info@biz4group.com

info@biz4group.com

Imagine a digital system that doesn’t wait for instructions but instead, understands your business goals, learns from real-time feedback, and takes independent actions to get the job done.

Read More

AI Summary Powered by Biz4AI

AI Summary Powered by Biz4AI

You've probably already spent weeks thinking about your teletherapy platform.

The features, the user flow, the branding, or maybe you've even started talking to developers.

But here's the question most founders never ask early enough: what type of teletherapy platform are you actually building?

Not in terms of features. In terms of architecture.

Because right now, without realizing it, you're standing at the most consequential fork in the road of your entire build. One path leads you toward a teletherapy marketplace platform architecture, where independent licensed providers operate on your infrastructure, and you facilitate the connection between them and patients. The other path leads you toward a single provider teletherapy platform architecture, where your company is the care delivery entity, providers work for you, and every clinical decision flows through one accountable structure.

These are not two versions of the same product. They are two completely different systems. Different databases. Different compliance obligations. Different billing infrastructures. Different revenue models. Different investor stories.

And here's what makes this the most expensive mistake in digital health: you cannot switch after you've built.

We've seen it happen. A founder builds a marketplace because it "feels more scalable." Twelve months later, an employer wants to sign a B2B contract, a payer wants to credential the platform, and the investors want clinical outcome data. None of that is possible with the architecture that's already in place. The rebuild costs more than the original build. The timeline resets. The runway disappears.

That's not a technology problem. That's an architecture decision problem. And it happens because the teletherapy platform business model architecture decision got made by default, not by design.

The mental health technology space isn't giving anyone a pass on this. The global teletherapy solutions market is projected to reach $3.02 billion by 2034, growing at 13.1% annually. And mental health remains the most utilized telehealth service in the United States as of 2025. The market is growing fast, competition is intensifying, and the platforms that win will be the ones that made the right foundational architecture call early, not the ones that built the fastest.

So which architecture is right for your business?

That depends on your go-to-market, your clinical model, your compliance posture, your funding stage, and what your investors are actually looking for. And that's exactly what we're going to break down in this guide, section by section.

The teletherapy marketplace vs single provider platform architecture question doesn't have a universal answer. But it does have the right answer for your specific situation. And by the time you finish reading this, you'll know what that is.

At Biz4Group, we've built both. We've seen what happens when founders get this right and what it costs when they don't. We're not going to give you a generic comparison. We're going to give you the technical, compliance, business model, and investor-level breakdown you need to make this call correctly, the first time.

If you're still working through the foundational business side of how to start a mental health business, that's a smart place to anchor your thinking before the architecture conversation begins. Because the business model and the architecture aren't separate decisions. One determines the other.

Before you make any technical decision, before you talk to a single developer, before you write one requirement document, you need to answer one question honestly.

Are you building a platform that connects people to therapists? Or are you building a company that delivers therapy?

Those sound similar. They are not. And the difference between them is the entire architecture of your product.

A teletherapy marketplace is a platform where independent, licensed mental health providers operate as separate businesses on your infrastructure. You don't employ them. You don't own their clinical relationships. You build the environment, they bring their practice, and patients come to find them.

Think of it this way. You're not the therapist. You're the building the therapists work out of, and you charge rent or take a commission for every appointment that happens inside it.

BetterHelp is the most recognized example of this model at scale. Zocdoc applies similar logic to broader healthcare. The platform facilitates. The provider delivers. The patient pays.

So why are so many founders drawn to this model?

These are real advantages. They explain why this model has become the default mental health startup model over the last several years.

But here's what most founders find out the hard way. When you actually build teletherapy marketplace platform architecture from the ground up, the operational lightness on the provider side gets replaced by serious technical complexity underneath. Your data model, your compliance structure, your billing infrastructure, and your matching engine all become significantly harder problems than they would be in a single-provider build.

We've worked with founders who came to us specifically because they'd seen the marketplace model work at scale and wanted to replicate it. The ones who struggled weren't the ones with smaller budgets. They were the ones who treated the teletherapy platform business model architecture decision as a default rather than a deliberate choice. They picked marketplace because it sounded scalable, without fully understanding what architecture commits them too technically.

The important thing to understand right now is what a marketplace actually is at its foundation. It is a multi-sided platform where every provider is a separate entity on shared infrastructure. That single fact reshapes every technical decision you make, from how you store patient records to how you handle a malpractice claim.

Understanding the teletherapy app architecture marketplace vs single provider distinction starts here, at the structural level, before features ever enter the conversation.

A single provider teletherapy platform works differently at every level.

Here, the platform is not the middleman. It is a care delivery entity. Therapists and psychiatrists are employees or W-2 contractors. The company holds clinical relationships, owns patient records, manages the credentialing, submits the insurance claims, and is accountable for the quality of care being delivered.

Brightside Health is a strong example of this model. Cerebral, in its more structured iteration, follows similar logic. These platforms don't present you with a directory of independent therapists. They present you with their clinical team.

And if that sounds like a harder business to run, in some ways it is. But the founders who choose single provider teletherapy platform architecture deliberately aren't doing it because it's easier. They're doing it because it's the only architecture that supports the business they're actually trying to build.

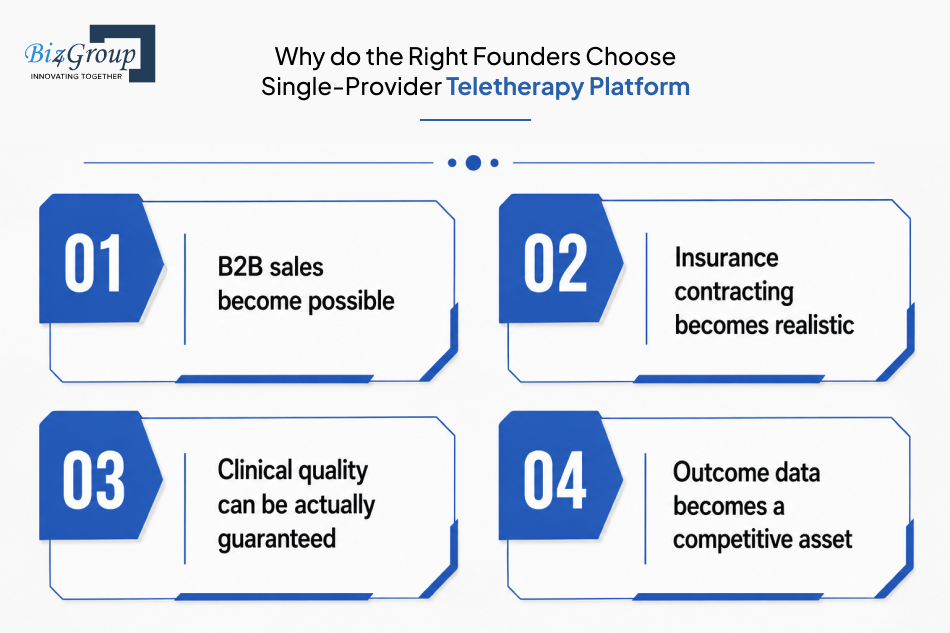

Why does the right founder choose this model?

In our experience working with behavioral health founders, the single provider teletherapy platform model is consistently underestimated because people assume it cannot scale. We've watched that assumption cost founders real money when they chose marketplace architecture for the wrong reasons and then couldn't access the B2B contracts or insurance relationships that would have made their business viable.

The single provider teletherapy platform architecture scales differently, not worse. And the founders who choose it deliberately are usually the ones who have thought most carefully about who their actual customer is.

That clarity matters more than most people realize. When founders ask us about the teletherapy marketplace vs single provider platform architecture question, the answer almost always comes back to one thing: who are you selling to, and what are you promising them clinically? The architecture has to match both answers simultaneously.

What are the key architectural differences between teletherapy marketplace platforms and single provider mental health platforms? That's the question the next section answers in full technical detail, layer by layer.

Understanding the top mental health app features that patients expect from both types of platforms is a useful grounding exercise before the architecture conversation gets fully technical. Because regardless of which model you build, the patient experience has to hold up, and the system underneath has to support it without compromise.

The wrong call here costs 18 months and $300K. Let's make sure you get it right the first time.

Talk to an ExpertFounders often ask us for a comprehensive comparison of teletherapy marketplace architecture versus single provider platform architecture that goes beyond a feature list. So here it is.

The teletherapy app architecture marketplace vs single provider split runs deeper than most people expect. What are the key architectural differences between teletherapy marketplace platforms and single provider mental health platforms, and how do they affect compliance, billing, and scalability? Every dimension is in the table below, and every dimension carries real build consequences.

In our experience building teletherapy marketplace platform architecture, the three areas founders most consistently underestimate are credentialing infrastructure, multi-tenant data isolation, and split payment billing logic. Those same three areas are where compliance failures concentrate and where technical debt compounds fastest.

When you're thinking through healthcare software product development for a teletherapy product, this table is where that conversation starts.

|

Technical Architecture Dimension |

Teletherapy Marketplace Platform |

Single-Provider Teletherapy Platform |

|---|---|---|

|

Data Model |

Multi-tenant architecture where each provider's patient records, session notes, scheduling data, and clinical history must be isolated at the database schema level, not just by access controls, because PHI from one provider must be structurally inaccessible to another, requiring tenant-per-provider schema design or row-level security with strict enforcement |

Unified clinical schema where all patient records, session notes, outcomes data, and clinical history live in one centralized database, making cross-provider analytics, care continuity, and population-level outcome reporting genuinely possible without any data migration or schema complexity |

|

Provider Identity |

Every provider is a separate entity on your infrastructure, requiring the platform to maintain independent provider profiles, separate credential records, individual contract states, and distinct data environments for each, which multiplies the complexity of every system that touches provider data |

Providers are part of one organizational entity, their profiles, credentials, schedules, and clinical records all live within a single unified identity model, which simplifies every system that touches provider data from onboarding through offboarding |

|

Provider Credentialing |

Must be automated, API-driven, and continuous, requiring NPI verification via NPPES, state license status checks against individual state board APIs, OIG exclusion list monitoring, CAQH integration, and automated license expiration alerts across potentially hundreds of providers in multiple states, adding 3 to 6 months to your build timeline |

An internal operational function handled through HR rather than software architecture, the platform verifies licenses before hiring and tracks renewals as an employment compliance task, significantly simpler to implement but requiring a dedicated clinical operations team as provider headcount grows |

|

Requires three distinct API layers, a provider-facing API for independent practitioners managing their own schedules, patients, and billing, a patient-facing API for discovery and booking, and an admin API for platform operations, each with different authentication models, rate limits, and data access permissions |

A single unified API layer serving all internal users, providers, patients, and administrators operate within one access model, which reduces API surface area, simplifies versioning, and makes integrations with third-party systems significantly more straightforward |

|

|

Authentication and Access Control |

Multi-tenant identity management where each provider operates as an independent tenant with their own user base, requiring tenant-scoped authentication tokens, strict data boundary enforcement between tenants, and role-based access controls that prevent any cross-tenant data leakage, one of the most technically demanding aspects of marketplace architecture |

Unified access control model where all users, providers, patients, and admins exist within one identity system, role-based permissions are simpler to implement and audit, and there is no tenant boundary enforcement problem because all data belongs to one organizational entity |

|

Matching Engine |

The teletherapy platform provider matching algorithm is a full recommendation system evaluating patient clinical need, provider specialty and therapeutic modality, state-level licensing compatibility, insurance network compatibility, and real-time schedule availability simultaneously, starting as rule-based filtering and evolving toward ML-based matching as outcome data accumulates, with a cold-start problem every marketplace has to solve before matching quality meaningfully improves |

A scheduling and assignment function rather than a recommendation engine, patients are matched to available providers based on specialty fit and availability, the complexity is operational rather than algorithmic, and the platform has full visibility into provider capacity and clinical fit without the data isolation constraints that complicate marketplace matching |

|

EHR Integration |

Complex because each independent provider may use their own EHR system, requiring the platform to either mandate a specific EHR for all providers, build integrations with multiple systems, or operate with incomplete EHR connectivity, any of which creates data fragmentation and interoperability gaps that affect clinical continuity |

Straightforward because all providers use the platform's own EHR or one integrated system, EHR integration for mental health platforms is a one-time architectural decision that applies uniformly across every provider and every patient interaction without fragmentation |

|

No-Show Rate Management |

Teletherapy no-show rate management platform logic must account for independent provider preferences and contractual terms, reminder systems need provider-level configuration, cancellation policy enforcement is inconsistent across a provider network with varying individual policies, and the platform has limited technical ability to intervene in the patient-provider relationship when no-show patterns develop |

A unified platform function where reminder infrastructure across SMS, email, and push notifications deploys consistently without individual provider configuration, cancellation policies are enforced uniformly, automated rebooking workflows keep patients in the clinical relationship, and intervention logic can be applied systematically across the entire patient population |

|

Scalability Architecture |

Teletherapy marketplace scalability architecture scales two variables simultaneously, patient volume and provider count, requiring a stateless horizontally scalable API layer, multi-tenant database sharding strategy for PHI isolation under load, async job queues for credentialing checks and provider-related operations, and an event-driven scheduling system handling real-time availability updates across a constantly changing provider pool |

Scales one variable, patient volume, with infrastructure that grows more predictably, provider count is managed through hiring rather than open onboarding, the database schema stays unified under load, and the primary scaling challenge is session infrastructure capacity rather than multi-tenant architectural complexity |

|

Data Portability |

When an independent provider leaves the marketplace, patient record ownership becomes architecturally and legally complex, the platform must determine what data the provider can take, what stays on the platform, and how patient continuity is maintained, a problem that must be designed into the data model from day one rather than solved operationally later |

The platform owns all patient records as the care delivery entity, provider departures are an HR event not a data architecture event, patient continuity is maintained within the platform's own provider network, and there is no ambiguity about data ownership because it never belonged to an individual provider |

|

Outcome Data Ownership |

Fragmented across independent providers who maintain their own clinical records, the platform cannot aggregate outcome data at the population level, cannot publish remission rates or treatment effectiveness metrics, and cannot use clinical evidence in payer negotiations or investor conversations without navigating individual provider data sharing agreements |

Unified at the platform level, all outcome data lives in one schema, the platform can measure which therapeutic approaches work for which diagnoses, track standardized outcome metrics across patient cohorts, and use clinical evidence directly as a competitive and commercial asset |

The teletherapy marketplace vs single provider platform architecture decision shows up in every row of that table, not as a business model preference but as a concrete technical commitment with real cost, timeline, and compliance consequences. Teletherapy marketplace scalability architecture requires two variables scaling simultaneously, patient volume and provider count, each with its own infrastructure demands. Single provider teletherapy platform architecture scales one variable, stays centralized on compliance, and produces a more predictable path to profitability. That's the tradeoff, and it starts at the architecture level, not the feature level.

When something goes wrong on your platform, who is legally responsible?

In a teletherapy marketplace, that question gets complicated fast. In a single provider teletherapy platform, the answer is always the same: you are, and you've built the systems to handle it.

We've worked with founders who came to us mid-build, already six months into a marketplace architecture, asking how to add payer contracting to their revenue model. The answer was hard to give: the compliance structure they'd built made it architecturally impossible without a significant rebuild. The teletherapy platform business model architecture decision they made early had closed off a revenue channel they hadn't anticipated needing.

That's the real cost of getting compliance architecture wrong. Not just regulatory risk, but commercial limitation.

What are the key architectural differences between teletherapy marketplace platforms and single provider mental health platforms and how do these differences affect compliance, billing, and scalability? The table below answers the compliance piece completely, and every row has direct consequences for what your business can do commercially.

|

Compliance Dimension |

Teletherapy Marketplace Platform |

Single-Provider Teletherapy Platform |

|---|---|---|

|

HIPAA Liability Structure |

Distributed across every independent provider on the platform, each provider is a separate covered entity or business associate operating under their own HIPAA obligations, and your platform's exposure depends on how tightly your BAAs are drafted and what technical controls you enforce across the entire provider network |

Centralized in the platform as a single covered entity, the platform holds full HIPAA accountability for every patient interaction, every data access event, and every clinical record, which makes liability clear, manageable, and defensible in any regulatory review |

|

Business Associate Agreements |

A separate BAA required with every independent provider on the platform, at 100 providers that is 100 individual legal agreements to draft, execute, maintain, and update whenever HIPAA requirements change, and every BAA represents a separate compliance obligation that must be monitored and enforced individually |

One unified BAA framework covering the entire platform and all employed providers, when HIPAA requirements change the platform updates one policy and one set of technical controls, not hundreds of individual provider agreements |

|

State Licensing Enforcement |

Must be enforced at the platform level in real time, every session booking must verify that the provider holds an active license in the state where the patient is located at the time of service, not where the provider is based, requiring automated license status checks against individual state board APIs before every appointment is confirmed |

Managed as an internal employment compliance function, the platform only operates in states where it holds group practice authorization, provider licenses are verified before hiring and monitored as an HR function, and the platform never books a session in a state it isn't authorized to operate in |

|

Multi-State Practice Compliance |

Every new state your providers cover adds a new licensing board, new renewal timelines, new telehealth practice standards, and potentially new prescribing rules if psychiatry is involved, and all of this must be tracked and enforced automatically at the platform level across a provider pool that is constantly changing |

The platform expands state by state as a deliberate business decision, obtaining group practice authorization in each new state before operating there, which keeps multi-state compliance controlled, sequential, and manageable rather than reactive and distributed |

|

Provider Credentialing Compliance |

An ongoing automated process that never stops, licenses expire, sanctions get added to OIG exclusion lists, malpractice coverage lapses, and your platform must catch all of it in real time across every provider on your network, because a single session delivered by a provider with a lapsed license or an active OIG exclusion is a compliance violation that lands on your platform |

A periodic internal audit function, the platform reviews provider credentials on a defined schedule as part of employment compliance, any credential issue results in immediate operational action, and the platform never has more providers than its clinical operations team can actively monitor |

|

Clinical Quality Audits |

Practically impossible at scale, each independent provider operates under their own clinical philosophy, documentation style, and treatment approach, and the platform has no contractual or operational mechanism to audit session quality, review clinical notes, or enforce evidence-based practice standards across hundreds of independent practitioners |

Fully operational and routine, the platform has direct access to all session notes, outcome data, and clinical records, supervisors can review documentation across the entire provider network, and clinical quality audits are a standard operational function rather than a contractual negotiation |

|

Insurance Billing Entity |

Structurally ambiguous, if independent providers bill under their own NPI and tax ID the platform is a scheduling tool not a healthcare provider, if the platform bills as a group practice it assumes full provider liability and must credential every provider through every payer individually, neither path is clean and the wrong choice made at architecture time is expensive to unwind |

Unambiguous from day one, the platform bills as a single group practice entity under one NPI and one tax ID, every provider is credentialed through the platform rather than individually, and the billing structure is immediately recognizable and acceptable to payers |

|

Payer Credentialing |

Structurally difficult because payers credential providers not platforms, in a marketplace of independent contractors the platform cannot negotiate a single payer contract that covers its entire provider network, each provider must be credentialed individually with each payer, creating an operational burden that scales with every provider and every payer relationship |

Straightforward because the platform credentials as a single group practice with each payer, once the platform is in-network all employed providers are covered under that contract, and payer relationships can be negotiated, managed, and expanded at the organizational level rather than provider by provider |

|

Breach Response Accountability |

Complex because a breach involving one provider's patient data may implicate that provider's BAA, the platform's technical controls, and potentially other providers' data environments depending on how the breach occurred, and untangling accountability across distributed tenants adds significant time and legal complexity to breach response |

Clear and immediate, the platform is the single accountable entity for any breach, the incident response plan covers the entire platform, notification obligations are managed centrally, and there is no ambiguity about who is responsible for remediation and patient notification |

|

Regulatory Audit Readiness |

Requires reconstructing a compliance picture across hundreds of individual provider BAAs, separate credentialing records, and distributed clinical documentation, which makes regulatory audits significantly more time-consuming and expensive to respond to |

The platform maintains one centralized compliance record covering all providers, all patient interactions, and all clinical documentation, making regulatory audits faster, cheaper, and significantly less disruptive to ongoing operations |

|

Patient Record Ownership |

Legally and architecturally complex, when an independent provider leaves the marketplace, the platform must navigate what patient data the provider can take, what stays on the platform, and how to maintain patient continuity, a problem that must be designed into the data model and provider contracts from day one |

Unambiguous, the platform owns all patient records as the care delivery entity, provider departures are managed as HR events not data ownership disputes, and patient continuity is maintained within the platform's own provider network without any legal complexity |

|

Prescribing Compliance |

If psychiatry services are included, each prescribing provider operates under their own DEA registration and state prescribing authority, the platform must track and verify each provider's prescribing permissions in every state they serve patients, adding another layer of ongoing automated compliance monitoring |

The platform manages prescribing compliance as a unified clinical governance function, all prescribing providers operate under a consistent policy framework, and prescribing authority is verified and monitored as part of the platform's single credentialing and quality oversight process |

The compliance gap between these two models isn't just about risk management. It's about what your architecture makes commercially possible. Payer contracting, B2B employer sales, and clinical outcome guarantees all require the kind of centralized accountability that single provider teletherapy platform architecture delivers by design and that build teletherapy marketplace platform architecture has to work significantly harder to approximate.

The teletherapy marketplace vs single provider platform architecture decision you make at the start determines whether compliance is a foundation you build on or a constraint you work around for the life of your platform.

One wrong compliance call and your payer relationships, B2B contracts, and investor story unravel together.

Get a Free ConsultationThe architecture decision you make doesn't just determine how your platform is built. It determines how your platform makes money, how predictably it makes money, and how attractive that money looks to the investors and acquirers you'll eventually be talking to.

We've sat across the table from founders who built a marketplace because they liked the commission model, only to realize 18 months later that their entire revenue ceiling was capped by how many cash-pay patients they could acquire. And we've worked with single-provider founders who initially dismissed insurance contracting as "too complex," then watched it become their single largest revenue channel within two years of launch.

How does the architecture decision between teletherapy marketplace and single provider platform affect long term business model viability, investor attractiveness, and competitive positioning? Here's the complete picture.

The teletherapy marketplace platform generates revenue in one of two ways, sometimes both simultaneously.

Commission per session: The platform takes 10 to 30% of every session fee paid by a patient to an independent provider. Simple to understand, straightforward to implement, and directly tied to session volume on the platform.

Provider subscription: Independent therapists pay a monthly fee, typically $50 to $200, for access to the platform's patient acquisition infrastructure, scheduling tools, and visibility in search results. Predictable recurring revenue that doesn't depend on individual session completion.

Sounds clean. But here's what the revenue model actually requires underneath:

In our experience, the teletherapy platform business model architecture decision toward a marketplace works best when your go-to-market is direct-to-consumer, your patient acquisition channel is performance marketing at scale, and your primary competition is on provider variety and matching quality rather than clinical outcomes or payer relationships.

The single provider teletherapy platform has access to revenue channels that the marketplace model structurally cannot reach.

Direct-pay session fees are the starting point, patients pay the platform directly for sessions with employed providers, and the revenue is clean, immediate, and fully attributable to the platform.

But here's where the single-provider model separates itself commercially:

How do teletherapy investors evaluate the marketplace versus single provider platform architecture decision when assessing business model viability and long-term scalability potential? The answer almost always comes back to revenue predictability, clinical outcome data ownership, and the platform's ability to access payer and employer channels. On all three dimensions, the single-provider model has a structural advantage that compounds over time.

Building an AI therapeutic app layer on top of a single-provider platform is also significantly more commercially viable, because the unified patient data that single-provider architecture produces is exactly what AI-driven clinical tools need to generate meaningful, defensible insights.

|

Business Model Dimension |

Teletherapy Marketplace Platform |

Single-Provider Teletherapy Platform |

|---|---|---|

|

Primary Revenue Model |

Session commission (10-30%) or provider subscription ($50-$200/month) |

Direct-pay session fees, insurance reimbursement, B2B employer contracts |

|

Gross Margin Profile |

60-80%, asset-light but variable |

40-60%, lower but significantly more predictable |

|

Patient Acquisition |

Two-sided, must acquire patients and providers simultaneously, high early-stage burn |

Single-sided, patient acquisition only, provider growth is controlled through hiring |

|

Insurance Contracting |

Structurally difficult, billing entity ambiguity makes payer contracting complex and slow |

Straightforward, platform credentials as a single group practice, payer contracts cover all employed providers |

|

B2B Employer Sales |

Not viable, employers require a single accountable clinical entity and outcome guarantees a marketplace cannot provide |

Core growth channel, platform can make clinical promises, sign single contracts, and deliver outcome reporting |

|

Revenue Predictability |

Variable, tied to session volume and two-sided marketplace liquidity |

Predictable, diversified across direct-pay, insurance, and B2B with recurring contract structures |

|

Outcome-Based Contracting |

Not possible, fragmented outcome data across independent providers cannot support value-based contracts |

Increasingly viable as unified outcome data accumulates, positions platform for where behavioral health reimbursement is heading |

|

Investor Type |

Consumer tech investors comfortable with marketplace dynamics and longer paths to profitability |

Healthcare-focused investors and strategic acquirers looking for clinical differentiation, payer relationships, and defensible revenue |

|

Long-Term Competitive Moat |

Marketplace liquidity, provider variety, and matching quality |

Clinical outcome data, payer contracts, and B2B relationships that take years for competitors to replicate |

|

M&A Attractiveness |

Harder to integrate into payer contracts post-acquisition, clinical quality variability is a due diligence risk |

Highly attractive to health system acquirers and payer strategic buyers, clean clinical identity and payer relationships transfer directly |

The business model picture here connects directly back to the architecture decision. A teletherapy marketplace is a strong model if your market is direct-to-consumer cash-pay and your competitive advantage is network scale and matching quality. A single provider teletherapy platform is the right model if your revenue strategy includes insurance, employers, or payers, and if clinical outcome differentiation is part of how you plan to win.

What makes this consequential is that you cannot add insurance contracting or B2B employer sales to a marketplace architecture after the fact without a fundamental rebuild of your compliance and billing infrastructure. The teletherapy marketplace vs single provider platform architecture decision and the business model decision are the same decision, made at the same time, at the start of your build.

Every founder we talk to eventually asks the same question: which architecture is actually right for my specific situation?

The honest answer is that the teletherapy marketplace vs single provider platform architecture decision is not about which model is better. It's about which model fits the business you're actually building, the customer you're actually serving, and the revenue channels you're actually planning to pursue.

Here's how to figure that out.

Ask yourself one question first: is your competitive advantage provider variety?

If patients come to your platform because they want access to a wide range of therapists across different specialties, languages, therapeutic approaches, and availability windows, and if your go-to-market is direct-to-consumer with performance marketing as your primary acquisition channel, the teletherapy marketplace platform architecture is likely the right fit.

It also makes sense if:

If all of those conditions are true for your business, build teletherapy marketplace platform architecture from the start and invest properly in the credentialing infrastructure, multi-tenant data isolation, and matching engine it requires.

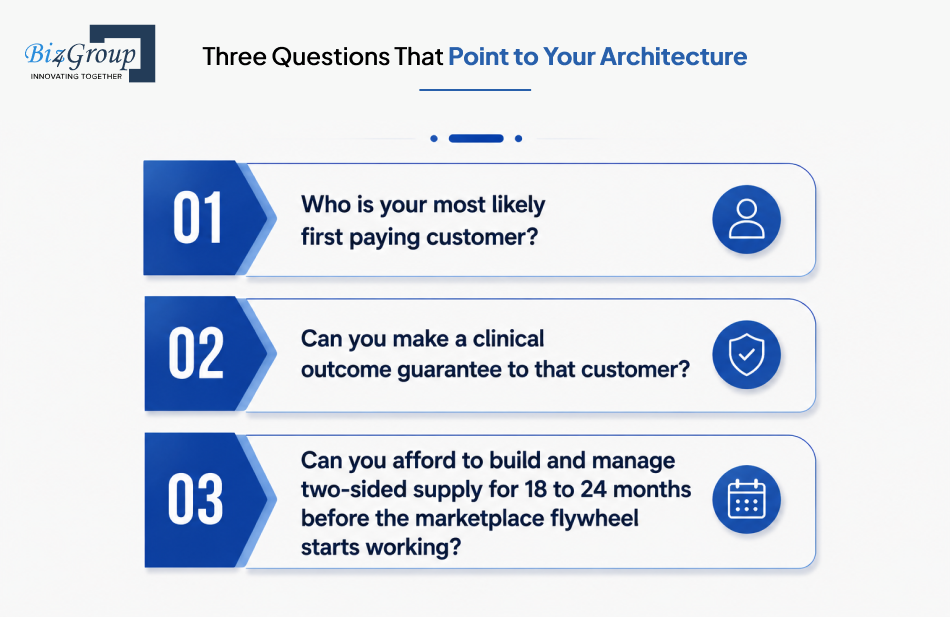

Ask yourself this: who is your first paying customer?

If the answer is an employer, a health plan, an employee assistance program, or any B2B buyer, the single provider teletherapy platform architecture is not optional. It's the only architecture that supports the sales motion, the compliance structure, and the clinical promises those buyers require.

It's also the right call if:

The MVP development path for a single-provider platform is also significantly more straightforward, letting you validate your clinical model and patient acquisition before committing to the full infrastructure investment.

Almost every founder asks about this at some point. Can we build a marketplace for general therapy and a single-provider model for specialized care? Can we start as single-provider and open up to independent contractors later?

The honest answer: hybrid models can work, but most of the time they don't, and the reason is always the same.

The data model becomes contradictory. When you try to run both models on the same infrastructure, you end up with a schema that serves neither model well, PHI ownership becomes ambiguous, compliance accountability splits in ways that are hard to defend, and the billing infrastructure tries to do two incompatible things simultaneously.

The one hybrid structure that genuinely works is a clean technical separation between two distinct service tiers:

A coaching and wellness marketplace for non-clinical services, independent contractors, no HIPAA, no insurance billing, straightforward commission model, and a licensed clinical therapy platform operating as a single-provider model with employed clinicians, full HIPAA accountability, and group practice billing.

The critical requirement is a hard technical wall between the two environments. Separate data models, separate authentication systems, separate billing infrastructure, and a clear patient-facing distinction between the two service tiers. If those walls don't exist at the architecture level, the hybrid model creates the compliance exposure of a marketplace with none of the commercial advantages of a single-provider platform.

If you're still uncertain after everything above, answer these three questions honestly:

Three questions. Your answers will point to the same architecture every time.

For founders who want to understand what healthcare SaaS solutions look like across both models before making the final call, it gives you the broader infrastructure context that sits underneath this architecture decision.

Here's a question worth asking any development partner before you sign anything: have you actually built both a teletherapy marketplace and a single-provider platform? Not read about them. Not adapted a generic healthcare template for one. Actually architected both from the ground up, navigated the credentialing API complexity, solved the multi-tenant PHI isolation problem, wired the split payment billing infrastructure, and delivered a fully compliant production build in both models?

Most can't say yes. And that matters enormously when the teletherapy marketplace vs single provider platform architecture decision is the one that determines your compliance structure, your revenue ceiling, and your investor story.

At Biz4Group, we've built both. 20+ of healthcare software development, 1,000+ projects delivered, and a specific depth in mental health platform architecture that comes from actually solving the hard problems, not theorizing about them. We've built the credentialing pipelines. We've navigated the BAA complexity at scale. We've architected multi-tenant data isolation that holds up under HIPAA scrutiny. We've built teletherapy marketplace scalability architecture that handles real provider and patient volume simultaneously, and we've built single provider teletherapy platform architecture that supports payer contracting, B2B employer sales, and outcome-based clinical reporting.

When founders come to us at the teletherapy platform business model architecture decision point, we don't lead with a recommendation. We lead with a compliance-first architecture review that maps your go-to-market, your clinical model, your funding stage, and your revenue channels to the platform structure that actually serves them. The recommendation follows the business, not our preferred tech stack.

That's the difference between a development partner who builds what you ask for and one who helps you ask the right question first.

The UI/UX design layer sits on top of all of it, because a platform that is architecturally sound but clinically unusable for patients or providers fails regardless of backend quality. We build both layers together, from the data model up through the patient and provider experience, so the architecture and the product work as one system.

If you're at the architecture decision point right now, hire mental health platform developers in USA at Biz4Group and get the architecture review before you commit to a single line of code.

Guessing is expensive. A conversation with Biz4Group isn't.

Book Your AppointmentEvery conversation about features, timelines, and costs in teletherapy platform development leads back to the same starting point. Which architecture are you building, and does it actually match the business you're trying to run?

The teletherapy marketplace vs single provider platform architecture decision is not a technical footnote. It determines your compliance structure, your revenue model, your clinical identity, and how investors read your business three years from now. Get it right and everything downstream gets easier. Get it wrong and the rebuild costs more than the original build.

Founders who make this call correctly aren't necessarily the ones with the biggest budgets or the most technical teams. They're the ones who made the architecture decision deliberately, with full information, before writing a single line of code.

The market is growing, the competition is intensifying, and the platforms that win won't be the ones that built the fastest. They'll be the ones that built the right thing first.

Build it right. Book a consultation with Biz4Group before architecture becomes the problem.

A teletherapy marketplace connects patients with independent licensed providers operating as separate businesses on your infrastructure. A single provider teletherapy platform is the care delivery entity itself, providers are employed, the platform owns the clinical relationship, billing, and compliance. The teletherapy app architecture marketplace vs single provider split runs through every layer of your system, from database schema to HIPAA liability to revenue model. These are not two versions of the same product.

Not without rebuilding. The teletherapy platform business model architecture decision is not a configuration you change after the fact. Your data model, billing infrastructure, provider contracts, and HIPAA BAA framework all have to change simultaneously. Founders who attempt this mid-build typically spend more on the rebuild than the original build. Validate your business model before committing to architecture, not after.

In a teletherapy marketplace platform, HIPAA liability is distributed across every independent provider, each requiring a separate BAA. When something goes wrong, untangling accountability across hundreds of distributed tenants is legally complex and expensive. In single provider teletherapy platform architecture, there is one covered entity, one BAA framework, one compliance posture. Accountability is clear from day one.

Single-provider, without question. Payers contract with entities not networks of independent contractors. B2B employer buyers require a single accountable clinical entity and outcome guarantees a marketplace structurally cannot provide. If insurance or employer channel sales are in your 24-month plan, single provider teletherapy platform architecture is the only model that makes those revenue channels genuinely accessible.

In a marketplace, the teletherapy platform provider matching algorithm is a full recommendation engine evaluating clinical need, provider specialty, state licensing compatibility, insurance status, and real-time availability simultaneously, starting rule-based and evolving toward ML as outcome data accumulates. In a single-provider platform, matching is a scheduling function. The platform has full clinical visibility without the data isolation constraints that make marketplace matching technically demanding.

Not inherently. Teletherapy marketplace scalability architecture scales two variables simultaneously, patient volume and provider count, each with its own infrastructure demands, database sharding, async credentialing queues, and event-driven scheduling across a constantly changing provider pool. Single-provider platforms scale one variable with more predictable infrastructure growth. Marketplaces are differently scalable, not automatically better, and most founders underestimate what scaling two variables simultaneously actually costs.

with Biz4Group today!

Our website require some cookies to function properly. Read our privacy policy to know more.