info@biz4group.com

info@biz4group.com

Imagine a digital system that doesn’t wait for instructions but instead, understands your business goals, learns from real-time feedback, and takes independent actions to get the job done.

Read More

AI Summary Powered by Biz4AI

AI Summary Powered by Biz4AI

Why are businesses still losing customers at the final step of a digital purchase when the right protection could have been offered instantly?

The answer often lies in disconnected insurance experiences that force customers into separate journeys while businesses miss valuable revenue opportunities. At the same time, tightening reinsurance terms and rising loss ratios have widened the global P&C protection gap to $183 billion, making accessible insurance distribution more important than ever.

This is exactly why embedded insurance API development is becoming a priority for companies building digital products.

If you're planning to offer insurance within your app or platform, the goal isn't just adding another feature. It's creating a buying experience that feels natural, keeps customers engaged, and opens a new revenue opportunity. Growing demand for customer-centric digital experiences is already reshaping the market, with embedded insurance premiums projected to exceed $722 billion globally by 2030.

Before you move forward, you probably have practical questions which might sound like:

Well, this guide is built to answer these questions step by step, helping you understand the decisions, development process, and business considerations before you build an embedded insurance API platform.

Let's dive in.

An embedded insurance API is a set of software interfaces that allows businesses to offer insurance products directly within their websites, mobile apps, or digital platforms. Instead of redirecting customers to an insurance provider, the API connects your platform with insurers, so insurance quotes, policy purchases, and related services become part of the same customer journey.

To help you understand the concept better, let's break it into two parts:

When these two concepts come together, businesses can introduce relevant insurance products exactly when customers are ready to make a decision. The result is a smoother buying experience, faster policy distribution, new revenue opportunities, and higher customer engagement without building an insurance ecosystem from scratch.

Now let's look at the core difference between traditional insurance and embedded insurance API:

Before planning an embedded insurance API development, it's worth answering one practical question: who is responsible for what? Every participant has a specific role, and each exchange of information serves a clear purpose. Understanding this flow helps you identify responsibilities, avoid data gaps, and create a smoother customer experience from the first interaction to policy management.

Once every participant understands their role, the entire process becomes easier to follow. Take a look:

Every participant contributes to a single customer journey, but they do not own the same information. Keeping customer, transaction, payment, and policy data with the appropriate owner improves governance, simplifies compliance, and creates a more reliable embedded insurance experience.

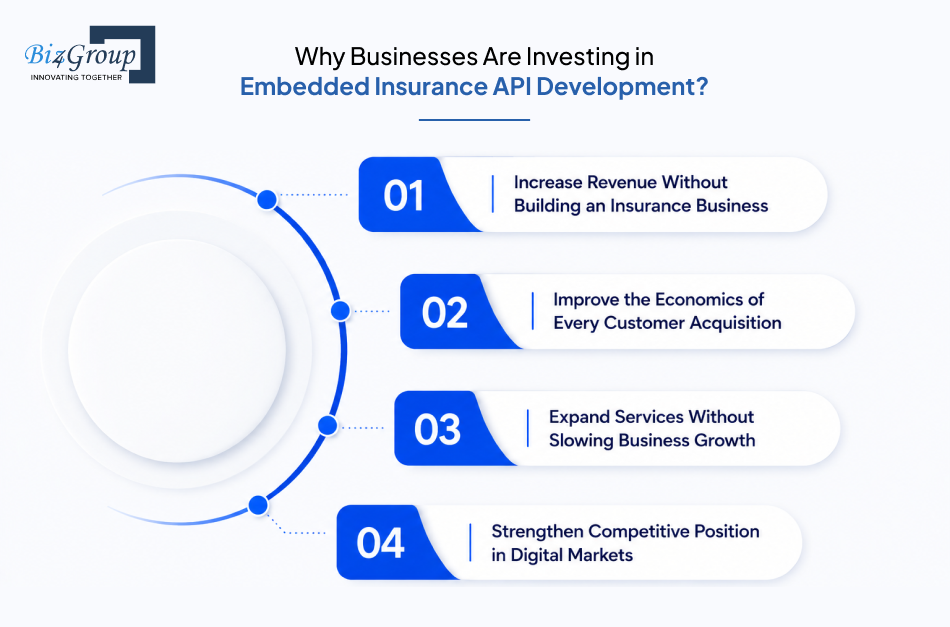

Businesses rarely approve technology investments because the technology is new. They invest when it helps improve revenue, increase the value of existing customers, enter new markets faster, or strengthen their competitive position.

The growing interest in embedded insurance API development follows the same pattern. Companies are investing because it creates measurable commercial outcomes that are difficult to achieve through traditional insurance distribution.

One of the strongest reasons businesses are investing is the opportunity to generate additional revenue from transactions that already exist. Instead of introducing a new product line, hiring insurance specialists, or becoming an insurance carrier, businesses can expand the commercial value of their existing products by offering relevant insurance at the point of purchase.

This is becoming a significant revenue channel rather than a niche opportunity. McKinsey projects that by 2030, nearly 25% of all personal lines premiums could be purchased through embedded propositions, representing more than $700 billion in gross written premiums across the P&C market.

Winning a customer is expensive. Naturally, businesses want every successful acquisition to generate more value instead of simply increasing customer volume. Developing embedded insurance technology solutions support the objective by creating another monetization opportunity within the same customer relationship, allowing businesses to improve revenue without proportionally increasing acquisition costs.

That commercial shift is also reflected in distribution trends. Online and API-led distribution represented 76.38% of the embedded insurance market in 2025 and is projected to grow at a 23.35% CAGR through 2031, indicating that businesses increasingly view digital distribution as the most commercially scalable model.

Launching new business offerings often requires additional operational capabilities, regulatory expertise, and long development cycles. Embedded insurance API development allows businesses to broaden their customer offering through strategic partnerships instead of building every capability internally. This shortens expansion timelines while allowing companies to remain focused on their primary products and services.

When competing businesses offer similar products, the overall customer experience often becomes the deciding factor. Companies are investing in embedded insurance because it increases the value customers receive from a single purchase, making their platforms more attractive without competing solely on pricing.

The opportunity continues to expand across industries. Electronics protection accounted for 44.74% of embedded insurance product lines, while IoT-driven micro auto insurance is projected to grow at a 33.87% CAGR through 2031. This demonstrates that embedded insurance is creating commercial opportunities across an increasingly diverse range of markets.

Businesses investing in embedded insurance API development are responding to one fundamental business reality: extracting more value from existing customer journeys is often more profitable than relying solely on acquiring new customers. That commercial objective is driving investment decisions across industries and sets the foundation for the architectural decisions discussed in the next section.

See how embedded insurance can create new revenue opportunities without disrupting your existing customer journey.

Let's Map Your Insurance StrategyA strong architecture does more than organize software; it determines how easily your platform can support new insurance partners, launch additional products, and handle future business growth. Before you build API-first embedded insurance platform capabilities, understand what each layer is responsible for. Once those responsibilities are clearly separated, expanding the platform becomes far more manageable.

Rather than viewing the architecture as three technical layers, think of it as three business responsibilities working together to deliver one seamless insurance experience.

Every insurance journey starts here. This layer focuses on customer interactions and ensures insurance is presented at the right moment without interrupting the purchase experience. It is also where an API-first architecture for business agility delivers practical value by making it easier to introduce new insurance offerings while keeping the customer journey consistent.

Its primary responsibilities include:

Without this layer, customers would struggle to discover, understand, and purchase insurance naturally during their existing journey.

Once customer information is available, the platform must decide what happens next. This layer evaluates requests, applies business rules, and ensures every insurance request follows the correct process before reaching the insurer. Its role is not simply to move information; it makes sure every decision is accurate and consistent.

This layer is responsible for:

Without this layer, every insurer would need separate business logic, making the platform difficult to maintain and even harder to scale.

Every quote, policy, payment, and customer interaction generates information that remains valuable long after the purchase is complete. This layer protects that information and keeps it available for future business operations, customer support, reporting, renewals, and compliance activities.

Its responsibilities include:

Without this layer, policy information would become difficult to manage, reporting would lose accuracy, and long-term customer servicing would quickly become unreliable.

Each layer performs a different responsibility, but none of them operate independently.

This separation of responsibilities gives businesses far more flexibility than a single, tightly connected system. Teams can improve customer experiences, introduce new insurance partners, or update business rules without redesigning the entire platform.

Adding insurance to your digital platform is only one part of the journey. The bigger decision is how you connect with insurance partners as your business grows. The right integration strategy depends on your business goals, the number of insurance providers you plan to support, and the level of operational flexibility you need. Let's understand where each strategy fits when we develop embedded insurance API capabilities:

Working directly with a single insurance carrier gives you greater control over the customer experience and business relationship. It works well when your insurance offering is centered around one trusted provider.

Instead of connecting with every insurer individually, this strategy connects your platform to an insurance aggregator that already manages multiple carrier relationships.

Many insurers still operate with long-established internal systems. Middleware acts as a coordination layer that helps modern digital platforms communicate with those existing business systems without requiring a complete replacement.

As partner ecosystems expand, relying on a single integration model rarely remains practical. Many enterprise platforms combine direct carrier relationships for strategic insurance products while using aggregators or middleware for broader market coverage.

|

Your Business Situation |

Recommended Integration Strategy |

|---|---|

|

Working with one insurance carrier |

Direct Carrier Integration |

|

Offering policies from multiple insurers quickly |

Aggregator-Based Integration |

|

Connecting with insurers using legacy systems |

Middleware-Based Integration |

|

Expanding across products, markets, and insurance partners |

Hybrid Integration Strategy |

Every integration strategy solves a different business challenge. The strongest platforms aren't built around the most complex integration model they're built around the one that supports current business goals while leaving room to grow.

Scalability isn't determined by the technologies you select; it starts with the decisions you make before writing the first line of code. The way your APIs are designed affects partner onboarding, future enhancements, maintenance effort, and long-term platform stability. Before you build embedded insurance API with REST APIs, GraphQL, and microservices, establish the design principles that will support your business as it grows.

Every decision below influences how your platform performs over time, so treat them as long-term business choices rather than short-term technical preferences.

Every API serves a specific audience. An API built for insurance carriers may not meet the needs of merchant platforms or internal business teams. Defining the primary consumers first makes every design decision more consistent.

Focus on:

The way data is delivered directly affects performance, flexibility, and partner experience. Rather than starting with a technology, begin by understanding how consumers expect to receive information.

Consider these decisions:

Not every function grows at the same pace. Quote requests may increase rapidly while policy servicing remains stable. Separating critical business capabilities allows individual services to evolve without affecting the entire platform.

Evaluate whether your platform should:

Microservices become valuable when business capabilities need to grow independently rather than together.

Every embedded insurance platform changes over time. New insurers join, products expand, and regulations evolve. Planning for those changes early prevents unnecessary disruption later.

Important design decisions include:

Before finalizing your API strategy, we suggest that you ask these questions:

Answering these questions first leads to architecture decisions that remain practical as your platform evolves instead of becoming expensive to redesign later. This approach also strengthens insurtech API development projects by reducing technical debt before it becomes a business problem.

Turn architecture choices into a platform that stays flexible as partners, products, and business needs grow.

Discuss Your API Blueprint

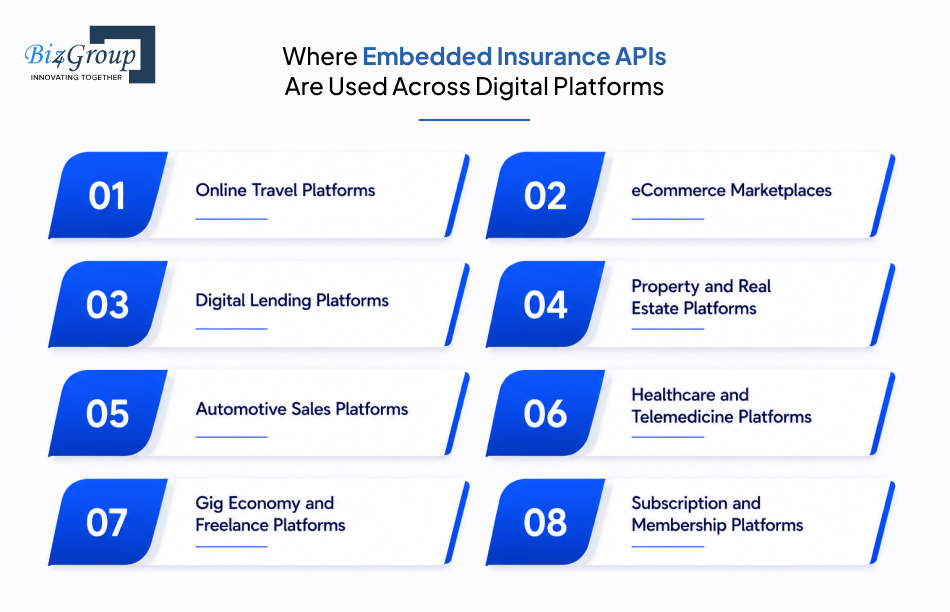

The value of embedded insurance isn't tied to a specific industry, rather it depends on the digital experience your platform delivers. Whenever customers make financial commitments, book services, or purchase high-value products, insurance becomes a natural extension of that journey. Businesses looking to make embedded insurance API for digital platforms successful should start by identifying where protection adds value instead of interrupting the customer experience.

The following examples show how different digital platforms use embedded insurance to solve specific business and customer needs.

Travel plans often involve uncertainties such as trip cancellations, medical emergencies, or lost baggage. Presenting travel insurance during the booking process allows customers to secure coverage without leaving the platform. At the same time, travel businesses create an additional revenue opportunity while improving booking confidence.

Many online purchases involve products that customers want to protect after checkout. Embedded insurance API development allows marketplaces to offer warranty extensions, accidental damage protection, or shipping coverage at the moment customers complete their purchase. The experience remains part of the same transaction instead of becoming a separate decision later.

Also Read: Guide to AI Insurance Marketplace Development

Customers applying for personal loans, vehicle financing, or business credit often require insurance linked to the financed asset or loan agreement. Embedded insurance APIs enable lending platforms to include relevant protection within the application journey, reducing manual coordination while simplifying the borrowing experience.

Buying or renting property usually involves multiple service providers and significant financial commitments. Property platforms can introduce home insurance, tenant insurance, or landlord coverage alongside property transactions, helping customers complete more of the process through one digital experience.

Vehicle purchases naturally create demand for motor insurance. Embedded insurance allows dealerships and online automotive marketplaces to present policy options during the buying process, giving customers the convenience of completing both the vehicle purchase and insurance selection together.

Also Read: AI Vehicle Damage Detection Software Development

Patients using digital healthcare services may benefit from insurance products related to consultations, treatments, or ongoing care plans. Offering relevant coverage within the healthcare journey simplifies access to financial protection without adding unnecessary administrative steps.

Also Read: How to Develop an AI Health Insurance App

Independent workers frequently move between projects, clients, and locations. Embedded insurance helps gig platforms offer coverage such as personal accident, equipment, or liability insurance directly within worker onboarding or project management, making protection easier to access as work arrangements change.

Subscription-based businesses often provide products or services that customers use continuously. Embedded insurance can be offered as an optional value-added service, helping businesses strengthen customer relationships while creating recurring insurance opportunities alongside existing subscriptions.

The strongest embedded insurance strategies don't begin with the insurance product they begin with the customer journey. Identifying the right touchpoint within each platform creates a more relevant buying experience, improves customer engagement, and turns insurance into a natural part of the overall digital service rather than an afterthought.

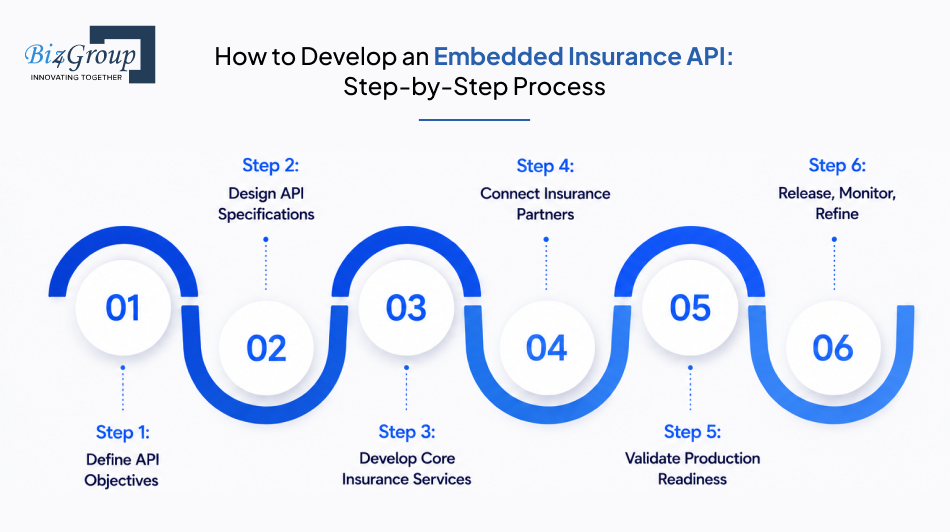

A successful embedded insurance platform comes from following the right implementation sequence rather than solving technical problems as they appear. Every stage prepares the next one, helping your team deliver reliable insurance services without unnecessary rework. Here's the development process most enterprise projects follow from planning through production.

Every development effort should begin with a clear API specification. Decide what insurance products your platform will support, which customer actions will trigger insurance offers, and which business outcomes the APIs must deliver. This stage also establishes the functional scope before implementation begins.

Document the following:

Once the scope is finalized, convert business requirements into detailed API specifications. This stage defines how information moves between participants and how every service behaves before development starts.

Your API specification should include:

This is where the actual implementation begins. Every service should be developed independently while following the API specifications prepared earlier. Keeping business services modular also makes future enhancements much easier during embedded insurance API development.

The first release typically includes:

Core services become valuable only after they communicate with the external business ecosystem. This stage focuses on implementing every required connection while validating that information is exchanged accurately across participating systems.

Complete integrations for:

Before releasing the platform, verify that every business scenario performs as expected under real operating conditions. The objective is to confirm reliability, security, and business accuracy rather than simply checking whether the APIs respond.

Validate scenarios including:

Deployment marks the beginning of continuous improvement. Monitor platform performance, collect operational insights, and introduce enhancements based on customer behavior, partner feedback, and evolving insurance requirements.

Track and improve:

|

Phase |

Primary Deliverable |

Outcome |

|---|---|---|

|

API Objectives |

Approved functional requirements |

Clear implementation scope |

|

API Specifications |

Complete API blueprint |

Development-ready design |

|

Core Services |

Working insurance APIs |

Functional business capabilities |

|

Partner Connectivity |

Integrated insurance ecosystem |

End-to-end business flow |

|

Production Validation |

Verified business scenarios |

Release-ready platform |

|

Continuous Improvement |

Performance insights and enhancements |

Scalable long-term operations |

A structured implementation process keeps every stage focused on a measurable outcome instead of isolated development tasks. Following this sequence gives your team a stronger foundation for delivering embedded insurance APIs that remain reliable, scalable, and easier to enhance as business needs evolve.

The technologies you select should support the responsibilities of an embedded insurance API throughout its lifecycle from processing quote requests and issuing policies to securing customer data and connecting with insurance partners. While there is no universal technology stack, the recommendations below represent enterprise-proven tools commonly used when building embedded insurance API ecosystem solutions.

|

Technology Area |

Recommended Tools |

Purpose |

|---|---|---|

|

API Development |

Spring Boot, ASP.NET Core, NestJS, FastAPI |

Develop secure, scalable APIs that manage quotes, policies, customer information, and other insurance operations. |

|

API Gateway |

Kong, Apigee, AWS API Gateway, Azure API Management |

Control API traffic, secure partner access, manage rate limits, and simplify API management through a centralized gateway. |

|

API Communication |

REST APIs, GraphQL |

Exchange information between merchant platforms, insurers, and business partners using standardized communication methods. |

|

Authentication & Authorization |

OAuth 2.0, JWT, Auth0, Okta |

Verify user identities and ensure only authorized users and systems can access insurance services. |

|

Business Rules Engine |

Drools, Camunda DMN, OpenL Tablets |

Manage eligibility rules, underwriting logic, pricing conditions, and policy validation without changing application code. |

|

Partner Connectivity |

REST Connectors, Apache Kafka, RabbitMQ |

Connect with insurers and external business systems while supporting both synchronous and event-driven communication. |

|

Identity Verification |

Trulioo, Onfido, Persona |

Verify customer identities to support regulatory compliance and reduce fraudulent policy applications. |

|

Payment Processing |

Stripe, Adyen, Checkout.com, Braintree |

Process insurance premium payments securely before confirming policy issuance. |

|

Data Storage |

PostgreSQL, MongoDB |

Store customer profiles, policy information, transaction history, and insurance records securely. |

|

Caching |

Redis |

Improve API response times by temporarily storing frequently requested information such as quote results and product details. |

|

API Documentation |

OpenAPI (Swagger), Postman |

Generate clear API documentation that simplifies partner onboarding, testing, and ongoing maintenance. |

|

Notifications |

Twilio, SendGrid, Firebase Cloud Messaging |

Deliver policy confirmations, payment notifications, renewal reminders, and other customer communications across multiple channels. |

|

Monitoring & Observability |

Datadog, Prometheus, Grafana |

Monitor API performance, service availability, and operational health to identify issues quickly. |

|

Logging & Audit Trails |

ELK Stack (Elasticsearch, Logstash, Kibana), Splunk |

Record business events and system activity to support troubleshooting, compliance, and audit requirements. |

|

Security Protection |

Cloudflare, AWS WAF, HashiCorp Vault |

Protect APIs, encryption keys, and sensitive insurance data from unauthorized access and cyber threats. |

|

Cloud Infrastructure |

AWS, Microsoft Azure, Google Cloud Platform |

Provide reliable, scalable infrastructure capable of supporting enterprise-grade embedded insurance API workloads. |

The recommended technologies above are widely adopted across enterprise API ecosystems, but the final stack should always reflect your business goals, integration requirements, compliance obligations, expected transaction volume, and internal engineering expertise. Selecting tools based on platform responsibilities creates a stronger foundation for reliable integrations, secure policy services, and long-term scalability.

Every insurance transaction involves sensitive customer and policy information. Protecting that information requires more than adding security features at the end of the project. During digital insurance API development, security, compliance, and regulatory requirements should be addressed throughout the implementation process, so every API request and partner connection follows the same protection standards.

The considerations below highlight the areas that deserve attention before moving your platform into production.

Every API request should exchange only the information required to complete the insurance process. Limiting unnecessary data sharing reduces security risks while supporting privacy obligations across different markets.

Protect customer information by:

Embedded insurance platforms often communicate with insurers, payment providers, and identity verification services. Every connection should have clearly defined permissions so each participant accesses only the information required for its responsibilities.

Access controls should include:

Compliance becomes easier when business processes are designed around regulatory expectations instead of treating them as a final project task. Insurance regulations, privacy requirements, and customer consent should remain part of every transaction from the beginning.

Key compliance considerations include:

Insurance transactions often require organizations to demonstrate how information was collected, processed, and shared. Maintaining detailed audit records improves operational transparency while supporting regulatory reviews and internal governance.

Maintain records for:

Security continues after production deployment. Continuous monitoring helps identify unusual activity, integration failures, and operational risks before they affect customers or business partners. As API traffic grows, many organizations also adopt AI automation services to detect anomalies, prioritize security alerts, and respond to potential threats more efficiently.

Ongoing monitoring should focus on:

Also Read: 10 AI Automation Use Cases for Enterprises to Scale Faster

Strong security comes from making protection part of the development process rather than treating it as a final checkpoint. Addressing these considerations early helps embedded insurance APIs operate more reliably, simplifies compliance efforts, and builds greater confidence among customers, insurers, and business partners.

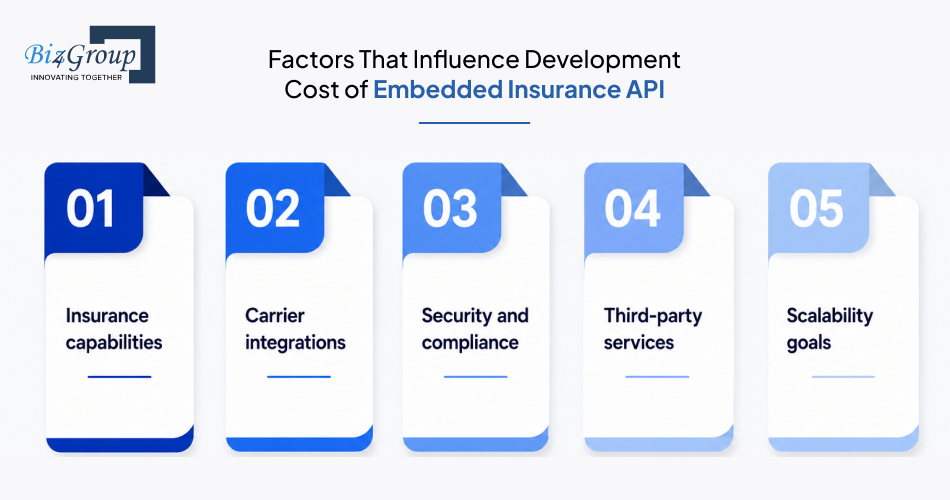

Budget planning becomes much easier when you understand what you're paying for before development begins. The total investment depends on platform capabilities, insurance partner integrations, security requirements, and long-term scalability.

While every project has unique business goals, the overall cost for embedded insurance API development ranges between $10,000 to $150,000+. The table below outlines typical development costs based on the scope of the embedded insurance API platform and the capabilities included in each implementation.

|

Platform Scope |

Estimated Cost |

Typical Timeline |

|---|---|---|

|

Basic Embedded Insurance API Platform |

$10,000 – $30,000 |

2–4 Weeks |

|

Moderate Embedded Insurance API Platform |

$30,000 – $75,000 |

4–8 Weeks |

|

Advanced Embedded Insurance API Platform |

$75,000 – $150,000+ |

8–16+ Weeks |

The estimated cost grows as additional insurance capabilities, integrations, and operational requirements become part of the platform.

Suitable for businesses introducing a single insurance offering with limited integration requirements.

Includes:

Designed for businesses expanding insurance offerings across multiple products and business partners.

Includes:

Designed for enterprise platforms supporting large transaction volumes and complex insurance ecosystems.

Includes:

The final project budget depends on implementation requirements rather than the number of APIs alone. Businesses planning to create embedded insurance API solution should evaluate these factors before estimating development effort.

Launching the platform is only the first stage of the investment. Continuous operations help maintain platform reliability, security, and partner connectivity.

|

Operational Activity |

Estimated Monthly Cost |

|---|---|

|

Cloud Infrastructure |

$500 – $5,000 |

|

API Monitoring & Logging |

$200 – $2,000 |

|

Security Updates & Compliance |

$1,000 – $5,000 |

|

Platform Support & Enhancements |

$2,000 – $10,000 |

A realistic budget comes from matching platform capabilities with business objectives instead of estimating the number of APIs to be developed. Defining the right scope early helps prioritize investments, reduce unnecessary implementation costs, and create an embedded insurance platform that remains ready for future expansion.

Get a realistic cost estimate based on your platform scope, integration needs, and business objectives.

Request My Cost Estimate

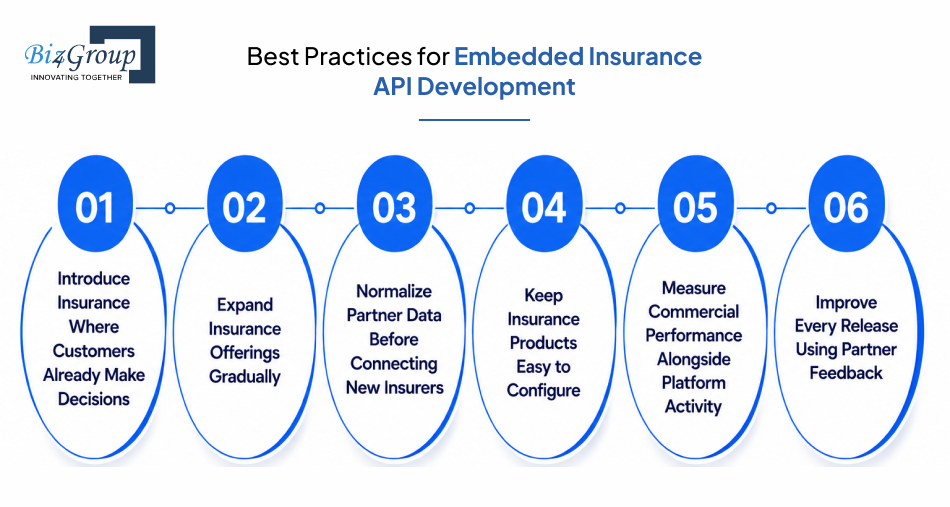

Successful embedded insurance platforms are shaped by practical implementation decisions that improve customer adoption, simplify partner collaboration, and support long-term business growth. The recommendations below reflect proven practices followed across successful embedded insurance API development projects without repeating earlier technical considerations.

Present insurance during existing purchase or booking journeys instead of creating separate buying flows. Natural placement increases policy adoption, reduces purchase friction, and makes insurance feel like part of the overall customer experience.

Launch with one insurance product and a limited number of carrier partnerships before expanding your ecosystem. A phased rollout simplifies implementation, improves operational stability, and creates a stronger foundation for future product growth.

Establish a consistent internal data model before integrating additional insurance providers. Standardized information reduces integration complexity, shortens onboarding time, and allows new partners to connect without disrupting existing business operations.

Business teams should be able to introduce new coverage options, pricing rules, and policy updates without extensive redevelopment. Configurable insurance products reduce release cycles and help platforms respond quickly to changing market opportunities.

Evaluate quote acceptance, policy conversions, partner participation, and customer engagement alongside operational metrics. Many organizations also adopt AI integration services to identify purchasing trends and uncover opportunities that improve embedded insurance performance.

Review feedback from insurance carriers, merchants, and business stakeholders after each release instead of waiting for major platform updates. Continuous refinement strengthens partner relationships, improves operational efficiency, and supports sustainable platform growth.

Embedded insurance API development deliver long-term value through continuous refinement rather than one-time implementation. Applying these practices throughout the development lifecycle helps teams improve customer adoption, simplify partner expansion, and achieve stronger business outcomes as the ecosystem grows.

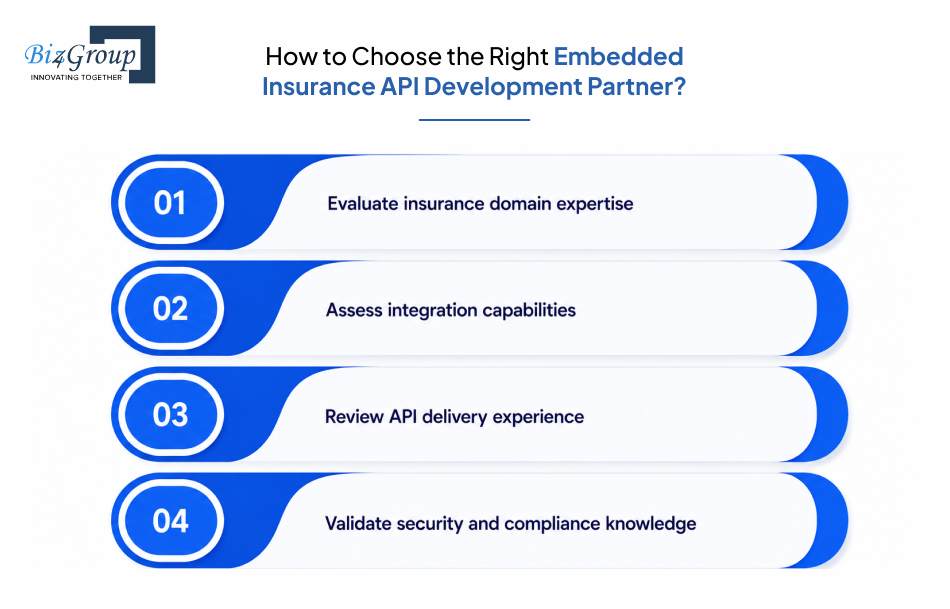

The success of your platform depends as much on the implementation partner as the technology itself. An experienced partner should understand insurance ecosystems, API integrations, regulatory expectations, and long-term platform scalability. Before starting your embedded insurance API development project, evaluate potential partners using the criteria below.

Review whether the company has experience delivering insurance APIs, embedded finance solutions, or platforms involving carrier integrations rather than only general API projects.

Confirm the team can integrate multiple insurance carriers, payment providers, identity verification services, and other third-party business systems without increasing implementation complexity.

Ask for examples of API-first platforms, documentation quality, integration workflows, and partner onboarding processes that demonstrate practical implementation experience.

Ensure the partner understands data privacy requirements, audit readiness, authentication standards, and regulatory expectations applicable to insurance APIs.

Look beyond initial delivery. A reliable partner should also provide platform enhancements, performance optimization, maintenance, and support as your insurance ecosystem grows.

Finding the right partner becomes easier when technical expertise is supported by real implementation experience. Biz4Group LLC, a software development company in USA, has 20+ years of expertise delivering enterprise software, AI-powered platforms, and API-driven digital solutions. Instead of providing one-size-fits-all implementations, the team works closely with businesses to align technical decisions with commercial objectives.

Depending on your project requirements, Biz4Group can help with:

The right development partner should strengthen both your technology strategy and your long-term business goals. Evaluating industry expertise, integration experience, and implementation capabilities before the project begins helps reduce delivery risks and creates a stronger foundation for a successful embedded insurance platform.

Embedded insurance works best when every decision supports the way your business operates, from carrier integrations and API design to security, scalability, and future expansion. That is exactly why embedded insurance API development deserves careful planning instead of rushing into implementation. Getting these decisions right early helps reduce unnecessary rework, simplifies partner onboarding, and creates a platform that is easier to manage as your insurance ecosystem grows.

Planning your platform is one thing. Turning that plan into a reliable implementation is another. Working with an experienced technology partner helps you move forward with greater clarity, fewer implementation challenges, and a roadmap that fits your business objectives.

At Biz4Group LLC, we work closely with businesses to design and develop embedded insurance API platforms that match real operational needs rather than generic implementation templates. So, if you have an embedded insurance idea in mind? Let's discuss your requirements and identify the right development approach for your platform.

Yes. Most enterprise platforms are designed to connect with multiple insurance carriers through a single API layer. This allows businesses to offer different insurance products, compare carrier responses, and expand partnerships without rebuilding the entire platform whenever a new insurer is added.

The cost of embedded insurance API development typically ranges from $10,000 to $150,000+, depending on platform scope, the number of carrier integrations, security requirements, compliance obligations, and the level of business automation required. Enterprise platforms with multiple insurer integrations and advanced workflows usually require a higher investment.

Development timelines generally range from 2 weeks to 16+ months. A basic implementation with limited integrations can be completed faster, while enterprise platforms supporting multiple insurers, complex policy workflows, regulatory compliance, and extensive testing require a longer implementation timeline.

Yes. In most cases, embedded insurance APIs are designed to integrate with existing platforms through well-defined interfaces. Whether you operate a fintech platform, eCommerce marketplace, travel portal, or mobility solution, insurance capabilities can usually be added without replacing your existing application.

Before development begins, define your insurance products, identify carrier partners, document customer journeys where insurance will be offered, determine compliance requirements, and establish clear business objectives. Preparing these decisions early helps reduce implementation delays and improves overall project planning.

Most businesses expand gradually by adding new insurance products, onboarding additional carriers, supporting new customer channels, and introducing automation where it creates measurable value. Planning for future expansion during the initial implementation makes these enhancements easier and more cost-effective.

Our website require some cookies to function properly. Read our privacy policy to know more.