info@biz4group.com

info@biz4group.com

Imagine a digital system that doesn’t wait for instructions but instead, understands your business goals, learns from real-time feedback, and takes independent actions to get the job done.

Read More

Building a fintech assistant app development like Cleo AI is a real business opportunity. Cleo shows that people want fast, personal financial guidance, not just basic budgeting tools. Copying features alone will not make an app successful. Founders need to understand how Cleo works, why users stick with it, and which technical and business choices matter.

Cleo is an AI financial assistant app development like Cleo AI. It connects to bank accounts in real time, tracks spending, predicts cash flow, and uses conversational AI to give advice that feels personal. Its value comes from automating finance tasks, providing context-aware recommendations, and alerting users before potential money problems happen.

The guide is intended for fintech entrepreneurs, startup founders, and product leaders who want to build a competitive AI-driven financial assistant. It is also useful for financial services companies exploring white-label or AI-powered advisory solutions. If you want to understand features, technical setup, compliance, or costs, it provides clear steps.

In the US, this opportunity matches industry trends. Fintech in wealth management is moving toward AI advisory tools, and AI in payments industry helps apps track accounts, cards, and digital wallets easily. Any app that wants to compete must balance technology, compliance, and user experience while moving fast.

The article shows which features to build first, how to set up your tech stack, the AI and NLP you need, realistic costs, and compliance requirements. Whether your goal is to develop an app like Cleo AI, create a Cleo AI alternative app, or launch an AI personal finance assistant app development like Cleo AI, it gives actionable steps to go from idea to launch.

Cleo is an AI-powered personal finance app that connects with user bank accounts, analyzes spending behavior, and delivers financial guidance through conversational AI. For founders, the opportunity is not simply to copy the app interface. The real challenge is building a product that combines real-time banking data, AI-driven recommendations, user engagement, and compliance into one scalable platform. This is why many startups are now investing in fintech assistant app development like Cleo AI to target users looking for smarter money management tools.

Cleo combines bank account connections, transaction tracking, conversational AI, and financial recommendations into one system. The app collects financial data, studies spending behavior, and gives users personalized responses in real time. This creates an experience that feels more interactive than a traditional banking app. Companies planning to build AI fintech app products need to understand how these components work together.

|

Core Layer |

What It Does |

Why It Matters |

|---|---|---|

|

Bank Account Integration |

Connects user accounts through banking APIs |

Helps the app track transactions in real time |

|

Data Processing Engine |

Organizes spending and analyzes cash flow |

Creates useful financial insights |

|

Conversational AI Layer |

Understands user questions and gives responses |

Makes the app feel natural and interactive |

|

Recommendation Engine |

Suggests budgets, savings goals, and spending tips |

Improves user engagement |

|

Notification System |

Sends alerts and spending updates |

Encourages users to take action |

Apps like Cleo work because every system supports the user experience. Founders exploring AI financial assistant app development like Cleo AI should focus on how data, personalization, and conversational AI connect together instead of treating AI like a separate feature.

Cleo’s growth shows that many users want financial tools that are simpler, faster, and more personal than traditional banking apps. This creates a strong opportunity for startups building AI-powered finance products.

More companies are exploring use cases of AI chatbot in banking and financial services to improve customer interaction

This demand is one reason many startups want to develop an app like Cleo AI. The opportunity also extends to banks, credit unions, and financial platforms looking to improve digital customer experiences.

Building a Cleo-style app requires more than basic mobile development. Startups need to plan for AI systems, banking integrations, compliance, security, and product scalability from the beginning. The app must also provide accurate financial recommendations while keeping user trust.

Most successful fintech startups solve one core problem first, such as budgeting, savings automation, or spending tracking. Expanding too quickly usually increases costs and product complexity.

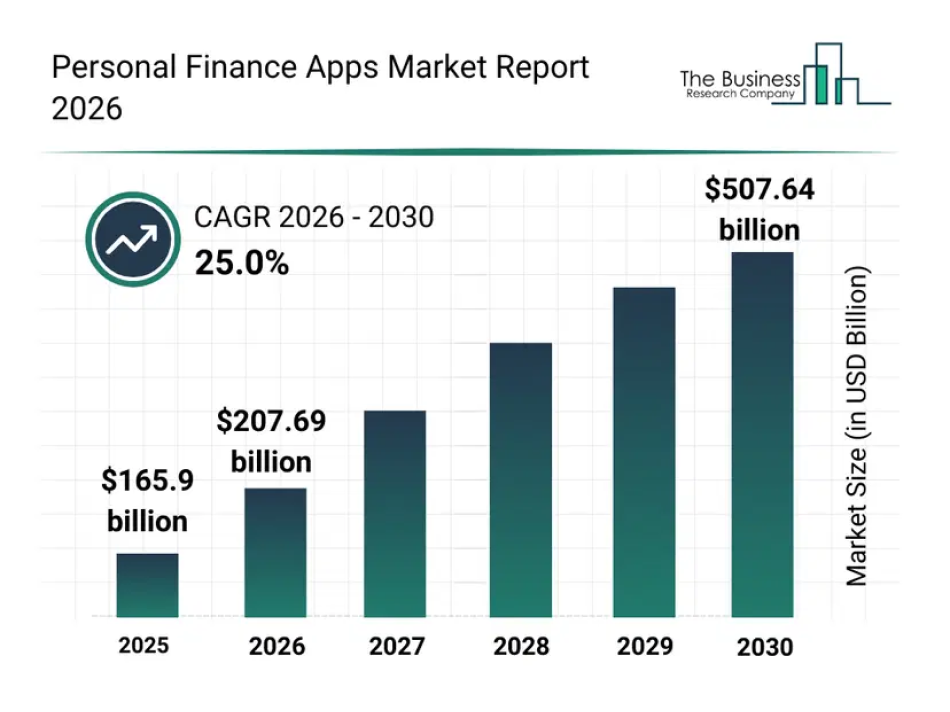

The demand for AI-powered finance apps is growing because users are rapidly adopting digital banking and AI-based financial tools. The personal finance apps market is projected to grow to more than $507 billion by 2030.

This growth is also changing user expectations. OpenAI recently introduced bank account connectivity inside ChatGPT for US users through Plaid integrations with over 12,000 financial institutions. This shows that conversational AI is moving directly into personal finance workflows, creating strong opportunities for startups investing in AI personal finance assistant app development like Cleo AI.

The US personal finance app market is expanding as more users depend on digital banking and mobile-first finance tools. Gen Z and millennials regularly use apps for budgeting, spending tracking, savings automation, and financial planning. This creates strong demand for startups looking to develop an app like Cleo AI.

The opportunity is growing beyond consumer apps. Banks, fintech companies, and credit unions are also investing in conversational finance tools to improve customer engagement and reduce support costs. Many businesses now want to integrate AI into an app to provide smarter financial experiences without building large support teams.

Another major factor is the growth of embedded finance and digital payment platforms. Apps that combine budgeting, spending insights, savings, and payments in one place usually have stronger retention. This is one reason AI financial assistant app development like Cleo AI continues to attract investment.

The biggest market opportunity comes from users who want financial tools that are easier to use and more personalized than traditional banking apps.

Most traditional finance apps focus heavily on charts and reports. Users now expect apps that explain spending behavior and provide useful financial suggestions in real time.

The AI finance app market is growing, but there are still several gaps where startups can compete successfully.

Many finance apps still depend on static dashboards. Users increasingly prefer conversational experiences that explain financial activity in simple language.

Most budgeting apps only show past spending data. Fewer apps help users predict future cash flow problems, subscription expenses, or savings opportunities.

Generic recommendations reduce engagement. Startups investing in AI model development can create more personalized financial experiences based on user behavior.

Users prefer apps that combine budgeting, savings, payments, and financial planning instead of managing multiple apps separately.

Many users still lack access to simple and easy-to-understand financial guidance, especially people with irregular income or limited financial literacy.

The market still has room for new products with focused features and better user experiences. Startups that solve specific financial problems clearly usually have a stronger chance of gaining users.

Launch fintech assistant app development like Cleo AI with smart budgeting, AI insights, and real-time banking integrations.

Talk to Our Fintech AI TeamA competitive AI finance app needs more than budgeting tools and chat support. Users now expect real-time financial insights, conversational AI, automated savings, payment features, credit monitoring, and personalized recommendations in one platform. Startups investing in building a fintech assistant app like Cleo AI with conversational AI budgeting and spending analysis features should prioritize features that improve engagement, retention, and financial decision-making.

|

Feature |

What It Does |

Why It Matters |

|---|---|---|

|

Conversational AI Interface and Human-Like Financial Guidance |

Allows users to interact with the app through natural conversations |

Makes financial management simpler and more engaging |

|

Bank Account Integration and Real-Time Transaction Sync |

Connects bank accounts and tracks transactions instantly |

Gives users accurate financial data in real time |

|

Spending Analysis Categorization and Predictive Insights |

Analyzes spending patterns and predicts future expenses |

Helps users understand and improve financial habits |

|

Personalized Budget Recommendations and Automated Savings |

Creates budgets and savings plans based on user behavior |

Improves long-term financial planning |

|

Cash Advance Salary Advance and Credit-Building Features |

Provides short-term cash access and credit improvement tools |

Supports users facing cash flow issues |

|

Proactive Alerts Behavioral Nudges and Smart Notifications |

Sends reminders, spending alerts, and financial recommendations |

Encourages better financial decisions |

|

Subscription Tracking and Recurring Payment Detection |

Detects recurring charges and unused subscriptions |

Helps users reduce unnecessary spending |

|

AI-Based Financial Goal Planning and Progress Monitoring |

Tracks savings goals and financial milestones |

Keeps users engaged with long-term planning |

|

Credit Score Tracking Risk Monitoring and Financial Health Insights |

Monitors credit activity and financial risk indicators |

Improves financial awareness and credit management |

|

Voice Assistant and Multi-Modal AI Interactions |

Supports voice commands and conversational interactions |

Creates a more accessible user experience |

|

Fraud Detection Identity Protection and Secure Authentication |

Detects suspicious activity and secures user accounts |

Builds trust and protects sensitive financial data |

|

Embedded Payments P2P Transfers and Digital Wallet Support |

Supports transfers, payments, and wallet functionality |

Expands app usability and retention |

|

Gamification Rewards and User Retention Features |

Uses rewards, streaks, and challenges to improve engagement |

Encourages consistent app usage |

|

Admin Dashboard Analytics and AI Model Management |

Gives businesses control over analytics and AI performance |

Helps optimize operations and personalization |

Many startups focus only on budgeting and chatbot features during development. Competitive products usually combine conversational AI, real-time financial insights, automation, and secure banking infrastructure into one experience. Companies planning to build AI fintech app platforms should prioritize features based on user problems instead of trying to launch every feature at once.

Portfolio Spotlight

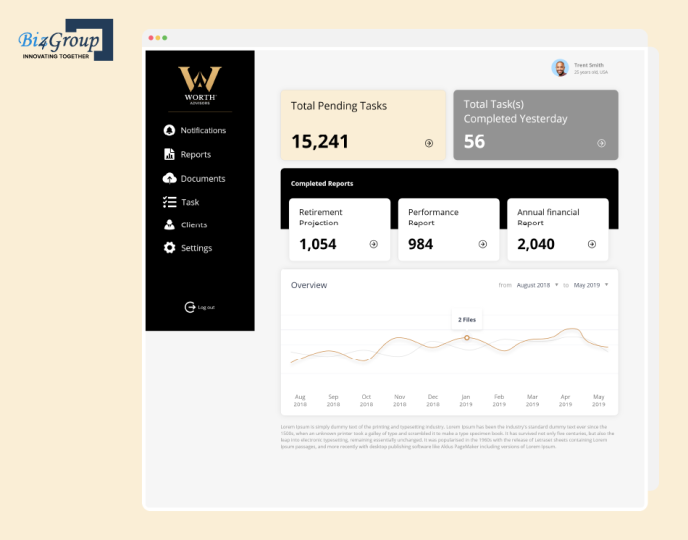

Worth Advisors is a modern financial planning platform built by Biz4Group that helps advisors streamline client onboarding, financial assessments, modular reporting, and long-term wealth planning through smart automation and data integrations. The platform reflects the growing demand for AI-driven financial guidance systems, similar to the personalized experiences users now expect from AI fintech assistant apps.

The technology stack behind an AI finance app directly affects scalability, response speed, personalization quality, and security. Startups planning AI financial assistant app development like Cleo AI need a stack that supports real-time banking data, conversational AI, predictive analytics, and fintech-grade protection without creating unnecessary infrastructure complexity.

|

Technology Layer |

Common Technologies |

Why It Matters |

|---|---|---|

|

Frontend Mobile Architecture Choices and Trade Offs |

ReactJS development, Flutter, Swift, Kotlin, NextJS development |

Impacts app performance, development speed, and cross-platform scalability |

|

Backend API Design Microservices and Data Pipelines |

NodeJS development, Express.js, GraphQL, REST APIs, Kafka |

Handles transaction processing, integrations, and scalable backend communication |

|

AI and Machine Learning Layer Models Decision Logic and Personalization |

Python development, TensorFlow, PyTorch, recommendation engines |

Powers financial predictions, personalization, and user behavior analysis |

|

NLP and Conversational AI Financial Empathy and Context Retention |

OpenAI APIs, LangChain, vector databases, conversational AI models |

Helps the app understand financial intent and maintain conversation context |

|

Data Infrastructure Real-Time versus Batch Processing |

PostgreSQL, MongoDB, Redis, Snowflake, Apache Spark |

Supports real-time transaction analysis and historical financial reporting |

|

Security Architecture Fintech-Grade Protection |

OAuth 2.0, MFA, AES encryption, tokenization, SOC 2 infrastructure |

Protects sensitive banking and financial information |

Most fintech startups use a combination of scalable backend systems, AI models, and secure cloud infrastructure instead of building everything from scratch. The right technology choices reduce long-term maintenance costs and improve scalability as user activity grows.

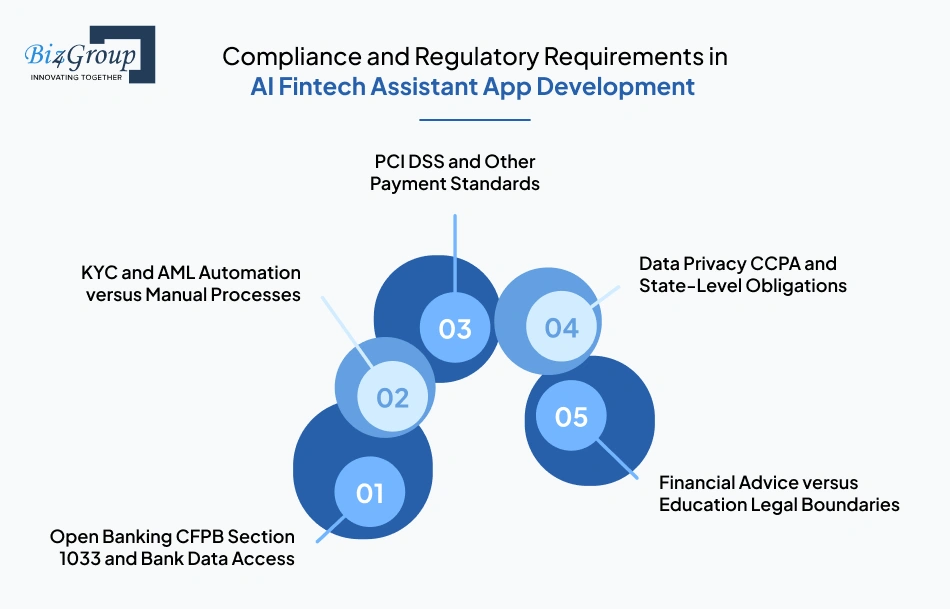

Compliance is a major part of AI financial assistant app development like Cleo AI in the US. Apps that connect to bank accounts, process payments, or analyze financial data must follow rules related to banking access, payment security, identity verification, and consumer privacy. Founders should plan compliance requirements early because fixing them later usually increases cost and delays product launches.

CFPB Section 1033 focuses on giving users secure access to their financial data. Startups using Plaid, MX, or Yodlee integrations should rely on API-based bank connections and consent-driven authentication instead of older credential-sharing methods.

Finance apps that support payments, lending, transfers, or stored balances may need to follow FinCEN rules for Know Your Customer and Anti-Money Laundering compliance. Many startups automate identity verification and fraud checks to reduce onboarding delays and operational costs. Teams that hire fintech software developers with compliance experience usually avoid expensive mistakes later.

Apps handling card payments or payment credentials must follow PCI DSS security standards. Products offering ACH payments or transfers may also require NACHA compliance and additional payment security controls. These requirements become important when apps add payment or cash advance features.

Finance apps operating in the US must comply with privacy laws such as CCPA and other state-level consumer data rules. Users should clearly understand what data is collected, how it is stored, and how consent is managed. Startups using AI integration services often build privacy controls and audit logs directly into the product architecture.

There is a legal difference between financial education and regulated financial advice in the US. Apps using conversational AI, budgeting recommendations, or investment-related insights must structure responses carefully to avoid triggering SEC or advisor licensing requirements.

Strong compliance planning reduces legal risk and makes partnerships, audits, and scaling easier later.

Develop an app like Cleo AI that delivers personalized spending insights, savings automation, and conversational finance experiences.

Start Building Your AI Finance App

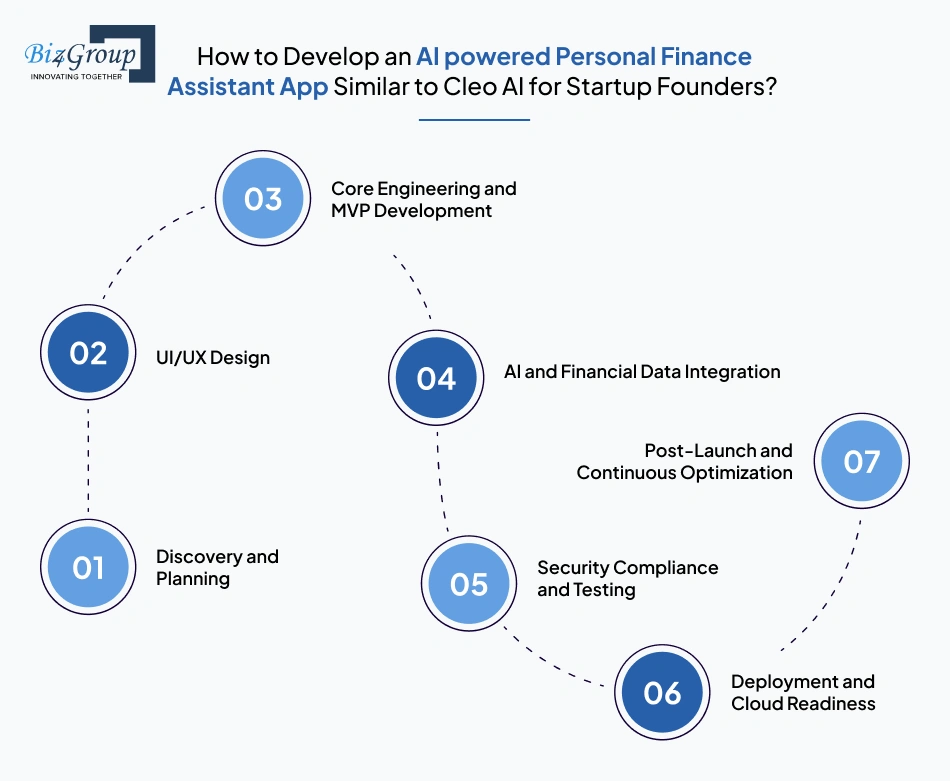

Building a fintech assistant app like Cleo AI requires balancing three things from the beginning: financial data infrastructure, conversational AI quality, and compliance. Most startups fail because they either overbuild too early or underestimate the complexity of bank integrations, AI personalization, and user trust. The roadmap below focuses on building a usable and scalable AI finance product step by step.

The first stage is defining the exact financial problem your app will solve. Cleo became successful because it focused on conversational money management instead of trying to become a full banking platform immediately. Founders should avoid building investing, lending, budgeting, and payments together in the first release.

Finance apps lose users quickly when onboarding feels complicated. Users should understand their spending, savings, and financial health within the first few minutes after connecting their accounts. Conversational AI should feel helpful instead of robotic.

Many fintech startups work with an experienced UI/UX design company because trust and usability directly impact retention in finance apps.

Also read: Top UI/UX design companies in USA

The MVP should focus on one strong financial workflow instead of launching every advanced feature at once. For most startups, the first release includes bank integrations, spending categorization, conversational insights, and basic budgeting automation.

Founders can easily reduce risk by starting with MVP development services before expanding into advanced financial products.

Also read: 12+ MVP Development Companies in USA to Launch Your Startup in 2026

The AI layer is what separates a basic budgeting app from a true financial assistant. Generic chatbot responses reduce engagement quickly. The app should understand transaction patterns, user intent, recurring expenses, and financial behavior over time.

Security issues damage trust faster in fintech than in almost any other industry. Apps handling financial data must secure bank credentials, transaction history, payment information, and user identity from the start.

Also Read: 15+ Software Testing Companies in USA in 2026

AI finance apps often experience traffic spikes after launches, referral campaigns, or salary periods. Infrastructure should scale automatically without slowing down transaction processing or AI responses.

Launching the app is only the beginning. Financial behavior changes constantly, which means AI recommendations and product workflows also need continuous improvement.

The strongest AI finance apps usually scale by solving one financial problem exceptionally well before expanding into broader banking or wealth management services.

Build a fintech assistant app like Cleo AI that improves engagement through personalized recommendations and behavioral insights.

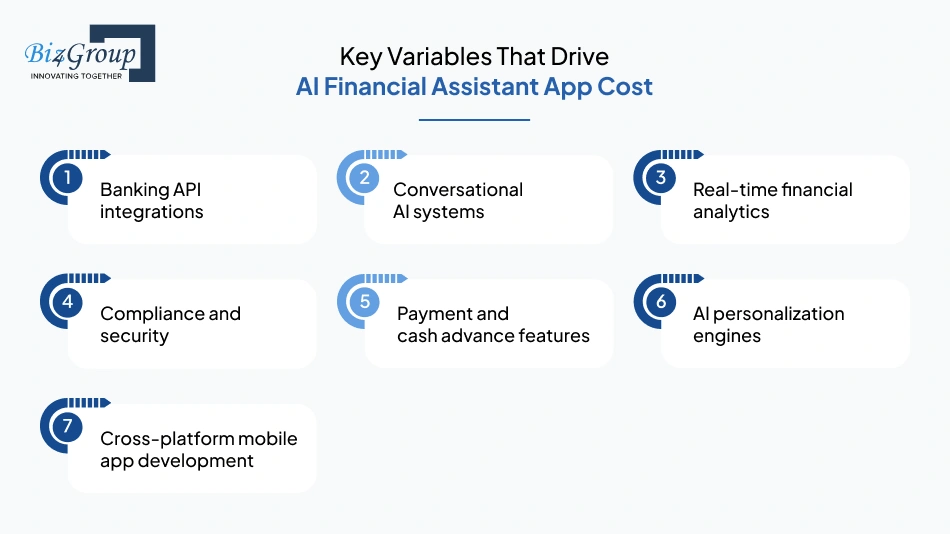

Explore AI Fintech DevelopmentThe cost of building a fintech assistant app like Cleo AI can range anywhere between $30,000 and $250,000+, depending on feature complexity, AI capabilities, compliance requirements, banking integrations, and development approach. These numbers are ballpark estimates, not fixed pricing. Startups planning AI financial assistant app development like Cleo AI should budget separately for MVP development, infrastructure scaling, compliance, and post-launch optimization.

Some features increase development costs much faster than others. Conversational AI, financial data infrastructure, and compliance systems usually consume a large part of the budget early.

|

Cost Driver |

Why It Increases Budget |

|---|---|

|

Banking API integrations |

Requires secure connections, testing, and transaction syncing |

|

Conversational AI systems |

Needs NLP pipelines, context retention, and AI training |

|

Real-time financial analytics |

Requires scalable backend infrastructure and data pipelines |

|

Compliance and security |

Includes PCI DSS, fraud prevention, MFA, and encryption |

|

Payment and cash advance features |

Adds regulatory complexity and payment infrastructure |

|

AI personalization engines |

Increases AI model training and optimization costs |

|

Requires frontend optimization for Android and iOS |

Teams investing heavily in AI model development and advanced personalization usually face higher infrastructure and maintenance costs compared to basic budgeting apps.

The development cost depends heavily on how advanced the product is at launch. A simple MVP focused on budgeting and conversational insights costs far less than an enterprise-grade platform supporting payments, lending, fraud monitoring, and large-scale AI personalization. The figures below are ballpark estimates and not fixed pricing.

|

Product Level |

Ballpark Cost Range |

Typical Features |

|---|---|---|

|

MVP AI Financial Assistant App |

$30,000–$80,000 |

Bank integrations, spending tracking, budgeting, basic conversational AI, notifications |

|

Advanced AI Finance App |

$80,000–$180,000 |

Personalized recommendations, automated savings, subscription tracking, predictive insights, credit monitoring |

|

Enterprise-Grade AI Financial Platform |

$180,000–$250,000+ |

Payment systems, cash advances, fraud detection, advanced AI personalization, compliance infrastructure, admin dashboards |

Most startups begin with a focused MVP to validate user engagement before expanding into advanced financial services. Products with custom AI systems, payment infrastructure, or enterprise banking integrations usually see much higher long-term operational and infrastructure costs.

Yes, $500K is usually enough to launch a competitive MVP if the scope stays focused. The problem is that many founders try to build budgeting, lending, investing, payments, and AI automation together in the first release.

A realistic MVP budget for a Cleo-style finance app usually covers:

A $500K budget becomes difficult when founders add advanced lending systems, custom AI infrastructure, or large-scale payment functionality too early. This is where overall AI fintech app development cost increases rapidly.

Most fintech founders plan for development costs but overlook operational and infrastructure expenses that appear after launch.

The most successful fintech startups usually control costs by limiting the MVP scope and expanding features only after validating user demand.

AI financial assistant app development like Cleo AI works best when features, compliance, and scalability are planned from day one.

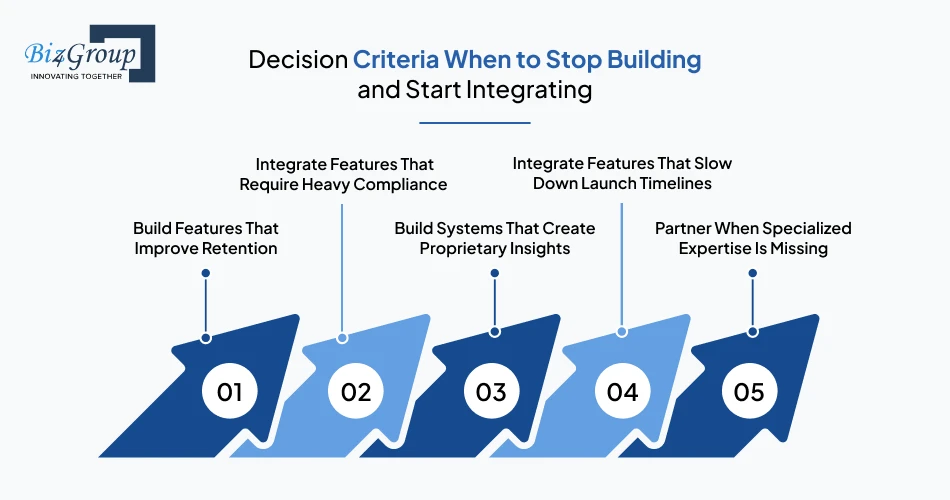

Schedule a Strategy CallStartups building AI financial assistant apps like Cleo AI do not need to build every system internally. Some features should be custom-built because they improve user engagement and product differentiation. Others are faster, cheaper, and safer to integrate through third-party providers. The right decision usually depends on budget, launch timeline, compliance complexity, and internal technical expertise.

Some systems directly affect how users experience the product. These features usually create the biggest competitive advantage when built internally.

|

Feature |

Why It Should Be Custom |

|---|---|

|

Conversational AI experience |

Shapes how users interact with the app daily |

|

Financial recommendation engine |

Improves personalization and budgeting accuracy |

|

Spending behavior analytics |

Helps predict user habits and financial risks |

|

Gamification and reward systems |

Increases retention and engagement |

|

AI-powered onboarding flows |

Improves account setup completion rates |

Startups investing in conversational finance platforms often build these systems internally because they directly affect retention and long-term growth. This becomes even more important for founders thinking about how to monetize AI app products through subscriptions or premium financial insights.

Some fintech infrastructure already exists through trusted providers, making integration a better option than custom development.

Startups building a fintech assistant app like Cleo AI use third-party providers for compliance-heavy infrastructure while focusing internal development on personalization and user experience.

A simple way to make build-versus-buy decisions is to ask whether the feature creates product differentiation or simply supports operations.

Conversational AI, financial insights, and personalization directly affect engagement and should usually remain internal products.

Payments, KYC, fraud monitoring, and banking infrastructure are often easier and safer to integrate through existing providers.

Custom analytics and recommendation engines can improve prediction quality and strengthen long-term product value.

Using third-party APIs can help startups launch faster and validate demand before expanding infrastructure.

Some startups work with an experienced AI chatbot development company instead of trying to hire AI developers for every advanced AI or fintech system internally.

Most successful fintech startups build the user-facing experience internally and integrate the infrastructure that already exists reliably in the market.

Most AI finance apps do not rely on one revenue stream. Products like Cleo usually combine subscriptions, embedded finance features, affiliate partnerships, and B2B licensing to increase long-term revenue. Startups planning AI financial assistant app development like Cleo AI should choose monetization models that match user behavior and feature usage.

Most finance apps use a free plan to attract users and a paid subscription to unlock advanced features. Free users usually get budgeting tools, spending tracking, and basic financial insights. Paid users get features like savings automation, cash advances, or personalized recommendations.

Cash advance and embedded finance features can increase revenue, but they also increase compliance and operational costs. Startups need to manage repayment risk, payment processing fees, and fraud prevention carefully before adding these features.

Finance apps can also earn revenue by recommending financial products like savings accounts, credit cards, insurance, or investment tools. These partnerships work better when recommendations are based on actual user spending behavior.

Many banks and credit unions want AI-powered budgeting and conversational finance tools but do not want to build them internally. White-label licensing allows fintech startups to provide these tools as ready-made platforms.

|

Monetization Model |

Primary Revenue Source |

Best Fit For |

|---|---|---|

|

Freemium + Subscription |

Monthly or yearly subscriptions |

Consumer-focused budgeting and savings apps |

|

Cash Advance and Embedded Finance |

Transfer fees, subscriptions, lending fees |

Apps targeting users with short-term cash flow needs |

|

Affiliate Partnerships |

Referral commissions from financial products |

Apps with high user engagement and spending insights |

|

B2B White-Label Licensing |

SaaS licensing and enterprise contracts |

Startups selling fintech solutions to banks and credit unions |

The strongest fintech products usually combine consumer subscriptions with additional revenue streams like partnerships or B2B licensing. This reduces dependence on a single monetization model.

From banking APIs to conversational AI, build an AI money management app like Cleo AI with secure and scalable architecture.

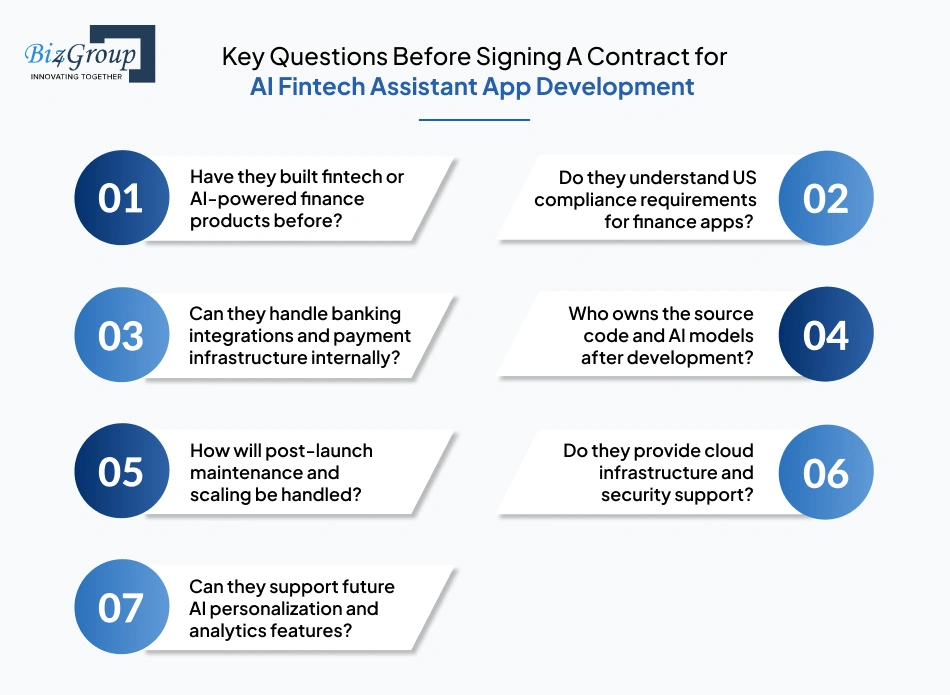

Connect With Our AI ExpertsThe success of an AI finance app depends heavily on the development partner behind it. Building a fintech assistant app like Cleo AI requires expertise in banking APIs, conversational AI, compliance, cloud infrastructure, and financial data security. A team without fintech experience can increase development delays, compliance risks, and long-term maintenance costs.

Many app development companies can build mobile applications, but fintech products require much deeper technical and regulatory expertise. Startups should evaluate whether an agency understands banking infrastructure, AI personalization, compliance, and financial data protection before signing a contract.

|

Evaluation Area |

Fintech-Experienced Agency |

Generic App Shop |

|---|---|---|

|

Banking API integrations |

Experienced with Plaid, MX, Yodlee, ACH systems |

Limited fintech integration experience |

|

Compliance knowledge |

Understands PCI DSS, KYC, AML, CCPA |

Often depends on external consultants |

|

Conversational AI expertise |

Builds finance-focused AI systems |

General chatbot development only |

|

Security architecture |

Designs fintech-grade security systems |

Basic mobile app security practices |

|

Scalability planning |

Builds infrastructure for transaction-heavy apps |

Focuses mainly on frontend delivery |

Many startups prefer working with specialized fintech teams instead of general app agencies because AI finance products require long-term infrastructure planning and compliance awareness from the beginning.

Before selecting a development partner, founders should evaluate both technical capability and long-term product support.

Majority of the founders focus only on initial development costs and ignore post-launch scalability, security, and compliance support during vendor evaluation.

US fintech products operate in a highly regulated environment. Teams building AI personal finance assistant app development like Cleo AI products need experience with US banking systems, consumer privacy laws, payment regulations, and financial compliance requirements.

Biz4Group LLC, a reliable AI development company in USA, is a strong choice for startups and enterprises building AI finance platforms because of its experience in fintech development, AI-driven applications, cloud infrastructure, and scalable enterprise systems. The company also works on advanced solutions involving AI agent implementation, conversational AI, wealth management software solutions, and secure fintech architecture for US-based businesses.

Choosing the right partner early can reduce development risks, improve launch speed, and make future scaling much easier.

AI finance apps are moving beyond budgeting and spending analysis. The next phase of the market will focus on autonomous financial actions, deeper personalization, and AI systems that continuously adapt to user behavior. Startups building AI personal finance assistant app development like Cleo AI products should prepare for these shifts early because they will shape user expectations over the next few years.

Future AI finance apps will move from giving recommendations to taking approved actions automatically. Instead of only suggesting savings transfers or bill payments, AI agents will execute them based on user-defined rules and financial goals. This shift is increasing demand for AI automation services in fintech.

Future finance apps will rely less on generic budgeting advice and more on AI systems trained on individual spending patterns, income cycles, and financial goals. Personalization quality will become a major competitive advantage.

Many finance apps still separate budgeting, payments, savings, and investing into different systems. Future platforms will combine these services into unified AI-driven financial ecosystems managed through one interface.

AI financial assistants will increasingly work across phones, smart speakers, wearables, and workplace platforms while maintaining financial context across devices.

As AI finance apps become more autonomous, regulators will expect companies to explain how AI recommendations and decisions are generated. Future systems will need transparent AI decision tracking and stronger compliance monitoring.

Payments, lending, insurance, and savings features will increasingly operate in the background instead of requiring separate apps or manual workflows.

More AI finance apps are expected to integrate directly with payroll systems for earned wage access, automated savings, tax forecasting, and income-based budgeting.

Future platforms may use multiple AI agents for budgeting, fraud monitoring, subscription management, debt optimization, and investment tracking instead of relying on one generalized assistant.

Traditional credit scoring models may gradually expand into AI-generated financial wellness scoring based on spending stability, savings behavior, and cash flow patterns.

Banks and financial institutions are increasingly adopting AI-powered customer engagement and automation systems. This is one reason many enterprises now work with top AI development companies in Florida to modernize digital financial experiences.

The next generation of AI finance apps will focus more on autonomous financial assistance, real-time decision-making, and highly personalized financial experiences.

Building a fintech assistant app like Cleo AI is not really about adding AI to a finance app anymore. That part is expected now.

The real challenge is building a product people trust enough to connect their bank accounts to, open daily, and rely on when making money decisions. That takes much more than a chatbot and spending charts. You need accurate transaction analysis, useful recommendations, fast onboarding, reliable bank integrations, strong security, and AI systems that actually improve the user experience instead of slowing it down.

A lot of founders make the mistake of trying to build budgeting, lending, investing, payroll, rewards, and embedded finance features all at once. In reality, the strongest fintech products usually start small, solve one problem really well, and expand after user behavior validates the direction.

That is why the technical decisions matter early. The wrong banking infrastructure, weak AI workflows, poor retention design, or delayed compliance planning can become expensive problems later. Building AI software for fintech products requires balancing scalability, compliance, personalization, and speed to market at the same time.

For startups entering this space, execution quality matters far more than feature quantity.

Working with an experienced custom software development company can also help reduce expensive rebuilds later, especially when the product starts scaling beyond the MVP stage.

Because fixing fintech infrastructure after launch usually costs a lot more than building it properly the first time.

Planning to build an AI fintech app? Let’s discuss your roadmap, budget, feature priorities, and launch strategy.

A basic MVP with budgeting, bank integrations, transaction tracking, and conversational AI usually takes around 4 to 6 weeks. More advanced platforms with lending, embedded finance, payroll integrations, or AI personalization engines can take 8+ months depending on complexity and compliance requirements.

The development cost can range between $30,000 and $250,000+ depending on the product scope, AI capabilities, banking integrations, security requirements, and development approach. These are ballpark estimates, not fixed pricing. MVPs cost significantly less than enterprise-grade fintech platforms.

It depends on the features your app offers. Budgeting and financial education apps usually face fewer licensing requirements, while apps handling payments, lending, salary advances, or money transfers may require additional compliance, partnerships, or financial licenses in certain states.

Most fintech startups use providers like Plaid, MX, or Yodlee for bank account aggregation and transaction syncing. The right provider usually depends on pricing, bank coverage, data quality, and long-term scalability requirements.

Yes. Many finance apps still rely heavily on rule-based systems, predictive analytics, and transaction categorization engines instead of fully generative AI systems. Generative AI mainly improves conversational experiences, personalization, and natural language interactions.

For most startups, the hardest part is balancing real-time financial data processing, AI personalization, compliance, and scalability together. Building reliable bank integrations and maintaining user trust usually becomes more difficult than frontend app development itself.

with Biz4Group today!

Our website require some cookies to function properly. Read our privacy policy to know more.