that downstream systems can trust and act on in real time.

This is why insurance automation software development is increasingly focused on decision orchestration at the point of intake. It is also why insurers evaluating an agentic AI development company are paying closer attention to domain expertise, integration capabilities, and an understanding of real claims operations rather than AI features alone.

And that raises a more important question: what does a truly agentic FNOL system look like in practice, and how much of the claims lifecycle can it realistically automate?

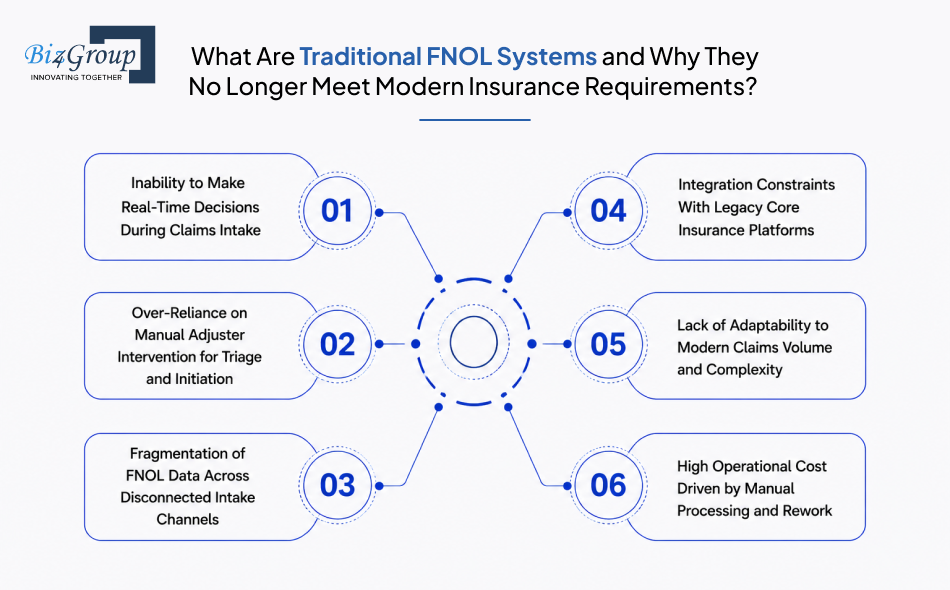

Traditional FNOL systems are insurance claims intake systems designed to capture first notice of loss data, log it into core platforms, and route it through predefined workflows for further processing. They are primarily rule-based systems built around structured data entry and manual validation rather than real-time decision-making.

The problem is that these systems were not built for today's speed, scale, or multi-channel complexity, which is where most inefficiencies begin to surface.

FNOL data is captured at intake but not acted on immediately, which delays triage and claim assignment. In many insurance operations, this adds several hours to multiple days before a claim moves forward, directly increasing cycle time.

Adjusters are still required to review, classify, and route incoming claims in many legacy setups. This creates a dependency on human availability, which slows down early-stage processing and introduces inconsistency in decisions.

Claims enter through phone calls, email, web forms, and agents, but are often stored in separate systems. This leads to duplicate entries, missing information, and additional reconciliation work before processing can begin.

Core systems like Guidewire or Duck Creek were not designed for real-time or AI-driven intake. As a result, FNOL data often needs transformation and validation layers before it can be used downstream, adding latency and complexity.

During surge events such as catastrophic weather losses, claims volume can increase by 200 to 300 percent within days. Static, rule-based workflows struggle to keep pace, creating bottlenecks across intake and routing functions.

Manual entry, validation, and correction cycles add significant operational overhead. Industry studies consistently show that manual-heavy claims processing can contribute to 20–30 percent inefficiency in total claims handling effort.

Modern carriers trying to reduce this dependency are increasingly moving toward automation approaches that go beyond workflow rules. In many cases, this includes working with an AI chatbot development company to modernize FNOL intake across digital channels.

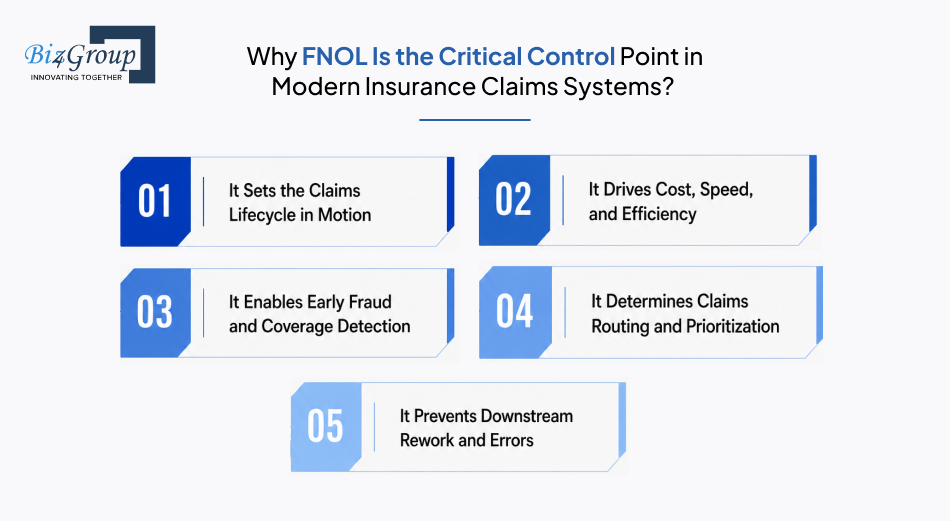

FNOL is the most critical control point in insurance claims systems because it determines how every claim will be processed, prioritized, and resolved. It directly influences cost, speed, fraud detection, and overall operational efficiency across the entire claims lifecycle.

Here is what makes FNOL so decisive in real insurance operations.

FNOL is the first structured entry point of a claim into the system, and everything downstream depends on how accurately it is captured and classified.

Early FNOL decisions influence how much manual effort, time, and rework a claim will require later in the lifecycle.

FNOL is the first point where anomalies, inconsistencies, and coverage mismatches can be flagged before claims progress further.

Routing logic at FNOL decides whether a claim goes to straight-through processing, manual review, or specialist handling.

Errors made at FNOL compound across the claims lifecycle, leading to corrections, delays, and inconsistent settlements later.

FNOL remains the point where operational efficiency is either created or lost. Many insurers are now exploring enterprise AI solutions to strengthen this stage, especially as they modernize toward more automated claims ecosystems.

As FNOL becomes more intelligent and automated, its role is shifting from a simple intake step to a true control layer that shapes the entire claims journey.

Also Read: Top Real-World Use Cases for Agentic AI in 2026

Agentic AI in FNOL refers to systems that capture and interpret claims data, make decisions based on it, and trigger downstream actions across the claims workflow in real time. The shift is from FNOL being a passive intake step to becoming an active decision layer inside insurance claims management systems, where early information directly shapes how the claim is handled.

If you're evaluating agentic AI for FNOL, these are the kinds of questions that usually come up first:

Traditional FNOL systems store and route claims after structured entry. Agentic FNOL systems interpret incoming data, resolve ambiguity, and trigger actions immediately, reducing dependency on downstream queues and manual decision points.

Below is how that shift actually shows up in real insurance operations.

FNOL becomes the point where claims are acted on immediately instead of waiting in review queues. The system makes early decisions based on available information, which improves speed but increases reliance on input quality.

For instance, a minor auto accident with clear photos and structured details can move directly into repair coordination without waiting for adjuster review. But if the initial details are incomplete or unclear, the same speed can lead to the claim being routed incorrectly before anyone catches it.

All FNOL inputs from phone, web, mobile, or agents are merged into one structured claim view instead of separate records.

In real operations, a customer might start a claim over a call center, then later upload supporting images through a mobile app. Instead of creating two disconnected records or forcing manual reconciliation, the system combines them into a single evolving claim timeline.

Claims are categorized at intake based on severity, complexity, and risk signals instead of waiting for manual sorting.

This becomes especially useful during high-volume events. For example, after a storm, property damage claims with similar patterns can be grouped automatically and directed to catastrophe handling teams instead of flooding general queues.

Once FNOL data is validated, workflows begin automatically without waiting for human assignment.

So instead of an adjuster first reviewing and then triggering next steps, things like repair scheduling or document requests can start immediately after intake validation. This reduces idle time between claim creation and action.

FNOL decisions influence how the entire claim behaves beyond intake, including investigation depth and settlement path.

A claim identified early as low complexity can move through a simplified path with fewer checkpoints, while higher-risk claims naturally stay in deeper review tracks. The key shift is that early classification starts shaping downstream behavior instead of just informing it.

Fraud checks and coverage validation now begin at intake rather than later in the lifecycle.

So if multiple claims show similar incident patterns or inconsistent details, the system can flag them immediately instead of letting them move further into processing where recovery becomes harder.

Claims that meet predefined conditions can bypass manual handling entirely and move through automated pipelines.

In practice, this often applies to low-value or straightforward claims where all required data is present at FNOL, allowing the system to push them straight toward settlement workflows without adjuster involvement.

Agentic AI doesn't just make FNOL faster. It changes its role inside the claims system. Instead of simply feeding downstream processes, FNOL starts influencing how those processes behave from the very beginning.

In most modernization programs, this shift is closely tied to how insurers approach AI integration services, especially when upgrading FNOL without replacing core claims infrastructure.

Agentic FNOL architecture is essentially a layered system that turns raw, multi-channel claim inputs into structured, decision-ready claims events that can safely trigger downstream actions in insurance systems. The focus is not just on ingestion, but on ensuring each FNOL event is interpretable, auditable, and executable across legacy platforms like claims and policy systems.

A common question from engineering teams building in this space is, "we are a software development company building a claims management platform for an insurance client and they want agentic AI built into the FNOL layer, we have AI experience but not insurance experience, what are the domain-specific things we absolutely need to understand before we start building".

The short answer is: FNOL architecture is less about models and more about controlled decision flow, system reliability, and integration with insurance core systems.

Layer |

What it does in simple terms |

Why it matters in FNOL |

|---|---|---|

Multi-Channel Intake Layer |

Collects FNOL data from phone, web, mobile, agents |

Prevents fragmented claim entry across channels |

Data Extraction Layer |

Converts unstructured inputs into structured claim fields |

Enables downstream systems to actually use FNOL data |

Agent Orchestration Layer |

Coordinates AI agents for triage, classification, and decisions |

Drives intelligent FNOL processing instead of static rules |

Event-Driven Processing Layer |

Triggers actions based on FNOL events in real time |

Reduces delay between intake and claims execution |

Integration Layer |

Connects FNOL system with core insurance platforms |

Ensures compatibility with legacy systems like claims and policy engines |

Human-in-the-Loop Governance |

Adds review points for sensitive or high-risk decisions |

Keeps compliance and auditability intact |

Why this structure matters in practice?

This architecture is designed to solve one core problem in insurance claims management systems: FNOL data must move from messy, multi-source input to structured, policy-aware decisions without breaking downstream workflows.

Similarly, insurers often rely on AI chatbot integration at the intake stage, but the real value only appears when those inputs are normalized and passed through an event-driven and governance-aware pipeline.

In real deployments, this layered structure is what allows insurers to safely move from traditional FNOL intake to agentic FNOL systems without destabilizing core claims infrastructure.

One challenge that often gets underestimated is insurance context. Agentic systems are only as effective as their ability to understand policy terminology, coverage concepts, and operational workflows. Through its experience developing AI-powered insurance solutions, including AI platforms designed to help agents navigate complex policy information and decision-making processes, Biz4Group LLC has seen firsthand why insurance-specific knowledge is just as important as the underlying AI architecture.

Deploy Agentic AI in Insurance Claims Management Systems to cut manual effort, rework, and operational delays.

Improve Claims Efficiency

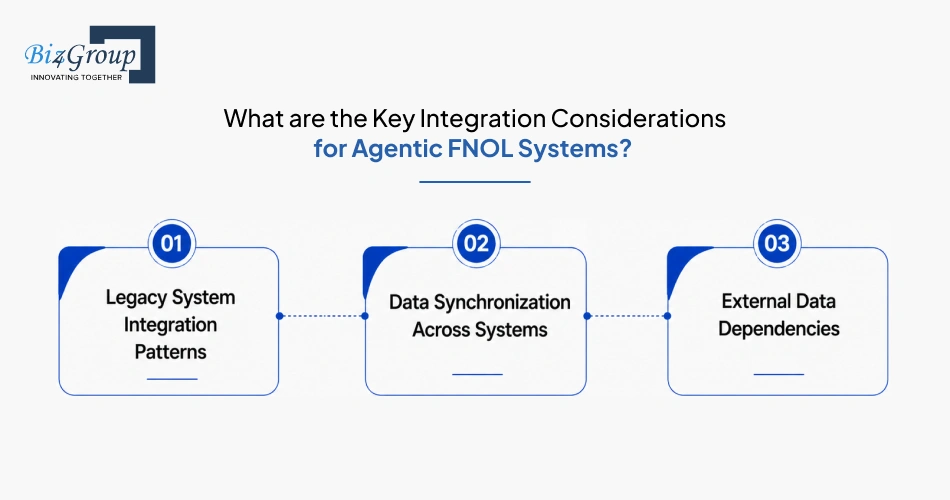

Agentic FNOL systems only work well when they connect smoothly with the insurance systems already in place. In most carriers, the real challenge is not building the AI layer, but making sure FNOL decisions actually move correctly across claims, policy, and external data systems without breaking consistency or slowing operations.

According to a report, A key reason this becomes difficult is that insurance integration is often more expensive and impact-heavy than it appears at first.

That's exactly why FNOL integration is usually where modernization efforts slow down or fail.

Most insurance systems were not built for real-time or AI-driven decisions. They work fine for structured data and batch updates, but FNOL today is a different kind of input stream.

So when an agentic FNOL layer is added, the real question is not "does the AI work", it is "can the legacy system even understand what it is receiving".

In practice, integration becomes a translation problem. AI generates structured decisions in real time, but older claims or policy systems often expect slower, more rigid data formats.

That gap is usually where things get tricky. The AI side does its job, but the system around it needs careful handling to avoid breaking workflows. This is also why insurers often hire AI developers when they want FNOL modernization without disturbing core claims systems.

FNOL data does not stay in one place for long. It flows into claims, policy, billing, and adjuster tools, and each one tends to update at its own pace.

So here is where things usually get interesting. What happens when one system shows a claim as "new", but another already shows it as "under review"?

That mismatch is more common than it sounds. And even though it looks small on the surface, it can affect routing decisions, reserves, and even how customer updates are triggered. Most insurers solve this by keeping everything aligned through event-based updates or reconciliation logic so all systems eventually agree on the same claim state.

External data is now a big part of FNOL decisioning. Weather feeds, fraud signals, identity checks, and even repair network data can influence how a claim is handled right at intake.

But the real question is not whether you can plug these in. It is: How much you should trust them in the first few seconds of a claim?

If the data is delayed or noisy, early decisions can easily go off track, especially during high-volume events like storms or regional incidents.

That is why many insurers prefer working with a custom software development company to build a controlled layer between FNOL and external intelligence sources, instead of letting everything directly influence decisions.

For a mid-sized US carrier, building an agentic AI FNOL and claims management system typically falls in the range of $30,000 to $250,000+. This is a broad ballpark estimate, not a fixed price, because the final cost changes significantly based on how complex the claims environment is, how much legacy infrastructure is involved, and how much real-time decisioning is expected from the system.

A simple way to think about it is: cost increases mainly with integration depth, automation scope, data complexity, and compliance requirements. For example, a carrier with heavy legacy dependence and multi-channel FNOL intake will spend more on system integration than on AI modeling itself.

A common operational question from insurers is: "our claims team spends most of their day manually entering data from FNOL calls into our system and routing claims to adjusters, i want to know if agentic AI can actually handle all of that automatically and what building that kind of system would cost for a mid-sized US carrier"

The short answer is yes, it can automate most of that workflow, but cost depends on how far you push automation versus augmentation.

Level |

Typical Cost Range |

What it Includes |

|---|---|---|

MVP Agentic AI FNOL System |

$30,000 – $80,000 |

Basic FNOL intake automation, simple triage, limited integrations |

Mid-Level Agentic AI FNOL System |

$80,000 – $150,000 |

Multi-channel intake, AI-based routing, partial legacy integration, basic fraud detection |

Enterprise-Grade Agentic AI FNOL System |

$150,000 – $250,000+ |

Full FNOL orchestration, real-time decisioning, deep integration with claims and policy systems, human-in-the-loop governance |

The largest costs are often not tied to the AI itself. Most budget overruns happen because carriers underestimate the work required to make agentic FNOL systems operate reliably inside existing insurance environments.

Common hidden costs include:

For many carriers, integration ends up consuming more effort than the AI layer itself. In fact, insurers with fragmented systems often discover that the real investment lies in connecting and synchronizing existing platforms before advanced automation can deliver meaningful value.

The need for outside expertise can also affect overall cost. For example, carriers that require AI consulting services during planning and architecture design will typically spend more upfront than organizations with mature internal AI and claims transformation teams.

The better question is not "What does an agentic FNOL system cost?" but "What does continuing to rely on manual FNOL processes cost?" When intake, triage, and routing remain heavily dependent on human effort, operational expenses rise, cycle times increase, and claims leakage becomes harder to control. The right investment level ultimately depends on how much of that inefficiency a carrier is trying to eliminate.

Leverage Agentic AI in Insurance Claims Management Systems to orchestrate decisions across the entire claims lifecycle.

See What's Possible

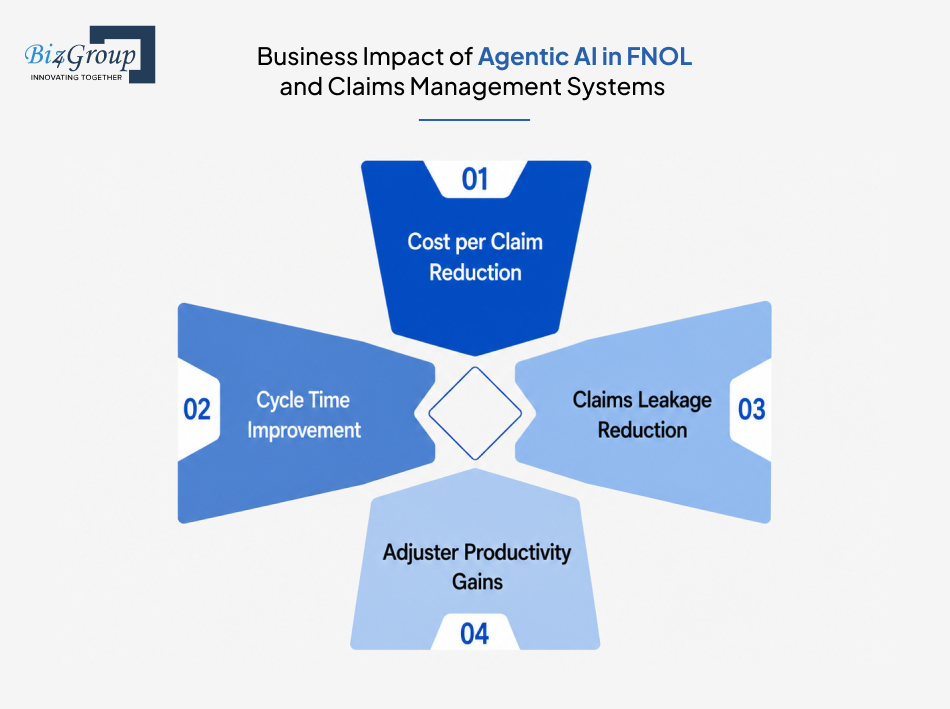

When insurers evaluate agentic AI, the question is rarely whether the technology works. The bigger question is whether it creates measurable business value.

For most carriers, the impact shows up in four areas: lower cost per claim, faster cycle times, reduced claims leakage, and better use of adjuster capacity. Since FNOL influences every claim that enters the system, improvements made there tend to ripple across the entire claims operation.

Where does the cost of handling a claim actually come from?

Most people think about settlements and payouts, but a large portion of claim handling costs comes from the work that happens before those decisions are ever made. Information has to be captured, reviewed, routed, validated, and often re-entered across multiple systems.

Agentic AI reduces many of those manual touchpoints by automating FNOL intake, triage, and workflow initiation. Fewer handoffs generally mean fewer operational hours spent on each claim.

That is one reason FNOL often becomes the first focus area for broader AI automation services. Intake is where many repetitive processes are concentrated, making efficiency gains easier to capture.

So where do claim delays usually come from?

In many cases, claims are not waiting on customers. They are waiting on internal decisions. Someone needs to review intake data, classify the claim, route it to the right team, and trigger the next action.

Agentic AI shortens those waiting periods by acting on FNOL information as it arrives instead of pushing decisions into manual queues.

Many insurers approach the challenge in a way that is similar initiatives of business app development using AI in other departments: remove unnecessary handoffs, reduce waiting between actions, and keep work moving forward.

The result is often a faster path from first notice of loss to resolution.

When claims leakage shows up, where does it usually begin?

Many insurers look at settlement decisions first, but leakage often starts much earlier. Missing information, incorrect classification, overlooked fraud indicators, or coverage validation gaps can all enter the system during FNOL.

The advantage of agentic decision-making is that these issues can be identified closer to the point of intake, before they influence downstream decisions.

A useful way to think about it is: problems are usually cheaper to fix at the beginning of a claim than in the middle or at the end.

If adjusters are among the most valuable resources in a claims organization, how much of their day should be spent on administrative work?

For many carriers, the answer is probably "less than it is today."

Adjusters often spend significant time reviewing intake information, requesting missing documentation, and handling routing-related tasks before they can focus on investigations or claim resolution.

By automating routine FNOL activities, agentic AI allows adjusters to spend more time on work that genuinely benefits from human judgment.

The goal is not to remove people from the process. It is to make sure expertise is being applied where it creates the most value.

Why These Outcomes Matter Together

Each of these benefits is valuable on its own. Together, they create a compounding effect across the claims lifecycle.

Lower handling costs improve efficiency. Faster claim movement improves customer experience. Better intake decisions reduce leakage. More productive adjusters improve operational capacity.

That combination is why many insurers now see FNOL modernization as more than a technology initiative. It is increasingly becoming a business performance strategy.

Business Outcome |

Impact of Agentic AI at FNOL |

|---|---|

Cost per Claim Reduction |

Fewer manual touchpoints across intake, triage, and routing |

Cycle Time Improvement |

Faster decisions and earlier workflow initiation |

Claims Leakage Reduction |

Earlier detection of missing information, fraud signals, and coverage issues |

Adjuster Productivity Gains |

More time spent on complex claims and less on administrative work |

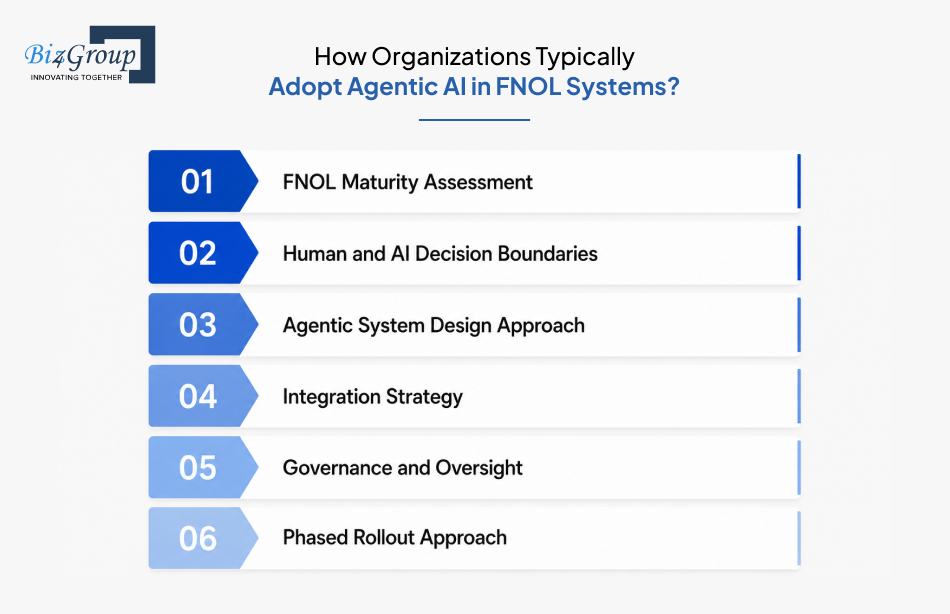

Most insurers do not replace their FNOL process overnight. Adoption typically follows a structured path that starts with understanding current claims intake operations, identifying where automation creates the most value, and gradually expanding agentic capabilities across the claims workflow. The goal is not simply to deploy AI, but to ensure it improves decision-making without disrupting existing operations.

Before introducing agentic AI, insurers need to understand how their current FNOL process performs. Where are delays occurring? Which activities still depend heavily on manual effort? Which intake channels generate the most rework?

Without a clear baseline, it becomes difficult to determine where an agentic claims management system will create the greatest operational impact.

One of the first decisions organizations need to make is determining which actions should be automated and which should remain under human control.

Routine activities such as claim classification, document collection, and routing are often handled by the system, while high-risk coverage disputes or complex fraud investigations continue to involve adjusters and claims specialists.

Once decision boundaries are established, organizations define how the agentic layer will operate within the claims management system.

This includes designing agent workflows, identifying required data sources, and establishing how agentic AI claims orchestration will trigger actions across the FNOL process.

Even the most capable FNOL system cannot operate effectively in isolation.

Organizations must determine how the agentic layer will interact with claims, policy administration, billing, CRM, and third-party data platforms. Teams looking to integrate AI into an app often find that integration planning consumes more effort than the AI implementation itself.

As automation increases, visibility and accountability become more important.

Organizations need clear governance models that define approval thresholds, escalation rules, audit requirements, and human-in-the-loop controls. This ensures automated decisions remain explainable and aligned with business and regulatory requirements.

Most successful implementations start with a limited scope and expand gradually.

Rather than automating every FNOL scenario at once, insurers typically begin with lower-risk claim types, validate performance, and progressively extend automation into more complex workflows. The same staged approach is commonly used during AI model development to reduce risk and improve adoption confidence.

Successful adoption is rarely about deploying more AI. It is about introducing the right level of automation at the right stage of the FNOL process. Organizations that move in phases, establish clear decision boundaries, and build around existing operational realities tend to see smoother adoption and stronger long-term outcomes.

Also Read: How to Build an Agentic AI Workflow Automation System for Business: A Complete Guide

The answer depends on how much control, customization, and speed your organization needs. Some insurers want complete ownership of their insurance claims management system development roadmap, while others prioritize faster deployment and lower implementation effort. In practice, all three approaches can work when aligned with the carrier's technology strategy and operational goals.

Approach |

Best Suited For |

Advantages |

Trade-Offs |

|---|---|---|---|

Build |

Carriers with unique claims workflows and complex integration requirements |

Full control over features, workflows, integrations, and future enhancements |

Higher upfront investment, longer implementation timeline, greater ownership responsibility |

Buy |

Organizations seeking faster modernization and proven capabilities |

Faster deployment, lower development effort, vendor-supported updates |

Limited flexibility, vendor dependency, constrained customization |

Hybrid |

Carriers looking to modernize without replacing existing platforms |

Balances speed and flexibility, preserves existing investments, reduces disruption |

Additional integration complexity and architecture management requirements |

A useful way to think about the decision is to ask: where does your competitive advantage come from?

If FNOL is viewed as a strategic differentiator, a build approach may make sense because it allows complete control over how claims intake, triage, routing, and agentic decision-making operate. In these situations, carriers often work with a software development company in Florida or a specialized insurance technology partner to accelerate delivery while retaining ownership of the resulting platform.

On the other hand, if the goal is primarily operational efficiency, buying an existing platform may provide faster value with less implementation risk.

Hybrid approaches have become increasingly common because they avoid the extremes. Rather than replacing an entire claims management system, insurers can add agentic AI capabilities to existing FNOL processes and expand them gradually over time. This allows modernization to happen in stages while preserving investments already made in core claims infrastructure.

There is no universally correct choice between build, buy, and hybrid. The better question is: which option aligns best with your existing systems, internal capabilities, and long-term claims strategy? For many insurers, the most successful path is the one that delivers meaningful FNOL transformation without introducing unnecessary complexity or operational risk.

Discover how AI Agents in FNOL for Claims Management Systems can improve speed, accuracy, and claims outcomes.

Talk to Our AI Experts

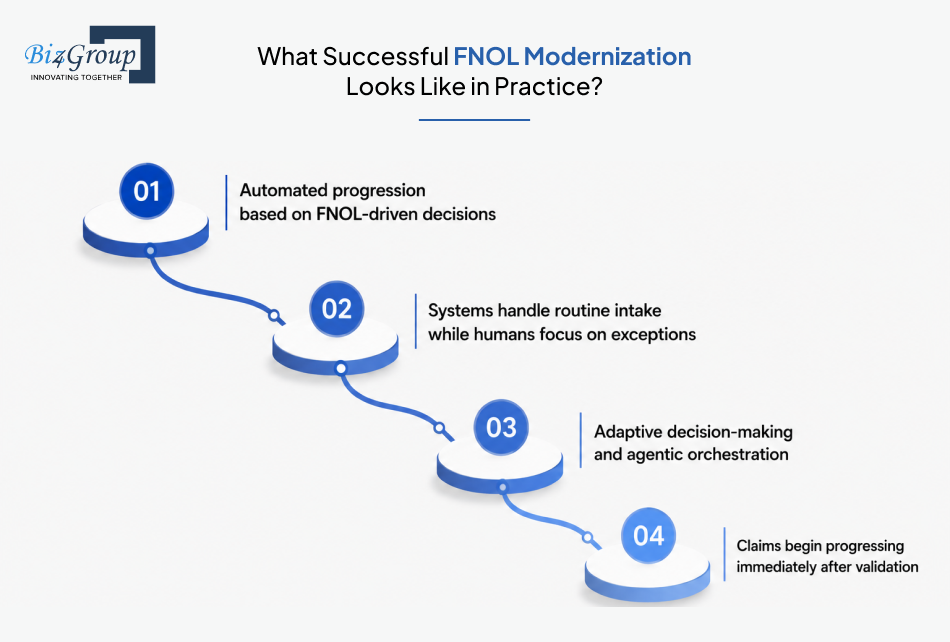

Successful FNOL modernization is not measured by whether AI has been deployed. It is measured by whether claims move faster, manual effort decreases, and better decisions happen closer to the point of intake. When those outcomes start showing up consistently, the modernization effort is delivering real business value.

Area |

Traditional FNOL Environment |

Successfully Modernized FNOL Environment |

|---|---|---|

Workflow Transformation |

Multiple manual handoffs and review queues |

Automated progression based on FNOL-driven decisions |

Shift in Intake Ownership |

Intake teams and adjusters manage most early-stage activities |

Systems handle routine intake while humans focus on exceptions |

Automation Evolution |

Static, rule-based workflows |

Adaptive decision-making and agentic orchestration |

Real-Time Claims Processing |

Claims wait for review before moving forward |

Claims begin progressing immediately after validation |

A common misconception is that successful FNOL modernization means fully autonomous claims processing from day one.

In reality, most insurers start seeing value much earlier. Once FNOL data becomes more structured and decisions start happening closer to intake, claims teams often experience faster routing, fewer handoffs, and less rework.

What does that actually look like in practice?

A simple auto claim that previously moved through multiple reviews before reaching the right adjuster can now be classified, validated, and routed almost immediately after the first notice of loss is received.

The same principle applies regardless of how a claim is reported. Whether it comes through a web portal, mobile application, contact center, or an AI conversation app, the goal remains the same: reduce the time between intake and action.

Another pattern shows up repeatedly in successful FNOL transformations: The strongest programs do not focus only on automation. They also improve the experience for policyholders and claims teams by making FNOL simpler, faster, and easier to navigate. That is why insurers are paying more attention to how information is collected and presented during intake.

For years, FNOL was treated as a data collection step. Today, that approach creates delays, rework, and unnecessary claims costs.

The real value of agentic AI is not that it automates intake. It is that decisions start happening the moment a claim is reported. Coverage validation, claim classification, fraud checks, routing, and workflow initiation can all begin at FNOL instead of waiting for downstream teams.

At Biz4Group LLC, working on AI solutions within insurance environments has reinforced how much operational impact depends on the quality of decisions made before a claim ever reaches an adjuster. As insurers continue modernizing claims operations, that early-stage intelligence is becoming increasingly valuable.

For insurers looking to build AI software for claims modernization, that shift is far more important than automation alone. It is also why the top agentic AI companies in USA are focusing on decision orchestration, not just AI features.

Agentic AI can handle both. It can automate routine claims end-to-end while identifying complex, high-risk, or ambiguous cases that require adjuster review. Most insurers use a combination of automated and human-led decision-making.

Most implementations take between 3 and 6 weeks. The timeline depends on integration requirements, automation scope, data readiness, and the number of existing insurance systems involved.

Yes. Agentic AI is typically integrated with existing claims, policy administration, and billing systems rather than replacing them. Most insurers modernize FNOL while keeping their core platforms in place.

The cost typically ranges from $30,000 to $250,000+. Final costs depend on system complexity, integrations, automation requirements, compliance needs, and deployment scale.

The most common metrics include: cost per claim, FNOL-to-assignment time, claims cycle time, claims leakage rates, straight-through processing rates, and adjuster productivity.

No. Agentic AI automates intake, triage, routing, and other repetitive tasks. Adjusters continue to handle investigations, coverage disputes, negotiations, fraud reviews, and complex claims decisions.

Our website require some cookies to function properly. Read our privacy policy to know more.