info@biz4group.com

info@biz4group.com

Imagine a digital system that doesn’t wait for instructions but instead, understands your business goals, learns from real-time feedback, and takes independent actions to get the job done.

Read More

ACH payments remain one of the most important ways businesses move money in the United States. From payroll and vendor payments to subscriptions and B2B transactions, ACH processing sits at the center of many financial operations. But as transaction volumes increase and payment workflows become more complex, traditional ACH systems often struggle to keep pace with growing demands around fraud prevention, reconciliation, exception handling, and operational efficiency.

This challenge is driving interest in AI ACH payment processing software development. Organizations are exploring how artificial intelligence can help modernize payment operations, automate repetitive workflows, and improve decision-making across the ACH lifecycle. At the same time, software teams, fintech companies, banks, and enterprise payment leaders are facing important questions around architecture, compliance, implementation, and long-term scalability.

For organizations evaluating an AI ACH payment platform, building custom payment software, or modernizing existing infrastructure, understanding where AI fits into ACH processing has become increasingly important. The growing adoption of AI in payments industry initiatives and the continued expansion of digital financial services, including fintech in wealth management, are accelerating demand for more intelligent payment systems.

In this guide, we'll explore how AI ACH payment processing software works, where it creates value, the components required to build it, the technologies commonly used in development, and the key considerations for implementation, compliance, and growth.

AI ACH payment processing software combines traditional ACH payment processing with artificial intelligence capabilities that help businesses process payments more efficiently. The ACH network still handles the actual movement of money, while AI is used to improve activities such as fraud detection, payment monitoring, reconciliation, and payment optimization. In other words, AI helps organizations make better payment decisions without changing how ACH transactions are processed.

ACH payment processing is the process of transferring money through the Automated Clearing House network. A typical ACH payment processing system handles payment initiation, account validation, ACH file generation, payment submission, settlement tracking, return handling, and reconciliation. These functions form the foundation of any ACH payment platform and are required whether AI is used or not.

AI is not responsible for moving money. Its role is to analyze payment data and help improve the workflows that surround ACH processing.

Common AI use cases within ACH payment processing software include:

The goal is to reduce operational effort, improve payment outcomes, and help teams manage larger payment volumes without increasing manual workloads.

When building or evaluating an AI ACH payment platform, it's important to understand the difference between the payment system and the AI layer. The payment system is responsible for processing transactions, while AI is responsible for analyzing data and supporting operational decisions.

|

Payment Infrastructure |

AI Decisioning |

|---|---|

|

Processes ACH transactions. |

Analyzes transaction data. |

|

Generates ACH files. |

Predicts payment outcomes. |

|

Connects to banks and payment networks. |

Detects fraud and unusual activity. |

|

Handles settlement and returns. |

Optimizes retry timing and payment decisions. |

|

Enforces NACHA compliance requirements. |

Automates operational tasks and recommendations. |

In simple terms, payment infrastructure moves money, while AI helps determine the best way

to process, monitor, and manage those payments.

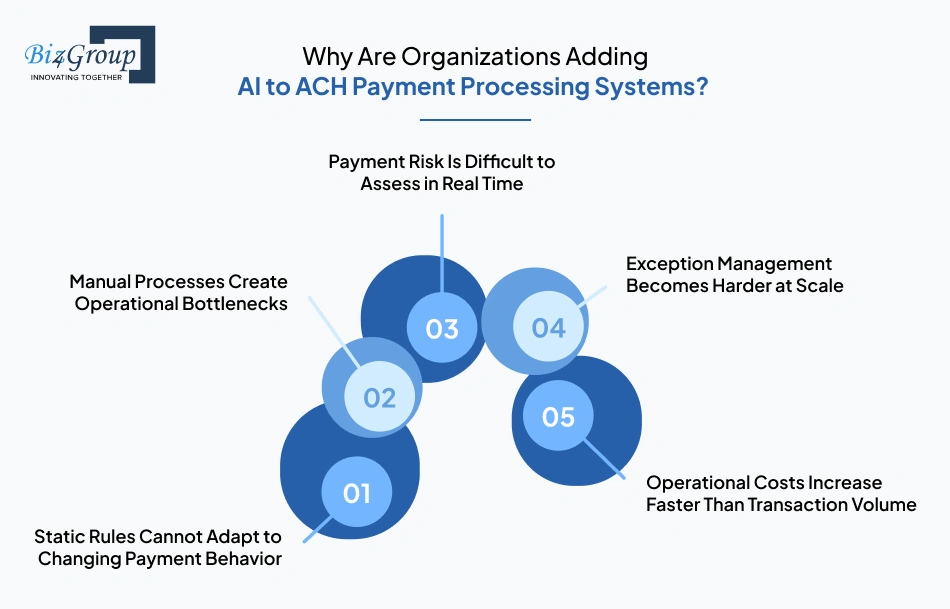

Organizations are adding AI to ACH payment processing systems because traditional ACH workflows often rely on static rules and manual work that become difficult to manage as payment volumes grow. AI helps businesses automate repetitive tasks, improve payment decisions, identify risks earlier, and handle larger transaction volumes without adding the same level of operational effort.

Most ACH payment systems use predefined rules for fraud checks, payment retries, and risk controls. These rules work well for known situations but struggle when customer behavior, transaction patterns, or fraud tactics change. AI can analyze new data continuously and adjust to changing conditions without requiring constant rule updates.

Many ACH payment teams still spend hours reviewing transactions, handling exceptions, investigating issues, and reconciling payments. As payment volumes increase, these tasks take up more time and slow down day-to-day operations. ACH payment automation software helps reduce the amount of manual work required to keep payment operations running efficiently.

Payment risk can change from one transaction to the next. Account activity, payment history, transaction amounts, and other signals can all affect the likelihood of fraud or payment failure. Traditional systems often rely on fixed thresholds, while AI can evaluate multiple signals at once and provide a more accurate view of risk.

Returns, failed payments, account validation problems, and reconciliation issues create exceptions that need to be reviewed and resolved. When ACH transaction volumes grow, these exceptions can quickly overwhelm payment teams. AI can help identify the most important issues first and reduce the time required to investigate them.

In many organizations, processing more ACH payments means hiring more people, performing more reviews, and spending more time on payment operations. As a result, costs often rise alongside transaction volume. AI ACH payment platforms help control these costs by automating routine tasks and reducing the need for manual intervention.

|

Traditional ACH Processing Systems |

AI-Enhanced ACH Processing Systems |

|---|---|

|

Depend on static business rules. |

Adapt to changing transaction patterns. |

|

Require significant manual review. |

Automate routine payment tasks. |

|

Assess risk using fixed thresholds. |

Continuously evaluate payment risk. |

|

Handle exceptions through manual queues. |

Prioritize exceptions based on importance and risk. |

|

Scale through additional staff and resources. |

Scale through automation and intelligent workflows. |

For fintech companies, banks, payment providers, and enterprise organizations, AI is

increasingly being used to make ACH payment processing more efficient and easier to scale. This is

one reason why AI ACH payment processing software development and broader enterprise AI solutions are

becoming an important part of modern payment operations.

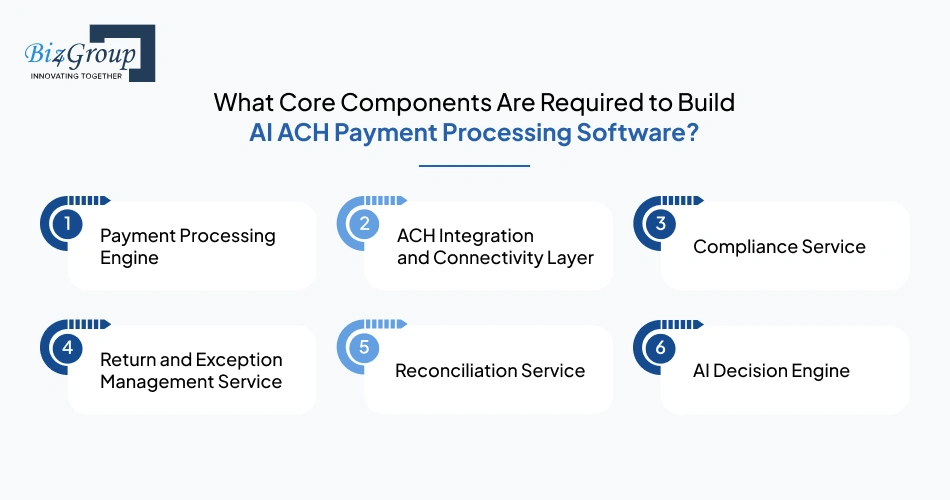

AI ACH payment processing software is usually built around six core components. Together, these components handle payment processing, bank connectivity, compliance, returns, reconciliation, and AI-driven decision-making. Whether you're building a custom AI ACH payment platform or modernizing an existing ACH payment system, these are the services that form the foundation of the platform.

|

Component |

Purpose |

|---|---|

|

Payment Processing Engine |

Handles payment requests, account validation, ACH file creation, transaction processing, and settlement tracking. |

|

ACH Integration and Connectivity Layer |

Connects the platform to banks, payment processors, FedACH infrastructure, and other payment networks. It manages file transfers, APIs, and communication between systems. |

|

Compliance Service |

Manages NACHA compliance requirements, payment authorizations, audit logs, fraud monitoring controls, and data retention policies. |

|

Return and Exception Management Service |

Handles ACH returns, failed transactions, return codes, payment exceptions, and recovery processes. |

|

Reconciliation Service |

Matches payments with settlement records, invoices, remittance data, and account balances to keep financial records accurate. |

|

AI Decision Engine |

Analyzes transaction data to support fraud detection, payment failure prediction, risk scoring, anomaly detection, and retry optimization. |

The first five components are responsible for running the ACH payment system. The AI

decision engine uses the data generated by those services to improve how payments are monitored,

reviewed, and managed. This layered approach is commonly used when building custom AI ACH payment

software because it allows organizations to establish a reliable, NACHA-compliant ACH processing

foundation before introducing intelligence through AI integration services.

Build a custom AI ACH payment processing platform that automates fraud detection, reconciliation, and payment decision-making.

Discuss Your Platform Requirements

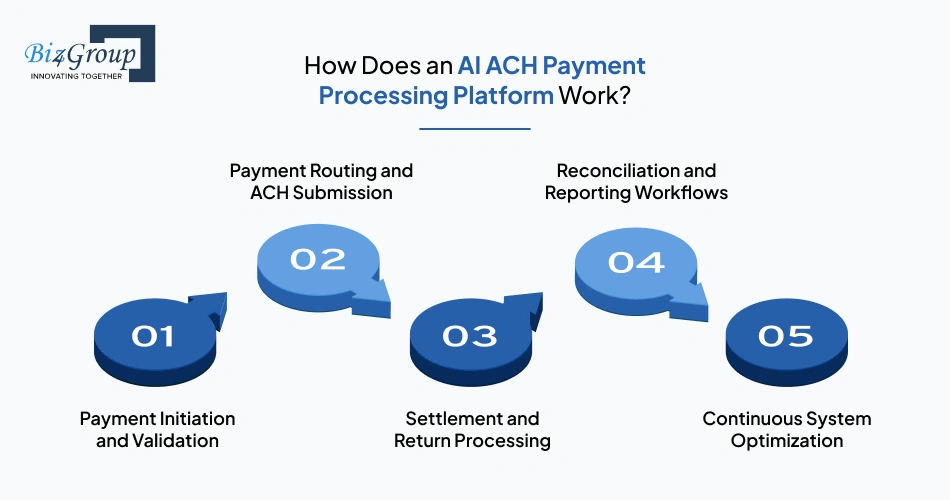

An AI ACH payment processing platform follows the same payment flow as a traditional ACH system. The ACH network still moves and settles funds, while AI helps improve the decisions made throughout the process. This includes tasks such as fraud detection, payment risk assessment, exception handling, reconciliation, and payment optimization.

|

Stage |

What Happens |

|---|---|

|

Payment Initiation and Validation |

The platform receives a payment request, validates account and transaction details, confirms authorization requirements, and performs initial fraud and risk checks. |

|

Payment Routing and ACH Submission |

Approved transactions are grouped, converted into ACH files, and submitted through bank and payment network connections. This stage may also support same day ACH processing. |

|

Settlement and Return Processing |

The platform tracks settlement status, monitors transaction outcomes, and processes ACH return codes, failed payments, and rejected transactions. |

|

Reconciliation and Reporting Workflows |

Payment records, settlement data, invoices, and remittance information are matched automatically to keep financial records accurate and up to date. |

|

Continuous System Optimization |

The AI layer analyzes payment results, fraud signals, return patterns, and reconciliation data to improve future payment decisions and automate routine tasks. |

The biggest difference between a traditional ACH payment system and an AI-powered ACH

payment platform is that the system continuously learns from payment activity. Over time, it can

improve fraud detection, identify payment risks earlier, automate more operational work, and help

teams manage growing transaction volumes more efficiently without changing how ACH payments are

processed. These improvements are typically driven by ongoing AI model development using

transaction, settlement, and operational data collected across the payment lifecycle.

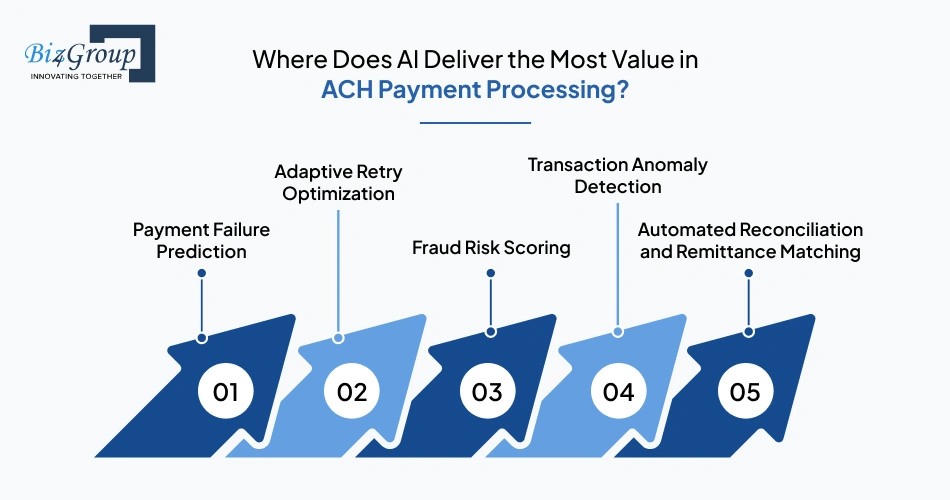

AI delivers the most value in ACH payment processing by helping businesses reduce failed payments, detect fraud earlier, automate manual work, and improve payment operations. These are the areas where traditional ACH systems often struggle as transaction volumes grow.

AI can analyze historical transaction data, account activity, and return patterns to identify payments that are more likely to fail before they are submitted. This gives businesses an opportunity to take corrective action and reduce avoidable ACH returns.

Many ACH systems retry failed payments using fixed schedules. AI can determine when a retry is most likely to succeed based on previous payment activity, customer behavior, and historical outcomes. This helps improve recovery rates while reducing unnecessary retries.

AI can evaluate multiple fraud signals at the same time, including transaction activity, account behavior, payment velocity, and historical patterns. This helps payment teams identify high-risk transactions more accurately than relying on static rules alone. Fraud risk scoring is also one of the most common use cases discussed during AI consulting services engagements focused on payment systems.

Some suspicious transactions do not match known fraud rules. AI can identify unusual transaction behavior that falls outside normal patterns, helping teams detect potential fraud, account misuse, and other issues earlier.

A common question from finance teams is: "our AP team is manually matching ACH payments to invoices every single day and it is taking hours and causing errors, someone told me we can build or buy software that uses AI to do this automatically, i want to understand what that software actually looks like under the hood, what AI models power the matching, and whether it makes more sense to build it custom or find a vendor who already has this"

The answer is that modern AI ACH payment platforms use machine learning models to match payments, invoices, remittance records, and settlement data based on transaction details, payment history, reference information, and historical matching patterns. This allows much of the reconciliation process to be automated, reducing manual work and improving accuracy. This capability is becoming increasingly important for organizations looking to build AI fintech app solutions that support high-volume payment operations.

|

AI Use Case |

Business Value |

|---|---|

|

Payment Failure Prediction |

Reduces ACH returns and improves payment success rates. |

|

Adaptive Retry Optimization |

Improves recovery of failed payments and reduces unnecessary retries. |

|

Fraud Risk Scoring |

Strengthens fraud prevention and improves risk management. |

|

Transaction Anomaly Detection |

Identifies unusual transaction activity earlier. |

|

Automated Reconciliation and Remittance Matching |

Reduces manual work and improves financial accuracy. |

For most organizations, AI creates the greatest value when applied to repetitive, data-heavy

payment workflows where better decisions and greater automation can directly improve operational

efficiency. These use cases are often the first areas targeted in AI ACH payment processing

software development projects because they can deliver measurable improvements without changing the

underlying ACH payment infrastructure.

A modern AI ACH payment processing platform combines payment processing, bank connectivity, compliance controls, data management, and AI capabilities into a system that can process ACH transactions reliably while supporting intelligent decision-making.

At the center of the architecture are the services responsible for payment processing. These include payment initiation, ACH file generation, bank connectivity, return handling, reconciliation, reporting, and compliance management. Each service is responsible for a specific part of the ACH payment lifecycle and works with other services to complete end-to-end transaction processing.

Most modern ACH payment platforms use an event-driven architecture. Actions such as payment creation, ACH submission, settlement updates, return events, and reconciliation updates generate events that other services can process independently. This approach improves scalability, reduces dependencies between services, and makes it easier to handle growing transaction volumes. It is commonly used in large-scale payment systems, including money transfer app development projects that process high transaction volumes.

Many organizations modernizing legacy payment systems ask: "our bank is still running legacy ACH infrastructure and we are getting killed on manual exception handling and return rates, we want to modernize and add AI to the system but we dont know if we should build from scratch or bolt AI onto what we have, what are the pros and cons and what would the new architecture look like if we rebuilt it properly"

A modern architecture typically separates transaction processing from AI decision-making. Payment events, settlement records, return data, fraud signals, and reconciliation information are collected in a centralized data layer. The AI decision engine uses this data to support fraud detection, payment failure prediction, anomaly detection, adaptive retry optimization, and automated reconciliation.

Security and compliance controls are built into every part of the platform. ACH payment software architecture typically includes encryption, access controls, audit logging, authorization management, transaction monitoring, and NACHA compliance controls. Designing and maintaining these controls often requires teams to hire AI fintech software developers with experience in payment security, compliance, and ACH infrastructure.

Together, these components create a layered architecture where payment processing, bank integrations, data management, AI capabilities, and compliance controls operate independently but work together as a single system. This approach makes AI ACH payment processing software easier to scale, maintain, and update as transaction volumes and business requirements grow.

Develop secure AI ACH payment processing software with bank integrations, compliance controls, and intelligent automation built in.

Plan My ACH PlatformAI ACH payment processing software needs a mix of core payment features and AI-powered capabilities. The core features are responsible for moving money, managing compliance, and connecting to banks, while AI features help reduce failed payments, detect fraud, automate reconciliation, and improve payment operations.

|

Feature |

Purpose |

|---|---|

|

Payment Initiation and Processing |

Creates, validates, and processes ACH debit and credit transactions. |

|

ACH File Generation and Submission |

Generates NACHA-compliant ACH files and submits them to banks and payment networks. |

|

Bank and Payment Network Integration |

Connects the platform to banks, payment processors, FedACH infrastructure, and other payment systems. |

|

Same Day ACH Support |

Supports eligible ACH transactions that require faster settlement. |

|

Return and Exception Management |

Handles ACH return codes, failed payments, rejected transactions, and exception cases. |

|

Compliance and Audit Controls |

Manages authorization records, audit logs, transaction monitoring, and NACHA compliance requirements. |

|

Payment Failure Prediction |

Uses AI to identify transactions that are likely to fail before they are processed. |

|

Risk Scoring and Fraud Detection |

Uses AI to identify suspicious transactions, unusual activity, and potential fraud risks. |

|

Adaptive Retry Optimization |

Uses payment history and transaction outcomes to determine the best retry timing for failed payments. |

|

Automated Reconciliation and Remittance Matching |

Matches payments with invoices, settlement records, and remittance data while reducing manual work. |

|

Reporting and Operational Analytics |

Tracks transaction activity, return rates, reconciliation status, and payment performance. |

Not every organization needs every AI feature on day one. Most successful AI ACH payment

processing software development projects start with reliable payment processing, compliance,

returns management, and bank connectivity. AI capabilities such as fraud detection, payment failure

prediction, adaptive retries, and reconciliation automation are typically added to improve

efficiency as payment volumes and operational complexity increase.

Many teams beginning AI ACH payment processing software development ask: "i need to build an ACH payment system for our fintech platform and i want to add AI to it but i have no idea where to start, can you walk me through what the architecture should look like, what components i need, and what tech stack makes sense for a US based company that needs to be NACHA compliant from day one"

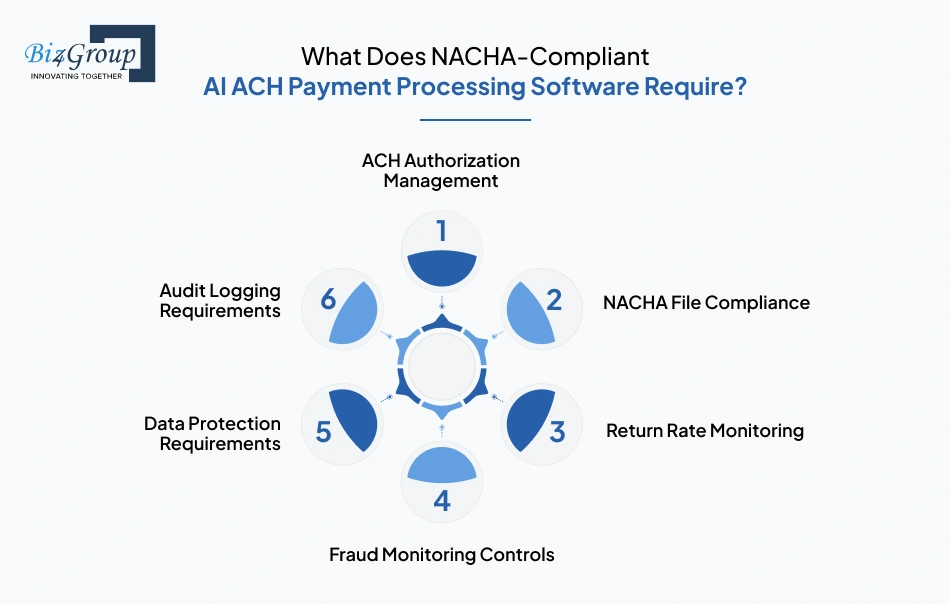

From a compliance perspective, the answer starts with six core requirements: authorization management, NACHA file compliance, return rate monitoring, fraud monitoring controls, data protection, and audit logging. Regardless of the architecture, technology stack, or AI capabilities used, these controls form the foundation of a NACHA-compliant ACH payment processing system.

Every ACH transaction must be supported by the appropriate customer authorization. The platform should be able to collect, store, retrieve, and manage authorization records while maintaining a clear audit trail for future verification and compliance reviews.

ACH files must follow NACHA formatting requirements before they are submitted to banks or payment networks. The system should validate file structure, transaction data, batch information, and required fields to reduce processing errors and file rejections.

NACHA places limits on certain return rate categories. ACH payment software should continuously track return activity, monitor return thresholds, identify emerging issues, and alert teams when return rates begin approaching compliance limits.

NACHA-compliant ACH payment software should include controls that monitor transaction activity, identify suspicious behavior, flag unusual payment patterns, and support fraud investigations. AI can strengthen these controls through risk scoring and anomaly detection, but it does not replace the need for formal fraud monitoring processes.

ACH systems process sensitive financial information and must protect that data throughout its lifecycle. Common requirements include encryption, access controls, secure data storage, credential management, and transaction-level security controls. These protections are essential regardless of whether the platform includes generative AI or other advanced AI capabilities.

Every important action within the system should be recorded through audit logs. This includes payment creation, approval actions, authorization updates, file submissions, return handling, user activity, and compliance-related events. Detailed audit logs help support investigations, compliance reviews, and operational accountability.

Together, these requirements ensure that an ACH payment platform can process transactions securely, maintain regulatory compliance, protect sensitive data, monitor risk, and provide the records needed for audits and investigations. For organizations building AI ACH payment processing software, compliance should be treated as a core system requirement rather than a feature added later. AI can improve payment operations, but it must operate within a compliant ACH processing environment from day one.

Organizations using ACH payment automation software can significantly reduce manual reconciliation effort and accelerate payment operations.

Explore Automation Opportunities

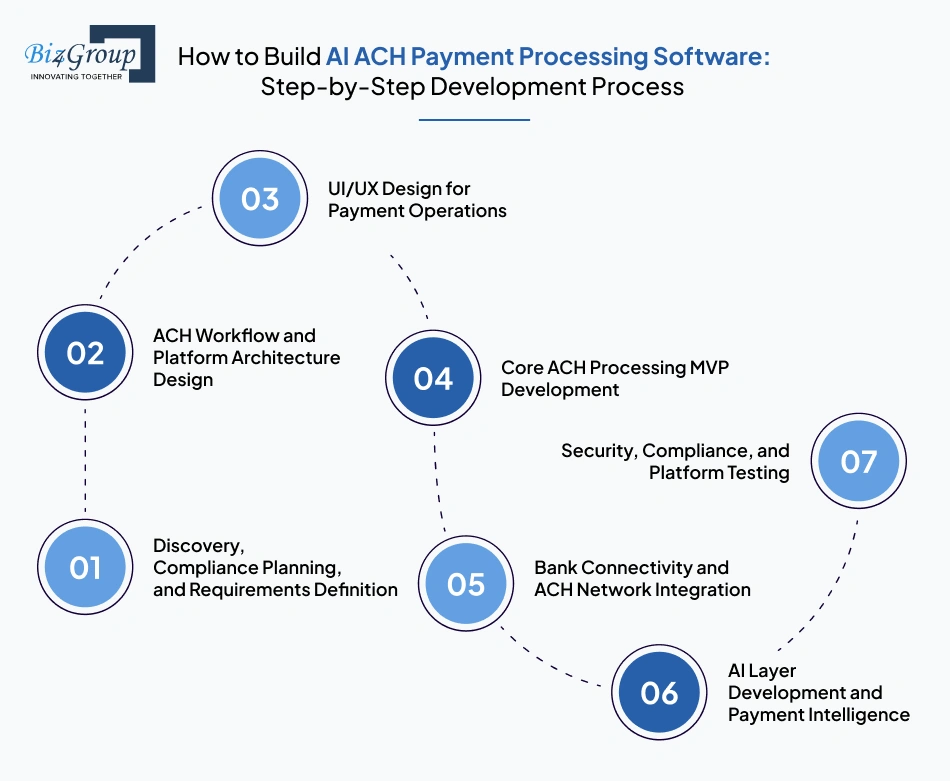

The most common mistake in AI ACH payment processing software development is treating AI as the foundation of the platform. In reality, ACH processing, compliance, bank connectivity, return management, and reconciliation must be built first. AI should then be added as a decision layer that improves payment outcomes, reduces operational workload, and strengthens risk management.

The first step is defining how the ACH payment platform will operate, who will use it, and which business problems AI is expected to solve. Decisions made at this stage influence compliance requirements, architecture choices, integration needs, and future AI capabilities.

Before development begins, teams should design the complete ACH processing workflow. This includes how transactions move through the system, how files are generated and submitted, how returns are handled, and where AI decision-making will be introduced.

Unlike consumer payment apps, ACH payment platforms are primarily used by finance teams, treasury teams, compliance officers, and payment operations staff. The user experience should make it easy to create payments, investigate returns, review fraud alerts, and manage reconciliation activities. Working with an experienced UI/UX design company can help simplify complex payment workflows and improve operational efficiency.

Also read: Top 15 UI/UX Design Companies in USA (2026 Edition)

The first release should focus on building a reliable ACH processing foundation. Instead of launching with advanced AI features, teams should validate payment processing, compliance workflows, and operational controls through focused MVP services.

Also read: 12+ MVP Development Companies in USA to Launch Your Startup in 2026

This phase focuses on connecting the platform to the banking infrastructure responsible for moving ACH transactions. The integration strategy may involve payment processors, sponsor banks, ODFI relationships, banking APIs, or direct ACH connectivity providers.

Once ACH processing, settlement tracking, return handling, and reconciliation workflows are operating reliably, AI can be introduced as a decision layer. The goal is not to replace ACH payment rails but to improve transaction outcomes and automate operational work.

ACH payment systems handle sensitive financial information and must operate within strict compliance requirements. Testing should validate not only functionality but also security, compliance, reliability, and operational readiness.

Also Read: 15+ Software Testing Companies in USA in 2026

After launch, the platform must be continuously monitored and improved. Payment behavior, fraud patterns, return rates, and compliance requirements change over time, making ongoing optimization essential.

Successful AI ACH payment processing software development follows a simple principle: build the ACH system first and the AI layer second. A platform that cannot reliably process transactions, manage returns, maintain compliance, and reconcile payments will not benefit from AI. Once those foundations are in place, AI can improve payment success rates, strengthen fraud controls, reduce manual work, and help the platform scale more efficiently as transaction volumes grow.

Combine AI-powered ACH payment processing with fraud detection, payment failure prediction, and automated exception management.

See What's PossibleThe ideal tech stack for AI ACH payment processing software should support secure transaction processing, NACHA-compliant workflows, bank integrations, real-time fraud monitoring, reconciliation automation, and AI-driven decision-making. Rather than choosing technologies based on popularity alone, teams should select tools that can reliably handle ACH processing, sensitive financial data, and growing transaction volumes.

|

Label |

Preferred Technologies |

Why It Matters |

|---|---|---|

|

Frontend Development |

React.js, Next.js, TypeScript |

Payment operations teams need fast, responsive dashboards for transaction monitoring, returns management, and reconciliation. Modern interfaces are commonly built using ReactJS development services. |

|

Customer & Admin Portals |

Next.js, TypeScript |

Supports secure portals for finance teams, compliance officers, and payment administrators. Many ACH platforms use NextJS development solutions for performance and scalability. |

|

Core ACH Processing Services |

Java, Go, Node.js |

Handles payment initiation, ACH file generation, settlement tracking, return processing, and transaction orchestration. Teams often rely on NodeJS development expertise for API-driven payment services. |

|

AI and Machine Learning Layer |

Python, XGBoost, LightGBM, TensorFlow |

Supports fraud detection, payment failure prediction, anomaly detection, and reconciliation automation. Most AI ACH payment platforms build these capabilities using Python development services. |

|

REST APIs, gRPC |

Enables communication between payment services, banking systems, AI services, and external platforms. |

|

|

Transaction Database |

PostgreSQL, MySQL |

Stores ACH transactions, authorization records, settlement data, return codes, and audit information. |

|

Caching Layer |

Redis |

Improves performance for frequently accessed payment and fraud monitoring data. |

|

Event Streaming and Messaging |

Kafka, RabbitMQ |

Supports event-driven ACH processing, settlement updates, return notifications, and fraud alerts. |

|

Data Warehouse and Analytics |

Snowflake, BigQuery, Redshift |

Centralizes payment, settlement, return, and reconciliation data for reporting and AI model training. |

|

Fraud Detection Infrastructure |

Python, Feature Store, Model Serving Layer |

Supports real-time fraud scoring and transaction risk assessment before payment submission. |

|

Cloud Infrastructure |

AWS, Azure, Google Cloud |

Provides scalable infrastructure for ACH processing, AI workloads, compliance controls, and high availability. |

|

Containerization and Orchestration |

Docker, Kubernetes |

Simplifies deployment, scaling, and management of payment processing and AI services. |

|

Monitoring and Observability |

Prometheus, Grafana, ELK Stack |

Tracks payment processing health, ACH return activity, fraud alerts, and system performance. |

|

Security and Compliance Controls |

Vault, IAM, KMS, SIEM Tools |

Supports encryption, access control, audit logging, and NACHA compliance requirements. |

For anyone asking “what programming languages, frameworks, databases, and cloud infrastructure should we be using if we are building an enterprise grade ACH payment platform in 2026 that needs to handle high transaction volumes, real time fraud detection using AI, and direct integration with FedACH and The Clearing House, we are a team of 6 developers and need to pick the right stack before we start”. The answer is: While technology choices vary, most AI ACH payment processing platforms rely on scalable backend services, event-driven architectures, relational databases, cloud infrastructure, and Python-based AI models to support secure ACH processing, fraud detection, reconciliation, and compliance.

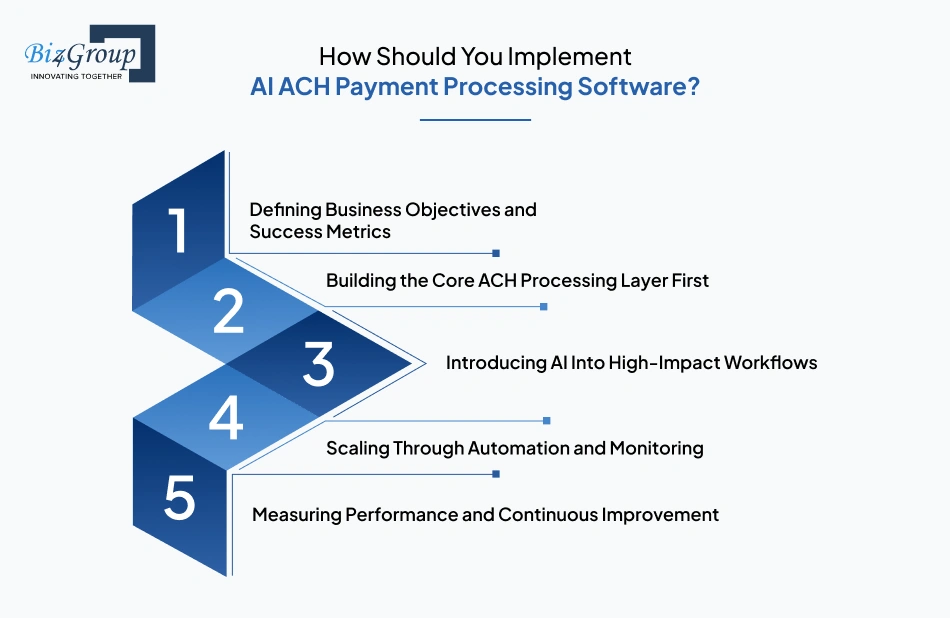

The best way to implement AI ACH payment processing software is to start with a working ACH platform and then add AI where it can solve specific payment problems. Trying to add AI everywhere from the beginning usually increases complexity without delivering clear results.

Before implementing AI, decide what problem you are trying to solve. For most organizations, the focus is reducing ACH returns, improving fraud detection, automating reconciliation, or increasing payment success rates. Defining clear goals early makes it easier to measure whether the implementation is successful.

AI should not be the first thing you build. The platform must already be able to process ACH payments, manage returns, track settlements, maintain compliance, and handle reconciliation. Once those processes are working reliably, AI has the data and workflows it needs to produce useful results.

Many development teams ask: "we are a software development company and a client wants us to build them a custom ACH payment processing platform with AI fraud detection built in, what are all the features we need to include, how do we handle same day ACH, returns, and reconciliation, and what does a realistic development timeline and cost look like for something like this in 2026"

The practical approach is to start with AI use cases that can create value quickly. Fraud risk scoring, payment failure prediction, adaptive retry recommendations, and reconciliation automation are often the best starting points because they improve payment operations without requiring major changes to the ACH processing system.

Once the first AI features are working well, additional automation can be introduced across other payment workflows. Teams should track how AI affects payment outcomes, fraud detection accuracy, return rates, and operational efficiency. This phased approach is common in business app development using AI projects where automation expands over time based on proven results.

AI systems need ongoing tuning and improvement. Payment behavior changes, fraud tactics evolve, and transaction patterns shift over time. Organizations often hire AI developers to refine models, improve decision accuracy, and keep AI performance aligned with business goals.

|

Implementation Phase |

Primary Goal |

Key Outcome |

|---|---|---|

|

Define Objectives |

Identify the payment problems AI should solve |

Clear success metrics and implementation priorities |

|

Build Core ACH Foundation |

Establish reliable ACH processing, compliance, returns, and reconciliation workflows |

Stable payment infrastructure and clean operational data |

|

Deploy AI in High-Impact Areas |

Introduce AI into fraud detection, payment failure prediction, retries, and reconciliation |

Faster ROI and measurable operational improvements |

|

Scale Automation |

Expand AI-driven automation across additional payment workflows |

Increased efficiency and reduced manual effort |

|

Continuously Improve |

Monitor performance and refine AI models over time |

Better accuracy, stronger fraud controls, and improved payment outcomes |

The most successful AI ACH payment processing implementations start with a clear business problem, apply AI to a few high-impact workflows, and expand from there. This approach keeps implementation risk low while making it easier to demonstrate measurable results.

Get clarity on architecture, compliance requirements, implementation strategy, and development costs before you start building.

Talk to Our AI & Fintech ExpertsThe cost of AI ACH payment processing software development typically ranges from $40,000 to $300,000+. These are ballpark estimates, and the final cost depends on factors such as banking integrations, compliance requirements, AI capabilities, transaction volumes, and overall platform complexity.

|

Platform Stage |

Estimated Cost |

Typical Scope |

|---|---|---|

|

MVP-level AI ACH Payment Processing Software |

$40,000 - $80,000 |

Core ACH payment processing, NACHA file generation, bank integrations, payment tracking, basic reporting, and foundational compliance controls. |

|

Production-Ready AI ACH Payment Processing Software |

$80,000 - $180,000 |

Adds return management, reconciliation workflows, Same Day ACH support, advanced reporting, stronger security controls, and initial AI-powered automation capabilities. |

|

Enterprise-Grade AI ACH Payment Processing Software |

$180,000 - $300,000+ |

Includes high-volume transaction processing, advanced fraud detection, payment failure prediction, automated reconciliation, multi-bank integrations, and enterprise-grade infrastructure. |

The biggest cost differences usually come from the complexity of the platform rather than ACH processing itself. Features like AI fraud detection, direct bank integrations, reconciliation automation, compliance controls, and support for large transaction volumes can increase both development costs and timelines.

A common question from technology leaders is: "i am a solutions architect and i need to explain to a non technical CFO why building a custom AI powered ACH payment system is better than just using Stripe or a third party processor, can you help me break down what the actual technical advantages are, what AI can do that rule based systems cant, and what the long term cost comparison looks like for a company processing 50000 plus ACH transactions a month"

For businesses processing large ACH volumes, a custom AI ACH payment platform gives more control over how payments, fraud checks, reconciliation, reporting, and automation are handled. AI can spot patterns that rule-based systems often miss, helping reduce failed payments, improve fraud detection, and cut down on manual work. Third-party processors usually cost less to get started, but transaction fees can add up quickly as payment volume grows. A custom platform costs more upfront but can become more cost-effective over time while offering greater flexibility. This is one reason many organizations work with a software development company in Florida when evaluating long-term payment infrastructure investments.

The decision usually comes down to how much control you need, how many ACH payments you process, and whether standard payment tools can support your business requirements. For some organizations, a third-party provider offers the fastest path to market. For others, a custom AI ACH payment processing platform provides the flexibility needed to support unique payment workflows, AI-driven automation, and long-term growth.

Custom AI ACH payment processing software development is often the better choice when ACH payments are a core part of the business rather than a supporting function.

Common scenarios include:

In these situations, the higher upfront cost is often worth it because the platform can be tailored to your payment operations instead of forcing your team to work around vendor limitations.

Not every organization needs to build and maintain its own ACH infrastructure.

Third-party providers are often a better fit when:

For many startups and early-stage fintech products, outsourcing ACH processing allows teams to focus on growing the business before investing in custom payment infrastructure.

|

Factor |

Custom AI ACH Payment Platform |

Third-Party Provider |

|---|---|---|

|

Upfront Cost |

Higher |

Lower |

|

Long-Term Cost |

Can decrease at scale |

Typically increases with transaction volume |

|

Workflow Customization |

Extensive |

Limited |

|

AI Capabilities |

Fully customizable |

Restricted to vendor offerings |

|

Bank Integration Flexibility |

High |

Dependent on provider support |

|

Compliance Responsibility |

Greater internal ownership |

Shared with provider |

|

Scalability Control |

Full control |

Provider-dependent |

Third-party providers are easier to launch, while custom platforms offer more control and

flexibility as payment operations become more complex.

Before deciding whether to build or buy, evaluate your payment volume, customization needs, compliance requirements, and long-term growth plans. The right choice depends less on company size and more on how important ACH payment processing is to your business operations and competitive strategy.

A simple rule is that the more unique your payment workflows become, the stronger the case for custom development.

Building AI ACH payment processing software requires experience with ACH processing, banking integrations, compliance, cloud infrastructure, and AI development.

Biz4Group LLC helps organizations build custom ACH payment platforms that combine payment processing, fraud detection, reconciliation automation, compliance controls, and AI-driven decision-making in a single system.

Key strengths include:

The overall experience of Biz4Group as one of the top AI development companies in Florida, helps ensure AI is implemented as a practical tool that improves payment operations and business outcomes.

Create custom AI ACH payment processing software tailored to your workflows, transaction volumes, and automation goals.

Book a Strategy CallAI ACH payment processing software is most useful when it solves real problems within ACH operations. The biggest opportunities are usually fraud detection, payment failure prediction, retry optimization, reconciliation, and exception management. These are the areas where AI can help payment teams save time, reduce risk, and improve payment performance.

The choice between a custom platform and a third-party provider depends on how your business uses ACH payments. Companies with simple payment needs can often move faster with an existing provider. Companies processing larger payment volumes or managing more complex workflows often need greater control over automation, reporting, integrations, and AI capabilities.

As ACH operations grow, the focus shifts from simply processing payments to improving how those payments are managed. Working with a custom software development company that understands ACH infrastructure can help build AI software that fits your payment processes, compliance needs, and long-term business goals.

Planning an AI ACH Payment Processing Platform in 2026?

Schedule a consultation to discuss architecture, banking integrations, AI use cases, compliance requirements, development timelines, and estimated costs for your specific business model.

Yes. Most AI ACH payment processing platforms are designed to integrate with existing banking infrastructure, payment processors, ERP systems, accounting platforms, and treasury management tools. This allows organizations to add AI-driven capabilities such as fraud detection, payment risk analysis, and reconciliation automation without completely replacing their existing payment environment.

Development timelines vary based on platform complexity, integration requirements, and AI functionality. A basic MVP can often be built within 3-5 months, while a production-ready platform may take 6-12 months. Enterprise-grade implementations with multiple bank integrations, advanced AI models, and high-volume transaction processing can require 12 months or longer.

AI models typically rely on historical transaction data, settlement outcomes, ACH return codes, account activity patterns, reconciliation records, and fraud-related events. The quality, accuracy, and volume of available data directly impact the effectiveness of fraud detection, payment failure prediction, and automation capabilities.

The cost of AI ACH payment processing software development generally ranges from $40,000 to $300,000+. Smaller MVPs typically fall at the lower end of the range, while enterprise platforms with advanced AI capabilities, multiple banking integrations, reconciliation automation, and large-scale transaction processing requirements can exceed the upper end of the range.

AI ACH payment processing software is commonly used by fintech companies, banks, credit unions, payment service providers, wealth management firms, insurance companies, healthcare organizations, payroll providers, and enterprises that process large volumes of ACH transactions. Organizations with significant payment operations often see the greatest benefits from automation and AI-driven decision-making.

Common challenges include poor-quality transaction data, insufficient compliance planning, overreliance on AI without proper oversight, and introducing AI into workflows before core ACH processes are stable. Organizations typically achieve better results when AI is implemented gradually and monitored using clearly defined performance metrics.

with Biz4Group today!

Our website require some cookies to function properly. Read our privacy policy to know more.