info@biz4group.com

info@biz4group.com

Imagine a digital system that doesn’t wait for instructions but instead, understands your business goals, learns from real-time feedback, and takes independent actions to get the job done.

Read More

How are insurers planning to evaluate complex risk profiles while policy volumes continue to grow each year? Underwriting teams are under constant pressure to review applications quickly while maintaining consistent risk decisions.

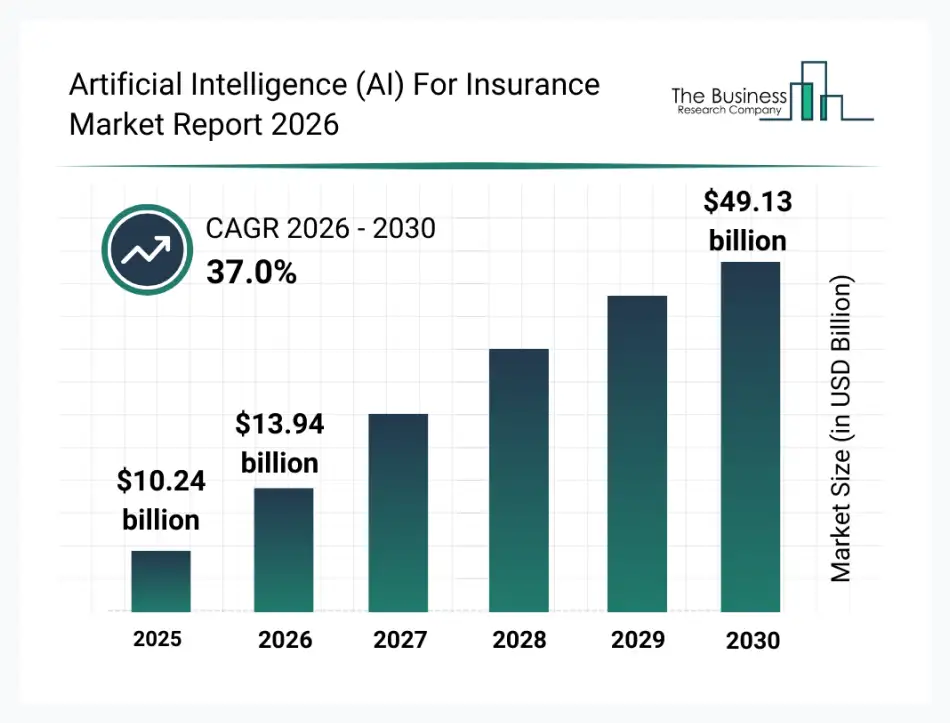

Market data reflects how strongly the industry is investing in intelligent underwriting technologies. The artificial intelligence market in the insurance sector is projected to reach $13.94 billion in 2026 and $49.13 billion by 2030 with a compound annual growth rate of 37.0%.

This rapid growth signals a shift in how underwriting systems operate inside insurance organizations. Digital platforms now analyze applicant data, claim histories, and risk indicators before underwriters make final policy decisions. These systems help insurers organize underwriting workflows while keeping evaluation standards consistent.

Here’s what you should know:

Organizations that plan AI insurance underwriting software development focus on building systems that assist underwriters with structured risk insights rather than replacing human judgment during policy evaluation.

Let’s dive further for more insights.

AI insurance underwriting software is a digital platform that evaluates insurance applications using structured data analysis and automated decision logic. Instead of relying only on manual review, the system analyzes applicant information and historical risk patterns before supporting underwriting decisions.

Insurers use this technology to review large volumes of policy applications while maintaining consistent risk evaluation. Many insurers investing in AI insurance underwriting software development implement these systems to support underwriting teams and reduce repetitive review work through controlled AI automation tools.

Insurance leaders usually evaluate technology investments through financial outcomes and operational efficiency. Many organizations begin AI insurance underwriting software development initiatives when underwriting delays, rising costs, and inconsistent risk decisions begin affecting profitability.

Before we understand the reasons to invest in AI insurance underwriting software, take a look at what AI in insurance statistics have to say:

These numbers clearly show where insurers are seeing measurable financial impact today. Now, here are why you should invest in AI insurance underwriting software development:

AI insurance underwriting software analyzes applications quickly and allows insurers to process more policy requests. Higher approval throughput enables companies to increase premium revenue without expanding underwriting teams.

Manual underwriting involves document review, risk calculations, and application verification. Automation reduces repetitive tasks and lowers administrative overhead, helping insurers improve margins through structured enterprise AI solutions.

Fraudulent applications create direct financial losses when high-risk policies enter the portfolio. AI risk evaluation identifies suspicious data patterns early, helping insurers prevent expensive claims exposure and protect underwriting revenue.

AI insurance underwriting models analyze claim history and applicant behavior before policy approval. Accurate pricing ensures premiums reflect real risk exposure, allowing insurers to maintain stronger margins across their underwriting portfolio.

AI automated insurance underwriting platforms process higher policy volumes without proportional operational cost increases. This allows insurers to expand product offerings and enter new markets while maintaining stable underwriting efficiency.

Organizations investing in intelligent underwriting platforms usually focus on financial outcomes such as revenue protection, cost efficiency, and scalable policy growth. These goals often drive long-term investment in AI insurance underwriting software development.

Also Read: AI Automation Use Cases for Enterprises to Scale Faster

Discover how intelligent underwriting platforms unlock faster approvals higher premium growth and stronger risk control

Talk To Our AI Experts

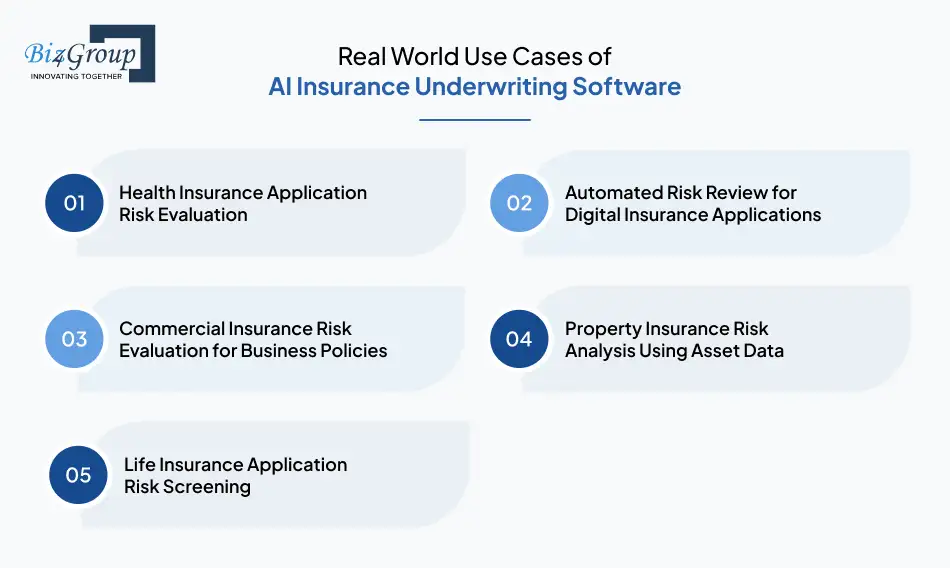

Insurance underwriting scenarios vary widely across product lines and risk categories. Organizations investing in AI insurance underwriting software development usually focus on practical underwriting situations where risk evaluation requires faster data analysis and consistent decision logic.

Health insurers handle large volumes of applications that require reviewing medical history, lifestyle information, and claim patterns. Underwriting teams increasingly rely on automated systems to review these datasets during policy evaluation.

Digital insurance platforms receive policy applications through mobile portals and online forms. Underwriting teams must evaluate these applications quickly while maintaining risk accuracy.

Commercial policies require evaluating multiple operational risks before issuing coverage. Underwriters often review financial records, operational details, and industry exposure.

Property insurers review location data, property details, and historical claims before issuing coverage. Automated systems help underwriters analyze these factors quickly.

Life insurance underwriting requires reviewing medical background, lifestyle factors, and demographic information before policy approval.

Insurance companies implement underwriting automation around specific policy evaluation scenarios rather than generic automation goals. Many organizations adopt these platforms when they create AI insurance risk assessment software designed to support real underwriting decisions across different insurance products.

Insurance organizations approach underwriting modernization in different ways depending on their existing systems and operational goals. When planning AI insurance underwriting software development, decision makers usually evaluate whether to build internally, integrate with existing systems, or adapt custom or off the shelf software to support underwriting workflows.

Building an AI insurance underwriting platform from the ground up gives insurers full control over system architecture and underwriting logic. This approach is common for companies that want proprietary underwriting models or unique policy evaluation rules. Development teams design the entire platform including risk scoring engines, underwriting workflows, and policy decision rules.

Organizations often follow this path when underwriting strategies vary across product lines or regions. Engineering teams working on AI insurance software development can design data pipelines and risk models tailored to their underwriting approach.

Many insurers operate legacy underwriting platforms that already manage policy applications and customer records. Instead of replacing these systems, organizations often integrate AI capabilities into existing infrastructure. AI models analyze application data and generate risk insights while the legacy platform continues handling policy management tasks.

This approach allows underwriting teams to modernize decision workflows without replacing operational systems. AI Integration typically focus on connecting risk models, document processing services, and data providers with the existing underwriting platform.

Some insurers require flexibility that sits between full development and simple integration. In these cases, development teams adapt frameworks or platforms around operational underwriting needs. Organizations pursuing custom AI insurance underwriting software development often start with a base system and modify workflows, risk scoring models, and compliance rules.

This approach helps insurers scale underwriting automation while maintaining alignment with existing operational practices. Customization is particularly useful when insurers expand into new product categories or regulatory environments.

Organizations usually evaluate internal systems, underwriting complexity, and long-term technology strategy before selecting the most appropriate development approach.

|

Development Approach |

Best Fit Scenario |

Key Advantage |

|---|---|---|

|

Build From Scratch |

Insurers with complex underwriting models |

Full control over underwriting architecture |

|

Integrate AI Capabilities |

Organizations with established legacy systems |

Faster modernization without system replacement |

|

Customize Platforms |

Insurers expanding underwriting capabilities |

Flexible platform aligned with business workflows |

Selecting the right strategy helps insurers align technology investments with underwriting operations. Many organizations eventually transition toward custom AI insurance underwriting automation software development as underwriting requirements expand and risk evaluation models require deeper customization.

Also Read: How to Develop an Insurtech SaaS Product from Idea to Market?

Discuss your underwriting workflows data systems and scaling goals with specialists building modern insurance platforms

Schedule Strategy DiscussionModern underwriting platforms help insurers process large volumes of applications while maintaining consistent risk evaluation. Organizations investing in AI insurance underwriting software development typically focus on features that automate data analysis, support underwriters, and streamline policy decision workflows.

|

Key Feature |

What the Feature Does |

|---|---|

|

Automated Risk Scoring |

Evaluates applicant data and predicts claim probability using trained risk models. The system generates underwriting scores that guide approval decisions. |

|

Intelligent Document Processing |

Extracts relevant information from policy forms, medical records, and supporting documents. This removes manual data entry during underwriting review. |

|

Fraud Detection Monitoring |

Identifies suspicious data patterns in applications or supporting documents. Early detection helps insurers investigate high risk submissions before policy approval. |

|

Underwriting Workflow Automation |

Automates routine underwriting tasks such as risk review routing, approval steps, and policy validation processes. |

|

Real Time Risk Evaluation |

Processes incoming application data immediately and calculates risk scores during the underwriting process. |

|

Data Integration with External Sources |

Connects the underwriting platform with credit databases, telematics providers, and medical data services for broader risk insights. |

|

Underwriter Decision Support |

Presents structured risk summaries that help underwriters review applicant profiles and finalize policy decisions faster. |

|

Policy Rule Management |

Allows insurers to configure underwriting rules, approval thresholds, and compliance policies inside the platform. |

|

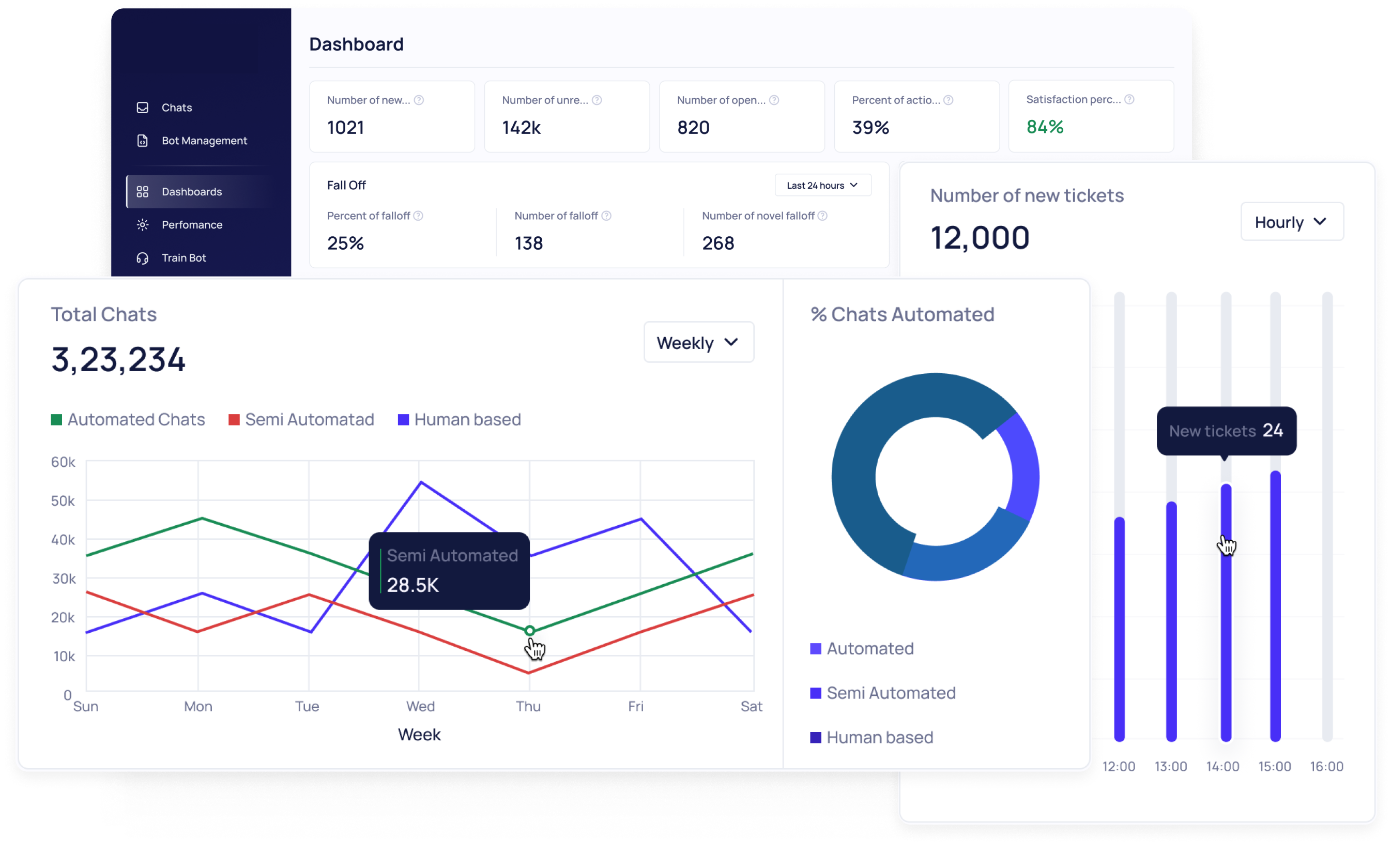

Risk Analytics Dashboard |

Displays underwriting metrics, policy risk distribution, and operational insights that help underwriting teams monitor performance. |

|

Model Learning and Improvement |

Continuously improves risk prediction models using new claims data and underwriting outcomes. |

These capabilities allow insurers to evaluate applications faster, reduce manual review work, and maintain consistent underwriting standards. Many insurers now prioritize these capabilities when investing in insurance underwriting automation software development.

Insurance underwriting platforms are evolving beyond basic automation. Modern systems now analyze larger datasets and identify deeper risk signals. These technologies help insurers create intelligent insurance underwriting solutions that support faster underwriting decisions while maintaining strong risk evaluation accuracy.

|

Advanced AI Capability |

What the Capability Does |

|---|---|

|

Machine Learning Risk Prediction Models |

Uses historical claims data and policy outcomes to estimate future risk levels. These models support underwriting decisions by applying predictive analysis to applicant data and policy information. |

|

Natural Language Processing for Insurance Documents |

Reads unstructured documents such as policy applications, inspection reports, and medical records. The system extracts relevant risk information so underwriters do not manually review every document. |

|

Computer Vision for Property and Asset Verification |

Analyzes images submitted during policy applications. Property photos, vehicle images, or inspection pictures can be evaluated to detect visible damage or risk indicators. |

|

Behavioral Risk Pattern Analysis |

Studies behavioral signals such as driving habits or usage data collected from connected devices. These insights help underwriting teams evaluate long term risk exposure. |

|

Claims Pattern Intelligence |

Reviews historical claim trends to detect unusual patterns across industries, locations, or policy categories. These insights help underwriting teams adjust risk thresholds during policy evaluation. |

|

Generative AI Underwriting Assistance |

Underwriters often review large datasets when assessing policy risk. Systems using generative AI can summarize risk signals and highlight unusual data patterns that require further underwriting attention. |

|

Risk Scenario Simulation |

Simulates different underwriting scenarios using historical data patterns. This allows insurers to evaluate potential outcomes before approving complex policy applications. |

Advanced analytics capabilities allow underwriting platforms to analyze more data sources while supporting faster policy evaluation. As insurers continue investing in AI insurance underwriting software development, these technologies help create intelligent insurance underwriting solutions that strengthen risk evaluation and operational efficiency.

Also Read: Building Effective Generative AI Solutions

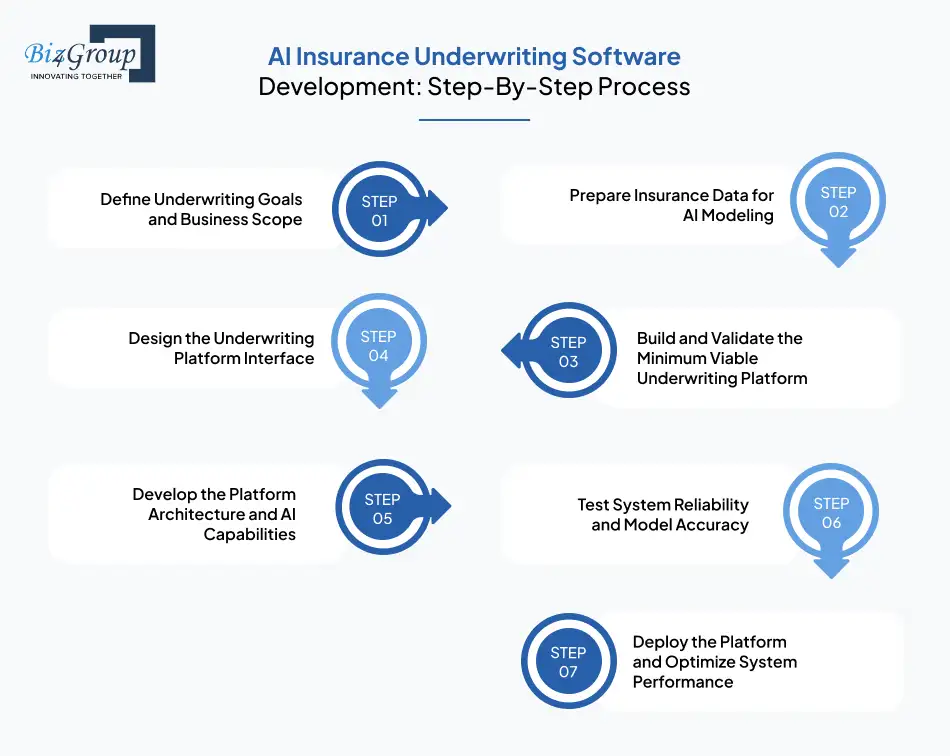

Insurance companies adopting AI underwriting usually begin with a clear operational roadmap. A structured process helps teams align underwriting workflows, risk evaluation logic, and automation goals before development begins. Organizations that plan carefully are better positioned to develop enterprise grade AI insurance underwriting software solutions that support scalable underwriting operations.

Also Read: Top MVP Development Companies in USA

Also Read: Top UI/UX design companies in USA

Successfully implementing these steps helps insurers build reliable underwriting platforms that improve risk evaluation, reduce manual review effort, and support scalable policy processing. This structured roadmap provides the foundation for effective AI insurance underwriting software development.

Insurance underwriting platforms handle sensitive policy data and large risk datasets every day. Organizations planning to build AI insurance underwriting software for insurers usually rely on structured system layers aligned with modern web/mobile app development practices to ensure stability, scalability, and smooth underwriting operations.

|

Architecture Layer |

Recommended Technology |

Purpose |

|---|---|---|

|

Presentation Layer |

React.js |

Builds underwriting dashboards where analysts review policy submissions and risk insights during ReactJS development. |

|

Frontend Framework |

Next.js |

Supports faster navigation and scalable user interfaces implemented during NextJS development for underwriting portals handling large policy volumes. |

|

Application Layer |

Node.js |

Handles underwriting workflows, application processing, and service coordination through structured NodeJS development. |

|

AI & Risk Modeling Layer |

Python, TensorFlow, Scikit-learn |

Supports risk prediction models and automated underwriting calculations created through Python development. |

|

Integration Layer |

REST APIs, GraphQL |

Enables communication between underwriting software, policy systems, and external data sources through structured API development. |

|

Data Storage Layer |

PostgreSQL, MongoDB |

Stores policy applications, underwriting outcomes, and customer risk profiles used during risk evaluation. |

|

Data Processing Layer |

Apache Spark, Apache Airflow |

Processes insurance datasets and prepares structured data used by underwriting risk models. |

|

Security Layer |

OAuth, IAM policies |

Protects customer information and controls access to underwriting systems. |

|

Infrastructure Layer |

AWS, Microsoft Azure, Google Cloud |

Hosts underwriting platforms in secure environments that support scalable operations. |

When these architecture layers operate together, insurers can process applications efficiently while maintaining reliable risk analysis. Successful AI insurance underwriting software development often depends on coordinated full stack development that supports scalable underwriting workflows and data driven decision systems.

Work with architects designing secure scalable underwriting platforms that integrate seamlessly with insurance ecosystems

Speak With Solution Architects

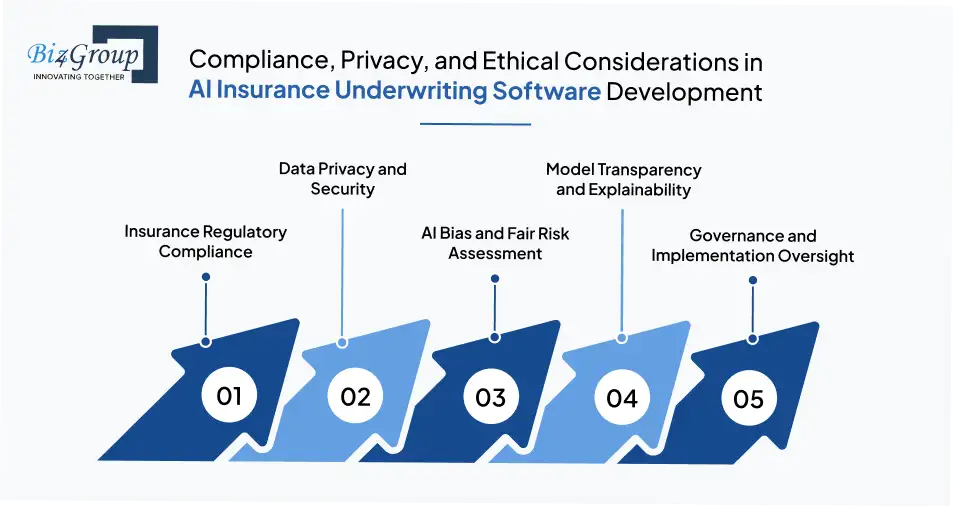

Insurance underwriting platforms handle personal records, financial information, and risk data. Companies that make AI underwriting software with insurance fraud detection features must design systems that respect regulations, protect customer data, and maintain fair decision processes from the start.

AI insurance underwriting decisions are governed by strict regulatory frameworks. Automated systems must follow the same underwriting guidelines that regulators expect from human underwriters.

These controls help insurers avoid compliance risks when deploying automated underwriting systems.

AI insurance underwriting platforms collect sensitive information such as health records, financial details, and personal identifiers. Protecting that data is essential for maintaining trust and regulatory alignment.

Strong privacy practices reduce exposure to data breaches and regulatory penalties.

AI models rely on historical data to predict risk. If those datasets contain hidden bias the system may produce unfair underwriting outcomes.

Fair model evaluation protects insurers from discrimination risks and regulatory concerns.

Underwriters must understand how automated systems generate risk scores and policy recommendations. Clear explanations help teams review decisions before approving policies.

Transparent decision processes strengthen internal governance and regulatory confidence.

Responsible deployment requires careful planning and oversight throughout the development process. Many insurers collaborate with experienced teams by hiring AI developers to build compliant underwriting models while guiding implementation through structured AI consulting services.

Compliance planning, responsible data management, and transparent decision logic help insurers deploy underwriting platforms with confidence. These practices remain essential for organizations pursuing long-term AI insurance underwriting software development.

Insurance companies planning AI insurance underwriting automation software development often evaluate the overall investment early in the project. Development cost usually ranges between $40,000 and $250,000+, depending on platform complexity, automation scope, and integration requirements.

|

Development Level |

Scope |

Estimated Cost Range |

|---|---|---|

|

MVP Level AI Insurance Underwriting Software |

Basic underwriting workflow automation, risk scoring models, limited integrations with policy systems, and simple underwriting dashboards for testing automation feasibility. |

$40,000 – $70,000 |

|

Mid-Level AI Insurance Underwriting Software |

Expanded underwriting automation, improved risk models, multiple data integrations, fraud detection support, and advanced analytics dashboards for underwriting teams. |

$70,000 – $130,000 |

|

Advanced AI Insurance Underwriting Software |

Enterprise underwriting automation, complex risk prediction models, large scale integrations, compliance features, and intelligent underwriting analytics capabilities. |

$130,000 – $250,000+ |

A structured development strategy helps insurers control project budgets while still delivering reliable underwriting automation capabilities. Careful planning and phased implementation remain essential for successful AI insurance underwriting software development.

Also Read: Cost to Hire an AI Software Developer

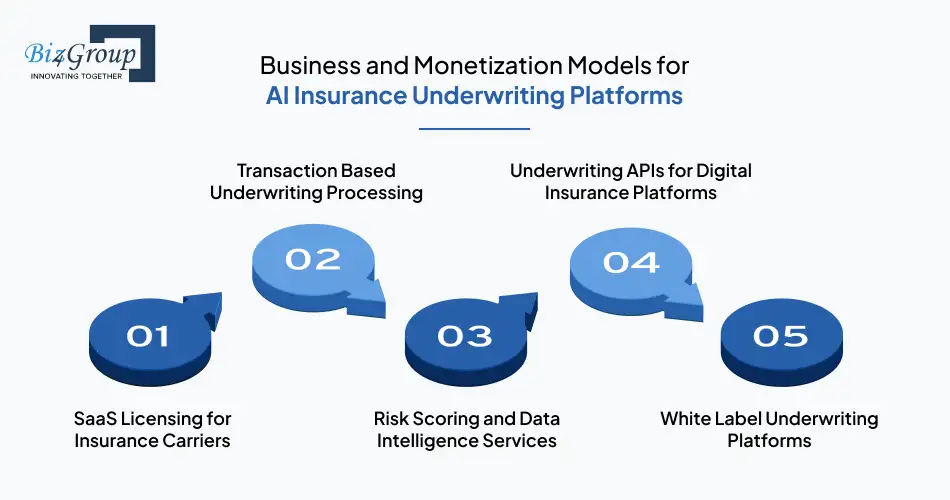

Companies building underwriting automation platforms can design the product with clear revenue pathways from the beginning. AI insurance underwriting software development for insurtech startups frequently focuses on scalable platforms that insurers, MGAs, and digital insurance providers can adopt across their underwriting workflows.

Many companies commercialize AI insurance underwriting platforms as subscription software used directly by insurers. This model generates recurring revenue while insurers pay for access to underwriting automation capabilities.

This approach allows underwriting technology providers to build predictable recurring revenue streams.

Some platforms generate revenue by charging for each underwriting decision processed through the system. This model works well for insurers that handle fluctuating application volumes.

Revenue grows directly with underwriting transaction activity.

AI insurance underwriting platforms can also generate revenue by offering risk intelligence services built from underwriting data. Insurers pay for advanced analytics that help them evaluate portfolio risk.

These services transform underwriting data into valuable analytical products.

Many insurtech companies embed underwriting technology directly into other insurance platforms through APIs. Revenue comes from API usage and integration partnerships.

This model expands underwriting technology across multiple insurance products.

Some technology providers license their AI insurance underwriting platforms to insurers who want to launch their own branded underwriting systems.

White label licensing allows insurers to deploy automated underwriting platforms without building internal technology teams.

Revenue generation models continue evolving as insurers adopt underwriting automation platforms across their operations. Clear monetization strategies help technology providers build sustainable businesses around AI insurance underwriting software development.

Discover monetization strategies insurers use to generate revenue from underwriting analytics automation and platform licensing

Explore Revenue OpportunitiesInsurance platforms often fail when teams rush into development without aligning data readiness, underwriting workflows, and operational goals. During AI underwriting software product development, these mistakes usually appear early and create long-term operational problems if ignored.

|

Common Mistake |

How to Avoid It |

|---|---|

|

Building models without reliable underwriting data |

Prepare structured datasets before development begins. Review historical claims data and remove incomplete records before teams build AI software for underwriting automation. |

|

Automating underwriting decisions too aggressively |

Introduce automation gradually. Allow underwriters to review flagged applications before the system generates final policy decisions. |

|

Ignoring integration with existing insurance systems |

Plan system integrations early. Work with engineers who understand insurance infrastructure or partner with a reliable custom software development company. |

|

Lack of fraud detection capabilities |

Include fraud analysis rules and anomaly detection models during development to flag unusual underwriting patterns. |

|

Overlooking regulatory and compliance requirements |

Document underwriting rules clearly and ensure automated decisions follow regulatory guidelines before deployment. |

|

No monitoring after deployment |

Track underwriting outcomes and retrain models regularly using new claims and policy data. |

Avoiding these challenges requires structured planning and experienced technical execution. Organizations often collaborate with an experienced AI underwriting software development company to reduce risks and implement reliable underwriting platforms that support long-term AI insurance underwriting software development.

Insurance underwriting platforms require careful planning, reliable data pipelines, and scalable system architecture. As a software development company in Florida, Biz4group LLC works closely with insurers and insurtech teams that need dependable AI insurance underwriting software development services tailored to real underwriting operations.

Insurance AI was designed as an AI-powered training assistant for insurance agents. It helps agents learn policy guidelines, understand insurance products, and receive instant answers during onboarding and daily operations.

The system uses conversational AI to simulate real support scenarios and guide agents through complex policy information. This kind of automation shows how intelligent tools can support insurance operations while reducing dependency on manual training processes.

Building reliable underwriting platforms requires both engineering depth and insurance domain understanding. Thus, our teams work closely with insurers and insurtech companies to deliver practical platforms that support scalable AI insurance underwriting software development.

Work with engineers delivering scalable underwriting platforms trusted by insurers building intelligent risk evaluation systems

Start Your AI Underwriting ProjectInsurance underwriting is changing quickly as insurers look for faster and more reliable ways to evaluate risk. Building the right system requires thoughtful planning around data, workflows, and regulatory responsibilities. Teams that work with an experienced AI product development company approach this process with a clearer roadmap and fewer implementation risks.

Business owners planning to develop AI underwriting software for insurance companies should focus on practical underwriting operations rather than isolated automation features. The goal is to create systems that help underwriting teams evaluate policies efficiently while maintaining accuracy and regulatory confidence.

Every insurer approaches underwriting differently. That is why AI insurance underwriting software development should align closely with real operational workflows. If you are considering building such a platform, scheduling a short conversation with our team can help clarify the next practical steps.

Insurance leaders should first evaluate underwriting workflows, data availability, and regulatory requirements. A successful platform depends on clean historical claims data, clearly defined risk rules, and integration with policy administration systems. Early planning helps insurers avoid costly redesigns later in the development process.

Most insurers already run policy administration, claims management, and CRM platforms. Development teams usually connect AI underwriting systems through secure APIs that allow data exchange with these systems. This integration ensures risk scores, policy approvals, and underwriting decisions update automatically across the insurance ecosystem.

Executives should prioritize risk scoring models, automated document analysis, fraud detection capabilities, and underwriting workflow automation. Platforms should also support real-time data integration with external sources such as credit data, telematics, or medical records. These capabilities help underwriters evaluate risk faster and improve policy decision accuracy.

Effective risk assessment systems combine historical claims data, customer profiles, and predictive modeling. Machine learning models analyze patterns across large datasets to estimate claim probability and risk exposure. Over time, model performance improves as new claims outcomes and underwriting decisions feed back into the system.

The cost to develop AI insurance underwriting software for insurers typically depends on system scope, data infrastructure, and integrations with existing insurance platforms and typically ranges between $40,000 and $250,000+.

Startups often focus on modular platforms that launch quickly and scale over time. They usually begin with core underwriting automation and predictive risk models. As the product grows, they expand the platform with advanced analytics, fraud detection, and integrations with partner insurers.

with Biz4Group today!

Our website require some cookies to function properly. Read our privacy policy to know more.