info@biz4group.com

info@biz4group.com

Imagine a digital system that doesn’t wait for instructions but instead, understands your business goals, learns from real-time feedback, and takes independent actions to get the job done.

Read More

AI Summary Powered by Biz4AI

AI Summary Powered by Biz4AI

Can AI actually shorten underwriting cycles from weeks to hours without exposing lenders to more risk?

In many cases, yes. But only when the underlying technology, workflows, data strategy, and compliance controls are designed correctly. That's what makes AI real estate underwriting software development such a high-priority investment for commercial lenders, mortgage providers, and real estate investment firms today.

If you're evaluating this technology, chances are you're not looking for another way to automate paperwork.

You're looking for a measurable shift in speed, accuracy, and decision quality.

That urgency is not surprising when you look at where the industry is heading. The AI in real estate space is projected to reach $1303.09 billion by 2030, growing at a compound annual growth rate (CAGR) of 33.9%.

At the same time, commercial real estate firms that have already adopted structured AI underwriting systems are reporting 300 to 500% ROI within the first 12 months, driven mainly by faster underwriting cycles, fewer manual errors, and improved deal throughput.

When teams start thinking about how a real estate AI software development effort actually fits into existing underwriting operations, the discussion quickly shifts from capability to execution, especially around data readiness, risk modeling, and workflow alignment.

That's exactly where Biz4Group LLC comes in with proven experience in turning fragmented underwriting data into structured, AI-ready systems that actually support decision-making.

It also helps CTOs, CIOs & technology leaders in real estate finance understand:

But the answers aren't always obvious.

So, before putting money into the development, it's important to understand what an AI powered property underwriting software is?

Let's turn weeks of manual underwriting into faster, data-driven lending decisions.

Talk to Our ExpertsMost lenders are not only asking what underwriting is. They also want to know what is breaking in their current process, and whether AI real estate underwriting software actually improves it without adding new risk. So first understand what is an AI real estate underwriting software?

Now let's get into the competitive advantages of AI underwriting software.

The reason lenders are investing in these platforms goes beyond efficiency. In competitive lending markets, faster decisions often translate into more closed deals, stronger borrower experiences, and greater operational scalability.

While one lender may spend days reviewing an opportunity, another using AI underwriting software for real estate can analyze the same information in a fraction of the time and move the deal forward sooner.

This advantage becomes especially valuable when underwriting teams are expected to handle growing loan volumes without increasing operational costs.

This advantage comes from the ability to:

The competitive edge is not the technology itself. It is the ability to evaluate more opportunities, maintain underwriting quality at scale, and act on deals before competitors do.

The real shift is not about replacing underwriting judgment. It is about removing the friction that slows it down. Once that shift is clear, the next step is understanding how these systems work actually power these systems behind the scenes and how they fit into real lending workflows.

Most underwriting teams assume AI starts with analysis.

It doesn’t.

It starts with structure. Without clean, organized inputs, even the most advanced models cannot support reliable lending decisions. In AI real estate underwriting software, the entire system is designed to turn fragmented data into decision-ready insights.

The process begins by gathering data from multiple sources into one pipeline. This is a core foundation when teams develop AI real estate underwriting software for lending workflows that depend on speed and consistency. Borrower documents, property files, financial statements, and external market data all flow into a unified system.

The platform relies on multiple data sources, which often requires robust AI integration services to connect underwriting workflows with banking systems, credit bureaus, and property databases.

Once data is collected, the system processes unstructured files and extracts structured information. In most AI underwriting software for real estate solutions, this step replaces manual document review with automated reading of financial and property data.

Extracted data is cleaned and standardized so it can be used consistently across deals. In AI powered property underwriting software, this step ensures that financial comparisons are accurate across different property types and reporting formats.

This stage applies predictive models to evaluate risk across borrower and property profiles. Within AI real estate underwriting software development, this is where historical data and statistical patterns are used to surface risk signals for underwriter review.

The final step brings everything back to human judgment. Underwriters review structured outputs instead of raw files, allowing faster and more consistent decisions in systems built through AI powered property underwriting software development.

With AI underwriting software for real estate, each step removes friction that traditionally slows down underwriting teams. The result is not just faster processing, but a more structured and consistent decision flow.

In AI real estate underwriting software development, this pipeline is what enables scale without losing control.

Once this pipeline is in place, underwriting stops being a document-heavy process and becomes a structured decision flow. Now comes the real question: how different lending teams apply it across real-world use cases?

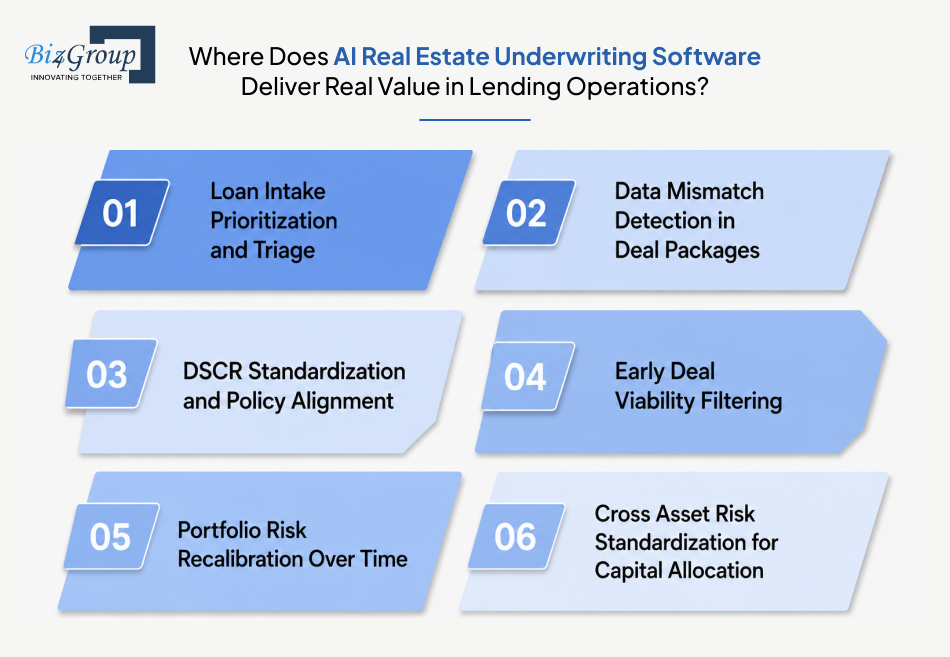

Once this pipeline is in place, underwriting stops being a document-heavy process and becomes a structured decision flow. The real impact becomes clearer when you look at the specific points where decisions slow down, risk gets misread, or capital allocation becomes uncertain. Look here to understand this system actually change outcomes in real lending operations:

Teams often treat all applications the same at the start, which slows down high-value decisions. With AI real estate underwriting software, loan intake is structured so incoming deals are automatically scored for completeness, risk signals, and data quality before an underwriter reviews them.

Example: A mortgage lender processes 300 applications in a week. AI underwriting software ranks applications based on completeness and early risk indicators, routing fully structured low-risk deals into a fast-track queue while pushing incomplete files into a verification stage before underwriting begins.

A major underwriting risk comes from inconsistencies across documents that individually appear correct. In AI underwriting software for real estate, cross-document validation compares rent rolls, financial statements, and lease data at the field level to identify hidden conflicts.

Example: A commercial real estate (CRE) deal shows consistent total income across financial summaries, but AI underwriting logic detects mismatched lease-level rent values compared to aggregated rent roll data, triggering a validation flag before risk scoring is finalized.

Dept service coverage ratio (DSCR) differences across lenders often come from inconsistent assumptions rather than actual deal performance. With AI powered property underwriting software, DSCR is recalculated using a unified underwriting policy layer applied consistently across all submissions.

Example: Two industrial loan files show similar profitability on paper, but AI underwriting recalculates DSCR using standardized expense treatment and reveals one deal falls below lending thresholds due to excluded operating costs.

Many underwriting resources are wasted on deals that fail basic risk thresholds but are still processed manually. Early-stage filtering process of AI real estate underwriting software evaluates income stability, occupancy trends, and borrower strength before full underwriting begins.

Example: A bridge loan application is analyzed immediately after ingestion and flagged due to unstable occupancy history and volatile cash flow patterns, preventing full underwriting effort on a structurally weak deal.

Portfolio exposure does not remain static after origination. The AI real estate underwriting software system, continuously reprocess portfolio data as new performance inputs arrive, updating asset-level risk scores dynamically.

Example: A multifamily portfolio receives updated rent collection data, and AI recalculates risk exposure across assets, identifying multiple properties where declining collections shift them into higher risk categories.

Different asset classes often use inconsistent underwriting assumptions, which makes capital allocation less precise. AI underwriting solution normalizes inputs so risk scoring remains consistent across asset types.

Example: A real estate investment firm evaluates retail, multifamily, and logistics assets. The AI software for real estate underwriting converts all deal inputs into a standardized format and generates comparable risk scores, enabling consistent capital allocation decisions across asset classes.

Across these scenarios, the value of AI real estate underwriting software comes from how consistently it structures and normalizes underwriting inputs before human judgment is applied.

That consistency is what ultimately improves both decision quality and capital efficiency. But what do you think of the core features inside AI real estate underwriting software that enable these kinds of underwriting decisions at scale?

The best underwriting workflow is the one your team actually uses every day.

Contact Our TeamThe core features determine whether AI underwriting software for real estate in USA powered by AI model development should be able to collect underwriting data, evaluate borrower and property risk, generate recommendations, support compliance requirements, and fit naturally into existing lending workflows. The features below form the foundation of a production-ready underwriting system.

|

Core Feature |

What It Is |

Why It Matters |

|

AI Document Processing |

Automatically reads and extracts information from financial statements, rent rolls, tax returns, bank statements, and property-related documents. |

AI real estate underwriting software depends on accurate data extraction to convert underwriting documents into structured information that can be evaluated consistently. |

|

Borrower Risk Assessment |

Evaluates borrower financial strength, repayment capacity, debt obligations, liquidity, and creditworthiness using historical and current financial data. |

Helps lenders identify potential borrower risks early and supports more consistent lending decisions across different loan types. |

|

Property Risk Assessment |

Analyzes property performance indicators such as NOI, occupancy, cash flow, valuation metrics, market conditions, and asset quality. |

Property-level analysis is a core requirement of AI underwriting software for real estate because asset performance directly influences lending risk. |

|

Automated Risk Scoring |

With the help of AI automation services it assigns risk scores using borrower, property, and financial data based on predefined underwriting criteria and predictive models. |

Creates a standardized framework for evaluating opportunities and improves consistency across underwriting teams. |

|

Underwriting Recommendation Engine |

Generates approval, rejection, or conditional review recommendations using underwriting rules, risk thresholds, and model outputs. |

Enables lenders to process applications more efficiently while maintaining control over final lending decisions. |

|

Compliance & Explainability |

Provides transparency into how risk scores, recommendations, and underwriting outcomes are generated. |

Organizations that develop AI real estate underwriting software must ensure every recommendation can be reviewed, justified, and audited when required. |

|

Human-in-the-Loop Review |

Allows underwriters to review, validate, modify, or override AI-generated recommendations before final approval. |

Preserves human judgment for complex lending scenarios while allowing real estate underwriting automation to handle repetitive analysis tasks. |

These features represent the minimum functional requirements of AI underwriting software for real estate. Without them, lenders often struggle with inconsistent risk evaluations, limited scalability, and continued dependence on manual underwriting processes.

So once these foundational features are in place, what advanced features actually push AI underwriting platforms beyond basic automation and into decision intelligence?

Core capabilities make the system usable. Advanced capabilities make it defensible.

This is where AI real estate underwriting software moves from structured automation into decision intelligence. These features are not required for basic underwriting. They become critical when firms want stronger forecasting, deeper risk insight, and competitive advantage in deal execution.

|

Advanced Feature |

What It Is |

Why It Matters |

|

Predictive default risk modeling |

A machine learning layer that forecasts probability of default based on borrower behavior, asset performance, and macro trends |

In AI underwriting software for real estate, predictive modeling shifts underwriting from reactive evaluation to forward-looking risk assessment, helping lenders avoid exposure before deterioration appears in financials |

|

Scenario-based underwriting simulation |

A simulation engine that tests how changes in interest rates, occupancy, or cash flow affect loan performance |

This capability in AI underwriting platforms allows lenders to stress test deals before approval, improving confidence in volatile market conditions |

|

Automated investment memo generation |

A system that converts underwriting outputs into structured investment summaries for internal or credit committee review |

In AI real estate underwriting software, this reduces manual reporting effort and ensures every deal has a consistent, decision-ready narrative |

|

Market intelligence integration layer |

A feature that pulls external signals like rent trends, vacancy rates, and regional economic indicators into underwriting models |

With AI real estate underwriting solution, external context improves risk accuracy by connecting property-level analysis with broader market conditions |

|

Explainable AI decision layer |

A transparency module that breaks down how risk scores and recommendations are generated |

This is critical in regulated environments where underwriting decisions must be defensible, auditable, and clearly justified |

|

Continuous portfolio intelligence engine |

A system that re-evaluates active loans and assets in real time as new data becomes available |

This feature in AI real estate underwriting system, continuous intelligence shifts underwriting from a one-time event to an ongoing risk monitoring process |

These advanced capabilities do not replace the core underwriting structure. Instead, they extend AI underwriting software for real estate into a system that not only evaluates deals but also anticipates risk, adapts to market conditions, and supports higher-confidence lending decisions.

Together with foundational features, they define the difference between operational automation and a fully intelligent underwriting platform.

Now we move from what the system can do to what constraints govern it in real lending environments (compliance).

“We are running a mortgage lending operation and I want to build an AI underwriting model but I am concerned about fair lending compliance and algorithmic bias and I need to understand what regulatory requirements apply before we deploy this in production.”

Lenders like you often ask this kind of questions on the online platforms. But you need to understand that compliance in lending is not a documentation exercise. It is a system design constraint that determines whether AI real estate underwriting software can be used in production at all.

In regulated lending environments, every automated decision must be explainable, auditable, and legally defensible. That includes how data is used, how risk is calculated, and how final credit decisions are supported.

Underwriting decisions must comply with Equal Credit Opportunity Act (ECOA) and Fair Housing Act (FHA) standards. These regulations prohibit discrimination based on protected characteristics such as race, gender, religion, and other factors.

AI underwriting software for real estate must be designed in a way that risk models only evaluate legitimate credit and property factors. Any indirect bias introduced through correlated variables must be identified and controlled to prevent discriminatory outcomes.

When a loan is denied or modified, lenders are required to clearly explain the reason to the borrower through adverse action notices. For AI-driven systems, this creates a strict requirement: every underwriting decision must be explainable in human terms.

Risk outputs generated by AI real estate underwriting software must map directly to clear drivers such as cash flow strength, occupancy stability, and borrower credit behavior rather than opaque scoring logic.

For banks and institutional lenders, AI models fall under formal Model Risk Management (MRM) expectations defined in SR 11-7 guidance.

This framework requires underwriting models to undergo independent validation before deployment, continuous performance monitoring after launch, clear documentation of assumptions and limitations, and ongoing controls to detect and manage model drift as market conditions evolve.

These controls ensure that predictive models inside AI real estate underwriting software development remain reliable, explainable, and aligned with risk appetite even as market conditions change.

Underwriting platforms process sensitive borrower and property financial data. This data is protected under the Gramm-Leach-Bliley Act (GLBA) and additional state-level privacy laws.

Security architecture in AI real estate underwriting software must enforce encryption, strict access controls, secure storage mechanisms, and governed data usage policies to prevent unauthorized access or misuse of financial information.

Regulators and internal audit teams require full visibility into how underwriting decisions are produced.

Lenders must be able to trace every underwriting output back to its original data sources, transformation steps, model versions, and any rule-based or human overrides applied during the process.

AI real estate underwriting software must maintain continuous data lineage tracking so every decision can be reconstructed and validated during audits or regulatory reviews.

Even in highly automated systems, final lending decisions must remain under human authority in most regulated environments. This ensures accountability cannot be delegated entirely to machine outputs.

Human-in-the-loop governance ensures underwriters retain final approval authority while AI systems provide structured risk intelligence to support decision-making.

These compliance requirements define the operational boundary of AI real estate underwriting software in real lending environments. Without them, even advanced underwriting systems cannot be safely deployed in regulated financial institutions.

At Biz4Group, we have extensive experience building AI-driven real estate underwriting platforms, giving us a practical understanding of compliance, auditability, data governance, and explainability requirements that modern lending systems must support.

Once these compliance boundaries are clear, the next step is understanding how the actual development process is structured to build AI real estate underwriting software that can operate within them.

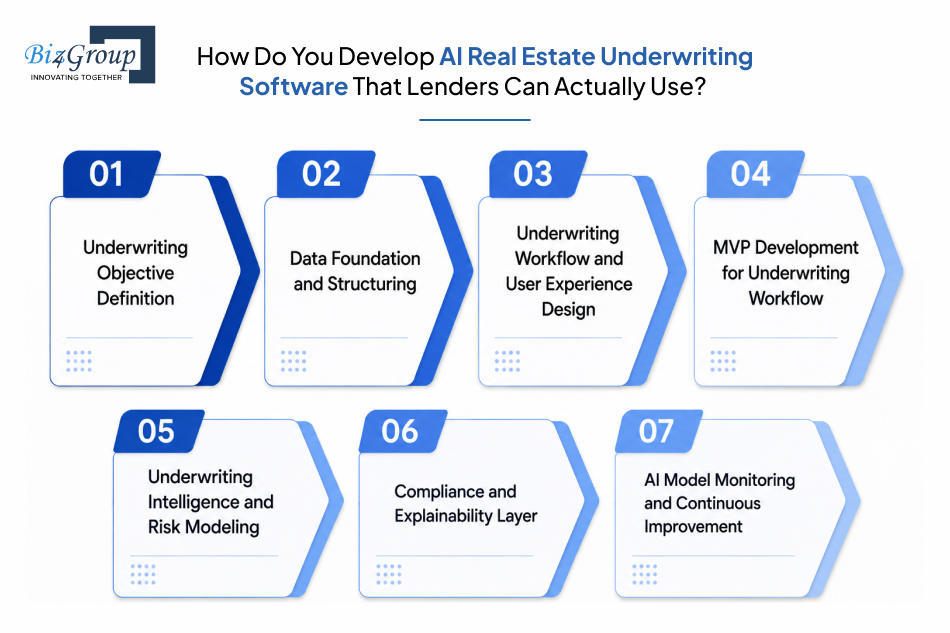

Organizations looking to build AI software for underwriting must approach development as a structured, multi-stage process rather than a standalone AI project. Through structured MVP development services Biz4Group validates whether underwriting data, workflows, and risk logic can work together before scaling. Here are the correct development steps:

The AI real estate underwriting software development begins by clearly defining what the underwriting platform must achieve inside real lending operations. Some systems focus on speeding up loan decisions, while others prioritize risk visibility or portfolio intelligence. Without this clarity, system design becomes unnecessarily complex and misaligned with credit expectations.

At this stage, underwriting policies are translated into system-level requirements so every output aligns with real decision-making standards.

AI underwriting performance depends entirely on how well lending data is structured. This phase focuses on consolidating historical loan files, borrower profiles, financial statements, and property records into a consistent and usable format.

The goal is not just storage but creating a reliable foundation for modeling and decision logic.

Before building an MVP, lenders need to define how underwriters, credit analysts, and risk teams will interact with the platform. Even the most accurate underwriting model will struggle to deliver value if users cannot easily review, validate, and act on its outputs.

This phase focuses on designing intuitive workflows, dashboards, approval paths, and review experiences that align with real lending operations. We as a UI/UX design company in USA ensure the platform supports adoption from day one.

For organizations evaluating feasibility before large-scale investment, understanding how to build AI real estate app MVP frameworks can significantly reduce implementation risk.

A minimum viable version of AI real estate underwriting software is built to test document ingestion, basic extraction, and initial risk scoring in a controlled environment.

The purpose is to confirm that underwriting logic holds up under real or historical deal scenarios.

Once the MVP is validated, the focus shifts to building the intelligence layer. This stage combines document understanding, data extraction, and predictive risk analysis into a single underwriting engine.

The platform converts unstructured financial documents into structured underwriting data and uses that information to evaluate borrower strength, property performance, and deal-level risk.

Before scaling, regulatory and audit requirements are embedded into system behavior. Every output must be traceable, explainable, and aligned with lending regulations across jurisdictions.

This ensures underwriting decisions can be reviewed and defended in regulated environments.

After deployment, model performance must be continuously tracked to prevent drift and degradation over time. Lending environments evolve, and models must adapt accordingly to remain reliable.

This stage ensures long-term stability of AI underwriting software for real estate in production.

Each stage builds toward a production-ready underwriting platform that supports consistent decision-making, regulatory alignment, and scalable lending operations across portfolios.

So what technologies actually power a production-ready AI real estate underwriting platform once it moves beyond the development phase?

What technology stack decisions actually determine whether AI real estate underwriting software can scale reliably in production environments?

“We want to create a real estate underwriting platform using AI, what technology stack should we choose?” If this question bothers you then understand that choosing the right stack for AI real estate underwriting software is not about picking popular tools.

It is about selecting components that can handle heavy document processing, financial data modeling, compliance logging, and real-time decision support without breaking under production lending workloads.

Below is a practical, production-oriented breakdown of the technology stack used across real-world AI underwriting systems.

|

Layer |

Technologies Used |

Why It Matters |

|

Frontend (Underwriting Interface) |

React, Next.js, TypeScript |

Through the |

|

Backend API Layer |

Node.js, Python (FastAPI), Java (Spring Boot) |

These frameworks with the |

|

AI and Machine Learning Layer |

Python, TensorFlow, PyTorch, Scikit-learn |

Python development technologies with ML frameworks is widely used because they support rapid model development, financial risk modeling, and predictive analytics required in underwriting systems. They enable continuous refinement of scoring logic in AI underwriting software for real estate. |

|

Document Processing and OCR |

AWS Textract, Google Document AI, Tesseract |

These tools are selected for their accuracy in extracting structured financial data from unstructured documents like PDFs and lease files. They significantly reduce manual data entry, which is a major bottleneck in underwriting workflows. |

|

Data Storage and Warehousing |

PostgreSQL, MongoDB, Snowflake, BigQuery |

These systems are used because underwriting platforms deal with both structured financial data and large historical datasets. They support fast querying for real-time decisions and long-term portfolio risk analysis. |

|

Data Processing and Pipelines |

Apache Kafka, Apache Spark, Airflow |

These tools ensure reliable data movement and processing across ingestion, transformation, and model execution stages. They help maintain consistency in underwriting workflows even when data volume increases. |

|

Risk Scoring and Analytics Engine |

MLflow, Python-based scoring services, custom ML models |

These technologies are used to maintain versioned, trackable risk models that can evolve over time. In AI real estate underwriting software development, they ensure scoring logic remains consistent, testable, and auditable. |

|

Cloud Infrastructure |

AWS, Microsoft Azure, Google Cloud Platform |

Cloud platforms are chosen for scalability, security compliance, and ability to handle large-scale underwriting workloads across multiple lending portfolios without infrastructure bottlenecks. |

|

API Integration Layer |

REST APIs, GraphQL, gRPC |

These technologies are used because underwriting systems must connect with external financial data providers, credit bureaus, and banking systems in real time with low latency and high reliability. |

|

Security and Compliance Layer |

OAuth 2.0, JWT, AWS KMS, HashiCorp Vault |

These tools are essential for protecting sensitive borrower and financial data while enforcing strict access control, encryption, and secure key management required in regulated lending environments. |

|

Monitoring and Model Governance |

Prometheus, Grafana, MLflow, Datadog |

These tools are used to continuously track system performance, detect model drift, and ensure predictive accuracy remains stable over time in production underwriting environments. |

A production-grade used in AI real estate underwriting software development is not defined by individual tools, but by how well these layers work together to support secure, explainable, and scalable underwriting decisions across real lending environments.

Once the right technology stack is in place, how does the actual development cost of AI real estate underwriting software break down across engineering, infrastructure, and model development efforts?

“How much does it cost to create a real estate underwriting platform using AI, and why does the budget vary so widely across projects?” Numerous real estate lenders in USA want to know the answer to this question before they hire AI developers.

The cost of AI real estate underwriting software development typically ranges from $25,000 to $250,000+, depending on system complexity, data readiness, compliance requirements, and the depth of AI capabilities. The variation is significant because underwriting platforms are not simple applications. They combine data engineering, machine learning, financial logic, and regulated decision workflows.

This breakdown highlights how different features contribute to the overall development cost of AI real estate underwriting software.

|

Feature Area |

Cost Impact Range |

Why It Affects Cost |

|

Document ingestion and data extraction |

$5,000 to $40,000 |

Costs increase when the system must process diverse financial documents, leases, and borrower files at scale. In AI underwriting software for real estate, higher accuracy OCR and document intelligence require advanced models and integration work. |

|

Financial data normalization engine |

$5,000 to $30,000 |

Standardizing financial metrics like NOI, DSCR, and occupancy requires custom rule design and validation logic across multiple property types. |

|

Risk scoring and predictive models |

$10,000 to $80,000 |

Machine learning models require training on historical underwriting data, feature engineering, validation cycles, and continuous tuning in AI real estate underwriting software development environments. |

|

Workflow automation and underwriting logic |

$5,000 to $25,000 |

Building structured underwriting flows with routing, approvals, and escalation rules requires backend orchestration and policy mapping. |

|

Compliance and audit trail system |

$5,000 to $30,000 |

Regulatory-grade logging, traceability, and explainability layers increase engineering effort due to strict data tracking and reporting requirements. |

|

Cloud infrastructure and deployment |

$3,000 to $25,000 (setup + scaling) |

Costs depend on compute usage for AI models, storage for underwriting data, and scalability needs across lending volumes. |

|

Integration with external financial APIs |

$5,000 to $20,000 |

Connecting credit bureaus, banking APIs, and property data sources adds complexity due to authentication, data mapping, and latency handling. |

The final cost of developing real estate AI underwriting software depends on several structural and technical decisions that shape engineering effort and long-term scalability.

Beyond initial development, several ongoing and indirect costs significantly affect total investment in AI underwriting software for real estate systems.

Cost efficiency in AI real estate underwriting software building is achieved through architectural decisions that reduce unnecessary complexity while preserving scalability.

The total investment in AI real estate underwriting software development depends less on fixed pricing and more on how deeply the platform integrates intelligence, compliance, and automation into real lending workflows.

With the budget, architecture, and development roadmap defined, what challenges should lenders expect when implementing AI real estate underwriting software, and how can those challenges be addressed before they become costly setbacks?

Building AI real estate underwriting software is rarely limited by technology alone. Most implementation roadblocks come from data quality issues, operational constraints, regulatory requirements, and adoption challenges that surface after development begins.

Understanding these challenges early helps reduce project risk and improves the chances of successful deployment.

|

Challenge |

Why It Happens |

Practical Solution |

|

Poor Data Quality |

Historical underwriting data is often incomplete, inconsistent, or spread across multiple systems, making it difficult to train reliable models. |

Establish data governance standards early and create a structured data preparation process before model training begins. |

|

Regulatory and Compliance Risk |

Compliance requirements become more complex as AI underwriting software for real estate takes a larger role in risk evaluation and lending decisions. |

Build explainability, audit trails, model governance, and compliance controls into the platform architecture from the beginning. |

|

Model Bias and Fair Lending Concerns |

As AI real estate underwriting software learns from historical lending data, it may inherit patterns that create unintended bias across borrower groups. |

Perform fairness testing regularly and validate models against fair lending requirements before deployment. |

|

Resistance From Underwriting Teams |

Teams may view automation as a replacement rather than a decision-support tool. |

Position AI as an underwriting assistant, maintain human review stages, and involve underwriters throughout implementation. |

|

Complex Third-Party Integrations |

Credit bureaus, banking systems, property databases, and internal platforms often use different formats and standards. |

Adopt an API-first architecture and prioritize integrations based on business impact rather than implementing everything at once. |

|

Model Performance Drift |

Market conditions, borrower behavior, and property trends change over time, reducing model accuracy. |

Continuously monitor model performance and retrain models using updated underwriting data. |

|

Scaling From MVP to Production |

Scaling challenges often emerge when AI real estate underwriting software development moves from limited pilot environments to enterprise-level underwriting volumes. |

Design for scalability from the beginning using cloud-native infrastructure and modular system architecture. |

None of these challenges are unique to AI underwriting software for real estate, but they become more visible as platforms move from pilot projects to production environments. The organizations that succeed are usually the ones that treat data quality, compliance, and adoption as business priorities rather than technical tasks.

Now, the bigger question becomes: where is AI real estate underwriting software heading next, and which innovations are most likely to shape lending decisions over the coming years?

"I want to explore how AI agents can automate real estate underwriting workflows in the future."

That question points directly to where the industry is heading. The next generation of AI real estate underwriting software will not simply assist underwriters with analysis. It will increasingly automate portions of the underwriting process, coordinate decisions across systems, and continuously evaluate risk as new information becomes available.

Organizations investing today are not just planning for real estate underwriting automation. They are preparing for underwriting ecosystems that can execute, monitor, and optimize lending workflows with far less manual intervention. Advances in generative AI are expected to automate large portions of underwriting documentation and reporting workflows.

Future underwriting software combined with

1. Collect missing information across multiple data sources

2. Coordinate verification workflows without manual intervention

3. Prepare review-ready underwriting packages for human approval

As organizations build AI-powered real estate underwriting platforms, a single AI model may no longer be sufficient. Future systems

1. Separate borrower, property, and compliance evaluations

2. Enable independent validation across risk categories

3. Improve decision consistency through collaborative analysis

Compliance monitoring is expected to shift from periodic reviews to continuous oversight. Future underwriting systems will proactively evaluate decisions against regulatory requirements before approvals are finalized.

1. Detect potential fair lending concerns earlier

2. Monitor policy deviations in real time

3. Support ongoing regulatory readiness

Future underwriting platforms will influence portfolio strategy in addition to individual lending decisions. This represents a major evolution for AI underwriting software for real estate, moving beyond deal evaluation into capital planning.

1. Identify markets with stronger risk-adjusted potential

2. Highlight emerging portfolio concentration risks

3. Support data-driven lending expansion decisions

Future underwriting systems may maintain continuously updated digital representations of financed assets. These living models will help lenders evaluate changing risk conditions long after loan origination.

1. Track changes in property-level risk continuously

2. Incorporate live market and occupancy signals

3. Improve long-term portfolio visibility

These trends suggest that the future of AI underwriting software for real estate will focus less on automating individual tasks and more on creating connected decision systems that support lending operations at scale. Many of these innovations are already influencing new real estate AI apps ideas focused on lending, investment analysis, and portfolio intelligence.

Building successful AI real estate underwriting software requires more than machine learning expertise. It demands a strong understanding of lending workflows, compliance requirements, financial data modeling, and scalable product engineering.

As an established AI app development company, Biz4Group helps lenders, real estate investment firms, and PropTech companies transform manual underwriting processes into intelligent, production-ready platforms.

Whether you're looking to develop AI real estate underwriting software for faster loan decisions or planning to build AI-powered real estate underwriting platforms with advanced risk intelligence, our team combines AI engineering, cloud architecture, workflow automation, and compliance-focused development to deliver solutions built for real-world lending environments.

While underwriting platforms have unique lending requirements, many of the underlying challenges remain the same, including data processing, workflow automation, intelligent decision-making, and user adoption. Over the years, Biz4Group has built AI-powered real estate solutions that address these challenges, providing experience that translates directly into underwriting software development.

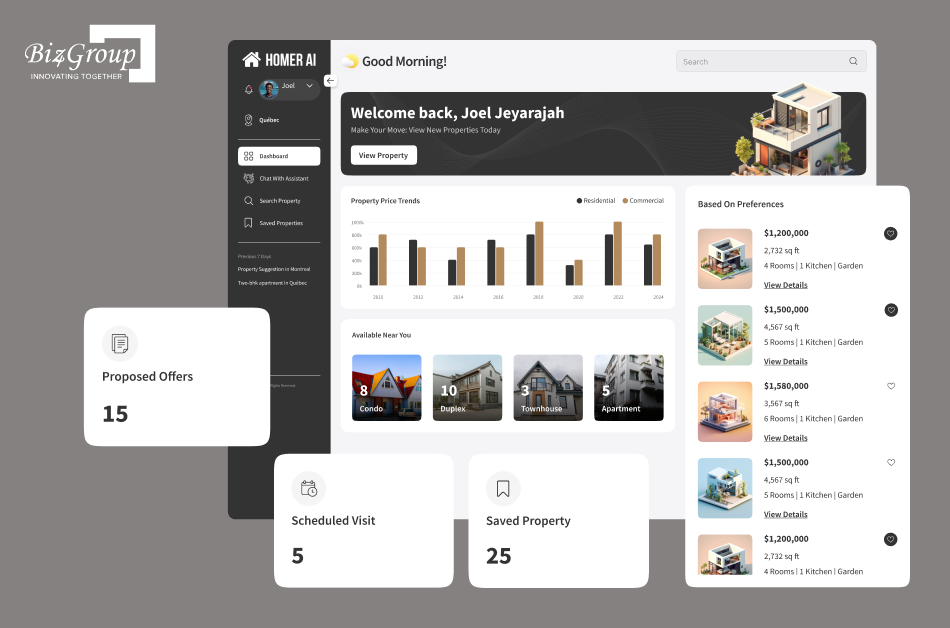

With Homer AI, Biz4Group built an AI-powered property platform that helps buyers and sellers discover properties through conversational interactions, personalized recommendations, and intelligent property matching. The project strengthened our expertise in applying AI to real estate decision-making workflows.

Facilitor streamlines the home-buying journey by guiding users from property discovery to purchase readiness. Building the platform required structured workflows, transaction management, and user-centric experiences that mirror many of the operational challenges found in lending environments.

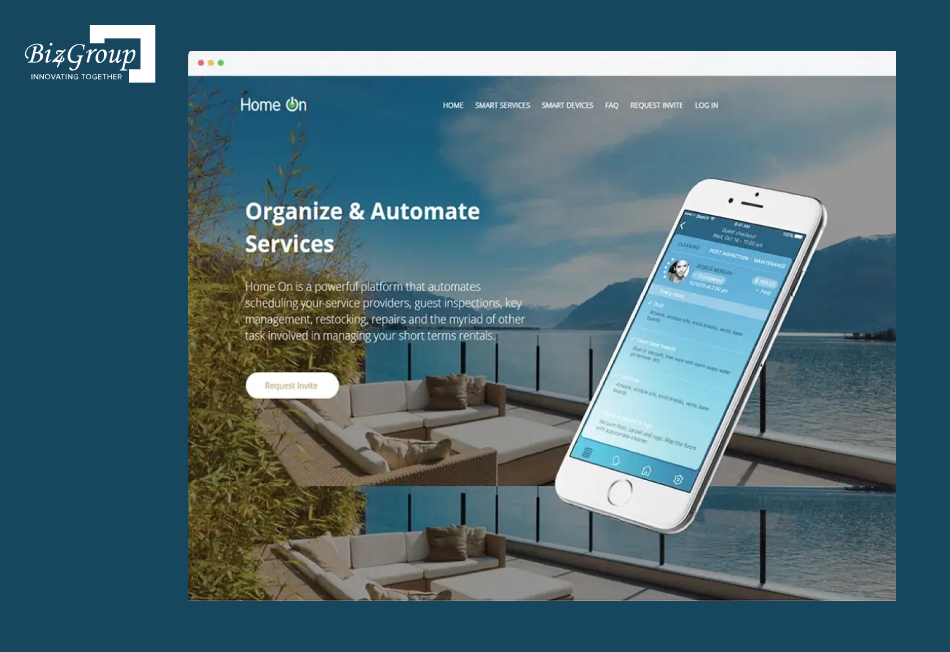

Homeon is a property operations platform that automates maintenance, inspections, scheduling, and rental management activities. The project highlights our experience in building scalable workflow automation systems that handle large volumes of real estate data and operations efficiently.

From MVP development to enterprise-scale deployment, we help organizations implement AI underwriting software for real estate that improves underwriting efficiency, supports data-driven decisions, and scales alongside business growth.

We'll help you build an AI underwriting platform that works harder than your inbox.

Schedule a ConsultationThe future of lending will not be defined by who reviews the most files. It will be defined by who can turn data into faster, more accurate, and more scalable underwriting decisions.

As demand for speed, transparency, and risk precision continues to grow, AI real estate underwriting software is becoming a strategic investment for lenders, banks, and real estate investment firms looking to stay competitive. From intelligent document processing and predictive risk assessment to compliance-ready workflows and emerging AI agent capabilities, the opportunities extend far beyond simple automation.

The real challenge is not deciding whether to adopt AI. It is deciding how to implement it in a way that aligns with your lending model, compliance obligations, and long-term growth objectives.

At Biz4Group, we combine deep expertise in AI, financial workflows, and enterprise software engineering to help organizations build underwriting platforms that are practical, scalable, and built for real-world lending operations. As a leading custom software development company backed by specialized AI consulting services, we help businesses move from ideas and prototypes to production-ready underwriting solutions with confidence.

With 20+ years of experience, 1,000+ projects delivered, 750+ clients served, and an 85% client retention rate, our team understands what it takes to build scalable, compliant, and future-ready AI solutions for complex business environments.

The next underwriting advantage may already be sitting in your backlog. It might be time to give it a promotion.

Organizations that require custom underwriting workflows, proprietary risk models, or deep integrations often choose custom development. Off-the-shelf platforms may offer faster deployment but can limit flexibility, customization, and long-term control.

The cost of AI real estate underwriting software development typically ranges from $25,000 to $250,000+, depending on platform complexity, AI capabilities, compliance requirements, integrations, and scalability expectations.

A basic MVP can often be developed in 2 to 4 weeks, while a fully featured underwriting platform may require 6 to 8 weeks. The timeline depends on data availability, feature scope, compliance requirements, and integration complexity.

ROI varies by lending volume and operational efficiency goals. Many lenders invest in real estate underwriting automation to reduce manual review time, improve underwriting consistency, accelerate loan approvals, and increase deal throughput.

Yes. Most modern real estate AI underwriting platforms can integrate with loan origination systems, CRMs, banking platforms, credit bureaus, document management systems, and third-party property data providers through APIs.

Yes. A properly designed platform can support commercial real estate loans, residential mortgages, bridge financing, construction loans, and portfolio underwriting while applying different risk models and decision rules to each lending product.

No. The more realistic future is a collaborative model where AI agents automate data collection, analysis, verification, and workflow coordination while human underwriters retain responsibility for judgment, exceptions, and final lending decisions.

Our website require some cookies to function properly. Read our privacy policy to know more.