info@biz4group.com

info@biz4group.com

Imagine a digital system that doesn’t wait for instructions but instead, understands your business goals, learns from real-time feedback, and takes independent actions to get the job done.

Read More

AI Summary Powered by Biz4AI

AI Summary Powered by Biz4AI

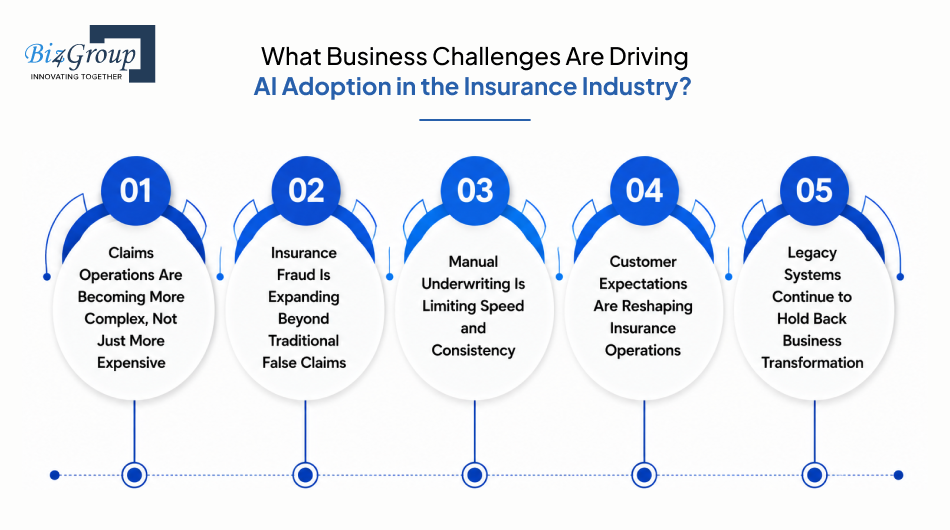

Why are insurers investing heavily in AI yet still struggling with slow claims, manual underwriting, and rising operational costs? The problem isn't a lack of AI adoption. It's knowing which AI use cases in insurance solve these challenges first and which ones simply add another pilot project to the list.

That question is shaping insurance strategies across the industry. As insurers look for practical ways to improve operational efficiency, the AI in insurance market is expected to grow from $13.94 billion in 2026 to $49.13 billion by 2030, expanding at a 37% CAGR. Yet growth in investment tells only part of the story. While 90% of insurance executives agree that work must be reinvented around AI, only 25% have translated that urgency into meaningful action.

So, if you're dealing with:

This blog will help you answer all these questions. Instead of discussing AI in theory, you'll see where insurers are applying it today, which use cases deserve priority and what real-world implementations look like. Let's dive in.

Every insurance leader is talking about AI, but the conversation usually starts much earlier with operational challenges that continue to slow growth, increase costs, and impact customer satisfaction. Perhaps you're asking, "I am a startup founder building an AI product for insurers and I want to know what gaps still exist in current AI use cases." The answer begins by understanding the business problems insurers are still trying to solve.

Take a look at what is driving the adoption:

Claims teams are expected to settle cases faster, yet every claim demands information from multiple sources, including policy records, repair estimates, medical reports, photographs, police reports, and third-party assessments. When this information is reviewed manually, adjusters spend valuable time validating documents instead of making claim decisions.

The growing complexity is becoming difficult to ignore. J.D. Power's U.S. Auto Claims Satisfaction Study found that 27% of all auto claims are now total-loss claims, increasing documentation requirements, stakeholder coordination, and settlement effort.

This creates operational pressure through:

Fraud today extends far beyond exaggerated repair bills or duplicate claims. Insurers increasingly deal with identity manipulation, organized fraud rings, fabricated documentation, and digitally coordinated fraud attempts that are harder to detect using manual review alone.

The financial impact reaches every stakeholder. According to the Coalition Against Insurance Fraud, insurance fraud costs consumers at least $308.6 billion every year. The FBI further estimates that, over a 10-year period, insurance fraud increases costs for the average U.S. family by $4,000 to $7,000 through higher insurance premiums.

These losses make fraud prevention an operational priority rather than simply an investigation function.

Modern underwriting depends on information collected from applications, inspection reports, financial statements, medical records, third-party databases, and regulatory documents. Reviewing this information manually increases turnaround time and often leaves experienced underwriters spending more time gathering data than evaluating risk.

As submission volumes grow, insurers face challenges such as:

Also Read: AI Insurance Underwriting Software Development Guide

Customers don't measure their insurance experience against another insurer anymore. They compare it with every digital service they use every day. They expect instant policy updates, real-time claim status, faster underwriting decisions, and personalized communication without repeatedly contacting support teams.

Meeting those expectations becomes difficult when customer information is spread across disconnected systems and every service request depends on manual intervention.

Operational challenges often include:

Many insurers have invested in digital initiatives over the years, but critical policy, claims, underwriting, and customer data often remains distributed across multiple legacy platforms. As a result, teams spend considerable time locating, validating, and reconciling information before work can even begin.

As Ben Woo, Deloitte China Insurance Digital Partner says, "The success of AI applications in insurance hinges on data quality, system modernization, and robust security. While the industry is buzzing with activity, realizing its full value remains a work in progress as many insurers contend with fragmented data and outdated systems."

Therefore, modernizing technology alone isn't enough when fragmented data continues to slow everyday operations.

As these operational demands continue to increase, insurers are looking beyond incremental process improvements and evaluating where artificial intelligence in insurance can remove bottlenecks, improve decision-making, and support sustainable business growth.

Let's identify where AI can remove friction before inefficiencies become expensive

Find Your Biggest AI OpportunityEvery insurer approaches AI with different priorities. Some begin with underwriting, while others focus on claims, customer service, or operational efficiency. The key is identifying the business challenge you want to solve first. The following AI use cases in insurance show where AI is already delivering measurable value across the insurance lifecycle.

Every policy recommendation influences both customer satisfaction and long-term retention, yet advisors often work with limited customer context when recommending coverage. By evaluating policy history, life events, financial profile, household details, and interaction patterns together, AI helps advisors identify coverage options that better match individual circumstances without extending consultation time.

The greatest value comes from helping advisors recommend coverage that reflects each customer's current circumstances rather than relying on standard product suggestions.

Operational Improvements:

Preparing a quote usually involves validating applicant information, checking eligibility, reviewing underwriting rules, and resolving missing details before a proposal can be shared. AI accelerates these activities by organizing application data, highlighting incomplete submissions, and preparing quote recommendations before they reach underwriting teams. The biggest impact is seen in organizations processing large volumes of personal or commercial insurance enquiries every day.

Operational Improvements:

Insurance fraud rarely appears as a single obvious red flag. Suspicious patterns often emerge only after comparing claims, policy history, supporting documents, and claimant behaviour. AI in insurance fraud detection continuously evaluates these signals as claims are submitted, helping investigators identify cases that deserve immediate attention before payments move further through the process.

Modern AI fraud detection systems can achieve upto 85–90% detection accuracy, while predictive analytics help insurers avoid an estimated 25–35% of potential fraud losses before payout. Deloitte estimates that by deploying AI real-time fraud analytics P&C insurers could save up to US$160 billion by 2032.

Operational Improvements:

Also Read: Voice AI Agent Development for Insurance Claim Fraud Detection

Not every enquiry deserves the same level of attention, but identifying serious buyers becomes increasingly difficult as lead volumes grow. AI evaluates behavioural signals, previous interactions, quote activity, and engagement history to identify prospects that deserve immediate attention, allowing sales teams to focus their efforts where conversion opportunities are strongest. This approach fits insurers and brokers managing high lead volumes across multiple acquisition channels.

Operational Improvements:

Customer needs evolve as families grow, businesses expand, vehicles change, or lifestyles shift, making broad marketing campaigns less effective over time. AI continuously groups policyholders based on changing characteristics, purchasing behaviour, policy portfolios, and engagement patterns so communication reflects current customer needs rather than static customer lists. This delivers the greatest value for insurers looking to strengthen long-term customer relationships through more relevant engagement.

Operational Improvements:

Every claim begins with collecting information, but incomplete forms, missing documents, and manual verification often delay the process before an adjuster starts reviewing the case. AI streamlines FNOL by capturing claim details, validating submissions, and flagging missing information during intake. This creates a cleaner starting point for the entire claims workflow.

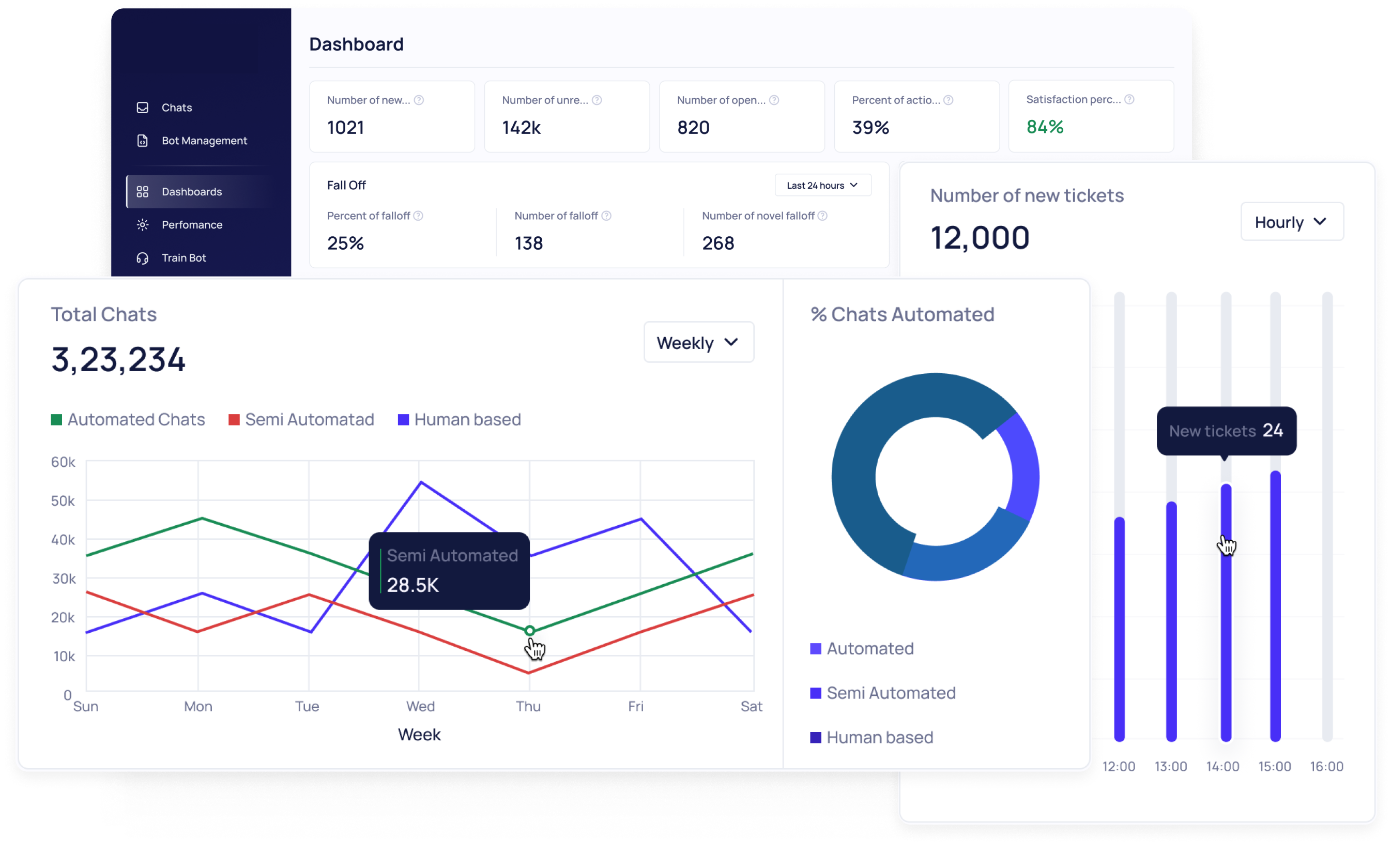

As AI adoption matures, around 50% of all claims are already handled through AI-driven systems, while routine claims are processed 40–60% faster, demonstrating how insurers are accelerating claim intake without compromising review quality.

Operational Improvements:

Also Read: Agentic AI vs Traditional FNOL for Insurance Claims Management

Underwriting teams rarely struggle because every submission is complex. The real challenge is that simple applications often sit in the same queue as high-risk cases, delaying decisions that require immediate expert attention.

AI reviews submission data, supporting documents, and predefined risk indicators as applications arrive. It allows underwriters to focus first on cases that genuinely require deeper assessment while straightforward submissions follow an accelerated review path. This approach is especially relevant for insurers managing growing application volumes with limited underwriting capacity.

Operational Improvements:

Commercial underwriting rarely depends on a single document. Risk decisions are often built from information scattered across ACORD forms, inspection reports, financial statements, loss histories, emails, and supporting records. This forces underwriters to spend considerable time locating information before assessment even begins.

Here, AI consolidates relevant details from these documents into a structured view, enabling underwriters to begin evaluating risk instead of searching for data. The workflow is particularly valuable for commercial and specialty insurers processing document-intensive submissions.

Operational Improvements:

Setting an appropriate reserve early in the claim is challenging when adjusters must balance incomplete information with potential future costs. Reserve decisions become more informed when historical claims, injury severity, repair estimates, and similar loss patterns are reviewed together by AI before financial commitments are made.

Insurers using predictive analytics report 15–20% lower operational costs and 3–5% better loss ratios, showing how stronger reserve planning can improve both financial control and claims management.

Operational Improvements:

Assessing risk becomes more challenging when historical claims, policy records, external datasets, and customer information must all be considered within limited review time. AI identifies patterns across these data sources and presents additional risk insights alongside the submission.

It gives underwriters broader context before making a final decision while preserving human oversight. This workflow delivers the greatest value where underwriting decisions depend on multiple sources of information rather than a single application.

Operational Improvements:

Pricing differences often arise because similar risks are evaluated by different underwriters, each interpreting available information slightly differently. AI analyzes applicant characteristics, claims history, policy performance, and relevant risk factors to recommend pricing ranges that support more consistent decision-making while leaving final authority with underwriting teams. The biggest impact is seen in insurers aiming to maintain pricing discipline across products, regions, and distribution channels.

Operational Improvements:

Property claims often remain on hold until an adjuster visits the site, even when policyholders have already submitted clear photos or videos of the damage. Visual evidence can be reviewed at the beginning of the assessment using AI, allowing the initial estimate to start before a physical inspection is scheduled.

Remote inspection tools and AI-powered image analysis support more than 35% of property claims assessments, helping insurers shorten assessment cycles without replacing expert judgement.

Operational Improvements:

Billing enquiries, policy updates, claim status requests, and endorsement changes continue long after a policy is issued. Handling every request manually reduces the time service teams can dedicate to customers facing complex situations.

Insurance AI agents resolve routine enquiries across web, mobile, and messaging channels while passing exceptions to advisors with the conversation history already available. Human representatives remain focused on policy advice, complaints, and cases that require judgement.

Operational Improvements:

Also Read: Top 10 AI Voice Agents for Insurance Companies in 2026

Renewal teams often realize a policyholder intends to leave only after a competing offer has influenced the decision. Changes in payment behaviour, service interactions, digital engagement, and policy activity done by AI often reveal early signs that a customer may be considering other options before renewal discussions begin.

These insights by AI enable retention teams to begin meaningful conversations before renewal decisions are finalized. The result is a more proactive retention strategy instead of reacting after customers have already disengaged.

Operational Improvements:

Renewing a policy should reflect how a customer's needs have changed since the last policy term. Standard renewal offers often overlook changes in driving habits, property ownership, family circumstances, or business operations.

Renewal recommendations are tailored by AI using updated customer information, policy history, and engagement patterns before the offer is presented. Among the most practical AI use cases for insurance customer experience and personalization, this helps insurers make renewal discussions more relevant instead of relying on one-size-fits-all offers.

Operational Improvements:

Service representatives frequently pause customer conversations to search policy documents, underwriting guidelines, product manuals, or internal knowledge bases. Finding accurate information quickly becomes difficult when content is spread across multiple systems.

AI-powered knowledge assistants surface relevant answers within the agent's workflow, reducing unnecessary searches while keeping employees in control of customer interactions. This is particularly valuable for insurers supporting multiple products, regions, or distribution channels.

Operational Improvements:

Also Read: Develop AI Virtual Assistant: Features & Implementation Tips

Insurance regulations continue to evolve across underwriting, claims, policy administration, and customer communications. Reviewing every workflow manually leaves compliance teams spending valuable time on routine checks instead of higher-risk exceptions.

AI evaluates policies, documents, and customer communications against predefined compliance requirements, highlighting potential issues before internal audits or regulatory reviews begin. Among the most practical insurance AI implementation examples, this use case strengthens governance while allowing day-to-day operations to continue without unnecessary disruption.

Operational Improvements:

Insurance leaders rely on data from underwriting, claims, customer service, finance, and sales to monitor business performance. Preparing these reports often requires collecting information from multiple systems before meaningful analysis can begin.

AI consolidates operational data into business-ready summaries, enabling leadership teams to review performance trends and make faster decisions without waiting for manual reporting cycles. This is one of the more valuable examples of AI transforming insurance operations because it supports decision-making across the entire organization rather than a single department.

Operational Improvements:

A major storm, wildfire, or flood can generate thousands of claims within hours, placing immediate pressure on claims teams, field adjusters, and customer support. Responding effectively depends on knowing where resources are needed first and how claim volumes are likely to develop.

AI analyzes incoming claims, location data, weather information, and operational capacity to support faster response planning during catastrophe events. Insurers using AI-powered analytics and automation have reported 60–70% higher claims team productivity, helping them maintain service levels when claim volumes surge. Among the most practical AI insurance solutions, this use case strengthens operational resilience during large-scale loss events.

Operational Improvements:

Workloads rarely increase at the same pace across underwriting, claims, customer service, and policy administration. Hiring additional staff after backlogs appear often comes too late to maintain service levels.

Analysis of historical workloads, seasonal trends, renewal cycles, and business activity by AI provides early indicators of future demand, helping operational leaders plan staffing before pressure builds. This becomes especially valuable for insurers advancing insurance digital transformation use cases with AI across multiple business functions, particularly when modernizing operations around legacy environments and expanding AI adoption.

Operational Improvements:

Not every insurer needs all use cases from day one. The right starting point depends on your business goals, operational gaps, and digital maturity. Once those priorities are clear, artificial intelligence in insurance becomes a practical investment that delivers measurable business outcomes rather than isolated automation projects.

Find the AI use cases that deliver measurable impact for your insurance business first

Prioritize Your AI RoadmapUnderstanding where AI can be applied is only one part of the decision. The next step is seeing how insurers are putting those insurance AI use cases into practice. These real-world examples show how leading insurance companies have deployed AI to solve operational challenges and deliver measurable business outcomes.

AIG Insurance is a leading U.S.-based global insurer that is scaling AI across underwriting and claims to modernize core insurance workflows and improve operational efficiency.

Business Challenge: Commercial underwriting required reviewing large volumes of structured and unstructured submission data before coverage decisions could be made.

To address this, AIG developed AIG Assist, an AI platform embedded into underwriting and claims workflows. The platform helps organize complex submission data, supports underwriting decisions, accelerates first notice of loss (FNOL), and improves coverage analysis while maintaining human oversight for final decisions.

Business Outcomes:

Lemonade is a U.S.-based digital insurer that has built its insurance platform around proprietary AI assistants to automate customer onboarding, policy servicing, and claims processing.

Business Challenge: Lemonade wanted to simplify the insurance experience by removing friction from policy purchases and claims handling.

It developed conversational AI agent known as, AI Maya which coordinates with other autonomous bot AI Jim, to automate customer onboarding, first notice of loss (FNOL), and claims workflows. Complex claims are automatically escalated to human experts after AI completes the initial assessment and routing.

Business Outcomes:

Travelers is one of the largest U.S. property and casualty (P&C) insurers, using AI across claims, underwriting, and customer service to modernize insurance operations and improve employee productivity.

Business Challenge: Handling large claim volumes and data-intensive underwriting required faster and more consistent workflows.

Travelers embedded AI into claims intake, straight-through claims processing, underwriting analysis, and digital customer interactions. The company also introduced a generative AI-powered voice assistant for first notice of loss (FNOL), helping automate routine claims while enabling claims professionals to focus on more complex cases.

Business Outcomes:

Aviva is one of the UK's leading insurers, using AI across its claims operations to improve efficiency, fraud detection, and customer experience.

Business Challenge: Claims operations involved repetitive manual activities that slowed customer service and fraud investigations.

Aviva introduced AI across its claims workflow, including GenAI-powered claims summarization, call-wrap capabilities, and 12 AI-driven fraud detection models. This helped claims handlers process cases more efficiently while allowing specialists to focus on high-value and complex decisions.

Business Outcomes:

Ping An is one of the world's largest insurance and financial services groups, embedding AI across underwriting, claims, customer service, and risk management to support large-scale insurance operations.

Business Challenge: Managing millions of insurance interactions required Ping An to improve efficiency across the entire insurance lifecycle.

The company integrated AI into underwriting, claims settlement, fraud detection, and customer service. It uses intelligent automation to accelerate routine insurance processes while allowing employees to focus on higher-value decisions and complex customer cases.

Business Outcomes:

These real-world examples of AI in insurance show that successful AI adoption isn't defined by the number of models an insurer deploys. It comes from solving the right business problems with measurable results. The next step is identifying which AI initiatives align best with your organization's priorities, operational challenges, and long-term growth strategy.

Turn proven AI strategies into practical solutions built around your insurance operations

Start Your AI Game Plan

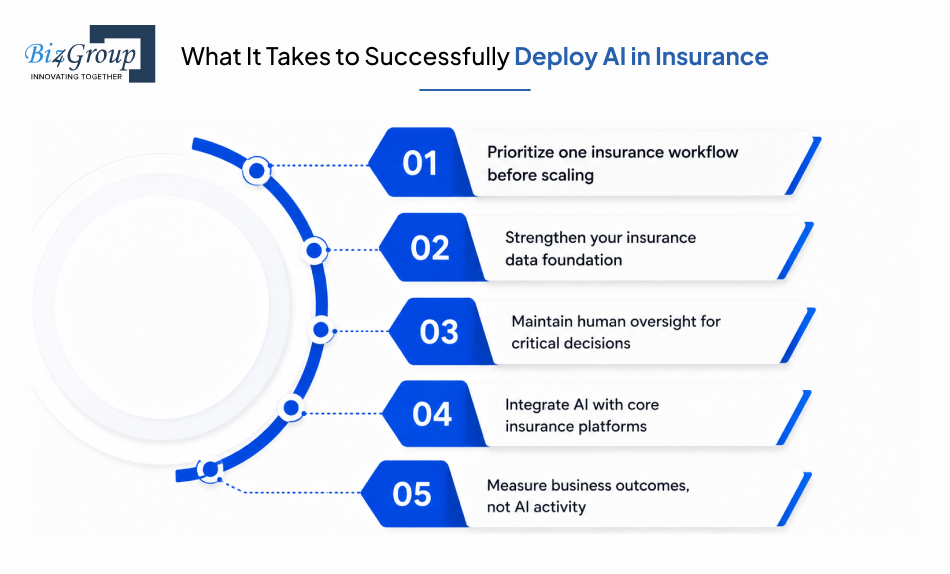

Successful AI adoption depends on more than choosing the right technology. To maximize the value of AI use cases in Insurance in 2026, insurers need the right operational foundation before scaling across the business.

The following insurance AI application practices help you achieve the business outcome you are aiming for:

Turning AI initiatives into production-ready insurance solutions requires expertise beyond model development. From modernizing claims and underwriting to building secure AI insurance automation software solutions, working with a partner that understands insurance operations makes implementation more effective. An AI development company such as Biz4Group LLC can help insurers and insurtech businesses build AI solutions aligned with real operational challenges. Have we built any?

Yes, we have! Take a look:

1. Insurance AI: Transforming Insurance Training with AI

Insurance AI is an AI-powered insurance training assistant developed for a senior insurance leader to help train and support insurance teams through conversational AI. Powered by GPT-4o and GPT-3.5, it delivers instant responses using custom-trained organizational knowledge, continuously improves through user feedback. It maintains interaction history, and integrates with existing web interfaces to provide consistent insurance guidance.

Here's what we offer more:

The future of insurance isn't about adopting AI everywhere at once. It's about identifying the right opportunities, solving real business challenges, and scaling solutions that create measurable value. Organizations that approach AI use cases in Insurance with a clear strategy, reliable data, and a focus on business outcomes will be better positioned to improve operational efficiency and customer experiences while staying competitive in a rapidly evolving market.

If you're evaluating where to begin or planning your next AI initiative, the right guidance can make all the difference. Biz4Group LLC's AI consulting services help insurers assess opportunities, define practical implementation strategies, and build solutions aligned with their business goals. Schedule a strategy call with our team and explore how AI can create measurable impact across your insurance operations.

The success of AI should be measured against business outcomes rather than technology adoption. Common KPIs include claims processing time, underwriting turnaround, fraud detection accuracy, policy renewal rates, customer satisfaction, operational costs, and employee productivity. Tracking these metrics before and after deployment helps insurers evaluate whether AI investments are delivering measurable business value.

AI models perform best when trained on diverse, high-quality insurance data, including policy records, claims history, underwriting information, customer interactions, loss reports, fraud cases, and regulatory documents. Clean, well-governed, and representative datasets improve prediction accuracy while reducing bias and inconsistent decision-making.

Yes. In personal insurance, AI is commonly used for claims automation, customer support, fraud detection, and policy servicing. In commercial insurance, it helps evaluate complex risks, analyze submissions, automate underwriting workflows, review policy documents, and support loss prevention across larger, more specialized portfolios.

Most insurers don't need to replace their existing technology stack. Instead, they can modernize gradually by improving data quality, exposing system APIs, integrating cloud services, and connecting AI with policy administration, claims management, and customer relationship platforms. This approach minimizes disruption while enabling AI adoption.

Common risks include poor data quality, biased AI models, regulatory non-compliance, limited system integration, and insufficient human oversight. Establishing governance policies, validating AI outputs regularly, and maintaining transparency in decision-making helps insurers reduce these risks while building trust with customers and regulators.

AI is expected to become a standard capability across underwriting, claims, customer service, fraud detection, and risk management. Future innovation will focus on intelligent automation, real-time decision support, personalized policy experiences, and greater collaboration between AI systems and insurance professionals rather than replacing human expertise.

Our website require some cookies to function properly. Read our privacy policy to know more.