info@biz4group.com

info@biz4group.com

Imagine a digital system that doesn’t wait for instructions but instead, understands your business goals, learns from real-time feedback, and takes independent actions to get the job done.

Read More

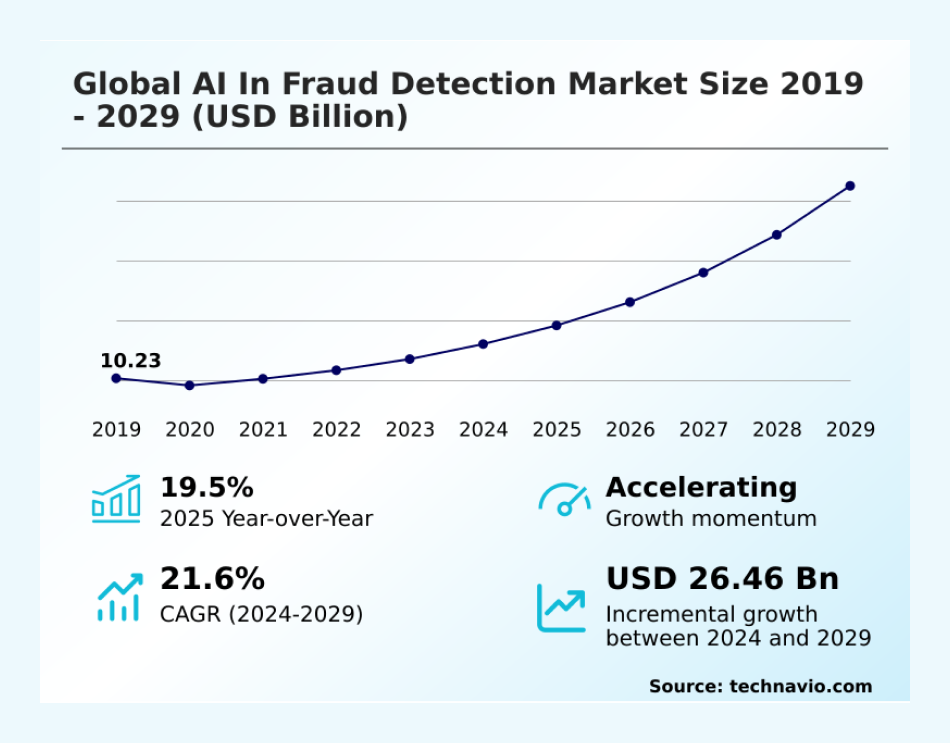

Every dollar lost to fraud is a dollar taken from growth, trust, and future opportunities. In today’s digital era, payment fraud isn’t a distant threat, it’s happening right now and growing fast.

Here’s the reality most leaders don’t talk about:

Growth like this is not abstract. More digital transactions create more opportunities for fraud, making AI fraud detection solutions for banks, fintech, and e-commerce platforms a critical requirement as payment volumes and attack surfaces expand.

Fraud today is fast, adaptive, and automated, making it difficult for traditional rule-based systems simply to keep up. This is where AI payment fraud detection software development moves from nice to have to must have integration in the financial ecosystems.

These systems rely on continuous AI model development to build AI transaction fraud detection tool that identify suspicious activity in milliseconds, protect revenue, and maintain customer confidence without slowing legitimate transactions.

In this guide, we’ll walk you through:

Ready to reduce fraud losses and strengthen trust? Let’s dive in.

AI payment fraud detection software focuses on protecting transactions as they move across complex digital payment environments. These systems sit directly within payment flows and assess risk the moment a transaction is initiated. They decide whether a payment should proceed, pause, or stop.

In modern ecosystems, fraud detection must work across cards, wallets, BNPL, and cross-border payments without adding friction. That requirement shapes how businesses develop AI payment fraud detection system today.

At a functional level, these solutions are designed to:

Unlike legacy tools, modern fraud detection software adapts as payment behavior changes. It becomes part of the payment infrastructure itself, not an external control layer.

AI payment fraud detection software development is built to function inside live payment flows, not after transactions settle. The goal is to evaluate risk instantly while customers complete payments without disruption.

In real-time environments, teams develop real time AI fraud detection software that follows a tightly coordinated process:

This flow runs continuously across gateways, processors, and settlement layers. It relies on automated decision paths supported by AI automation services that help systems respond at scale without manual intervention.

The advantage lies in timing. Acting before a transaction completes reduces fraud exposure while preserving a smooth payment experience. That balance defines effective real-time fraud detection in modern payment ecosystems.

Watch real-time detection simplify payment risk. You've seen the system. Now let payment experts fine-tune it.

Build with Biz4Group

AI payment fraud detection software development exists because modern payment systems expose risks that traditional controls cannot manage effectively. As payment volumes increase and channels multiply, fraud becomes harder to predict, detect, and stop in time.

Banks, fintech platforms, and e-commerce businesses process payments across multiple rails. Cards, wallets, BNPL, and cross-border flows all behave differently. Fraud signals scatter across systems, reducing visibility during live transactions.

Payments are expected to be completed instantly, and fraud checks must happen in milliseconds. Delays increase abandonment, while late decisions result in financial loss. Maintaining accuracy without slowing transactions remains a constant challenge.

Fraud tactics change faster than static rules can adapt as what looks safe today may become risky tomorrow. Teams struggle to keep detection logic aligned with changing transaction behavior.

As fraud volume rises, manual reviews grow quickly. This slows response times and increases operational costs. It also limits scalability during traffic spikes and peak payment periods.

The challenge is not identifying fraud after settlement. It is detecting risk early enough to protect revenue while preserving a seamless payment experience.

Also Read: How AI in Payments is Changing the Digital Payments Landscape?

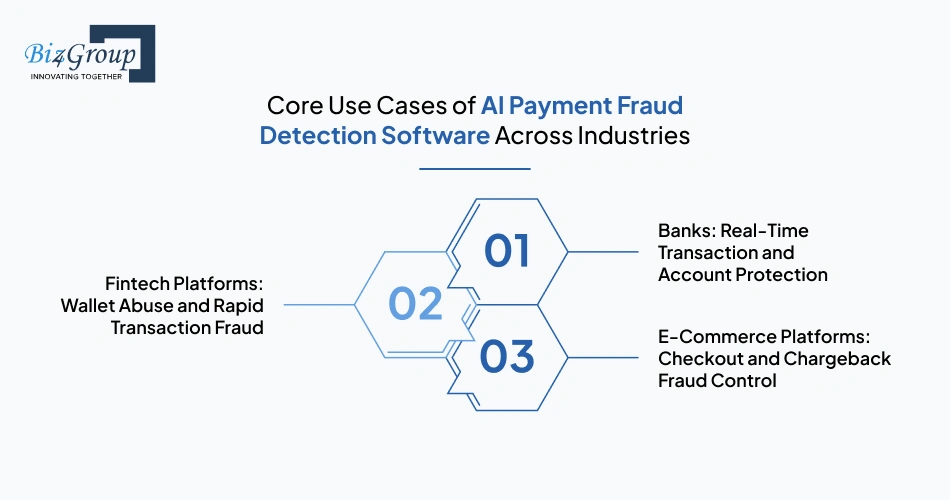

AI payment fraud detection software development shows its real value when applied to industry-specific payment risks. Each sector faces different fraud patterns, transaction speeds, and customer expectations. These use cases reflect how detection systems operate inside real payment environments.

Banks process high volumes of cards and digital transactions every second. Fraud detection must act before authorization is complete. Common use cases include:

Many institutions build AI powered fraud detection systems for banks and fintech to reduce false declines while maintaining regulatory confidence.

Also Read: How to Build AI Banking App: Steps, Cost and Challenges

AI in fintech platforms handle fast onboarding and high-velocity payments. Fraud often appears as sudden spikes rather than slow patterns. Key use cases include:

Clear fraud workflows are often shaped with support from AI consulting services before scaling across payment flows.

Also Read: How to Build an AI Fintech App: From MVP to Market-Ready

E-commerce fraud appears mainly during checkout and post-purchase disputes. Trained AI models help in:

Across industries, these use cases show one clear priority. Detect payment risk early, act before funds move, and protect revenue while keeping legitimate transactions smooth and uninterrupted across every payment channel.

This section reviews leading platforms used for AI payment fraud detection in real payment environments. It helps teams understand how existing solutions handle transaction risk and where custom development may be required.

Feedzai focuses on real-time payment risk management for banks and large payment processors. The platform supports complex transaction environments where speed, accuracy, and regulatory alignment matter every second.

Featurespace is known for detecting unusual payment behavior using adaptive risk models. It fits organizations that manage high transaction volumes across multiple payment channels.

Kount focuses on protecting digital commerce and payment flows from fraud abuse. It is commonly used by merchants balancing fraud prevention with smooth checkout experiences.

SEON is widely used by fast-growing fintechs and online platforms. It emphasizes flexible fraud controls that adapt quickly to new attack patterns.

NICE Actimize is designed for regulated financial institutions managing complex fraud and compliance demands. It supports large-scale monitoring across payments, accounts, and financial activity.

These platforms show how AI fraud detection solutions for banks, fintech, and e-commerce platforms operate in real environments. They also highlight why many organizations choose custom AI payment fraud detection development when off-the-shelf tools cannot fully match their payment flows, risk models, or growth plans.

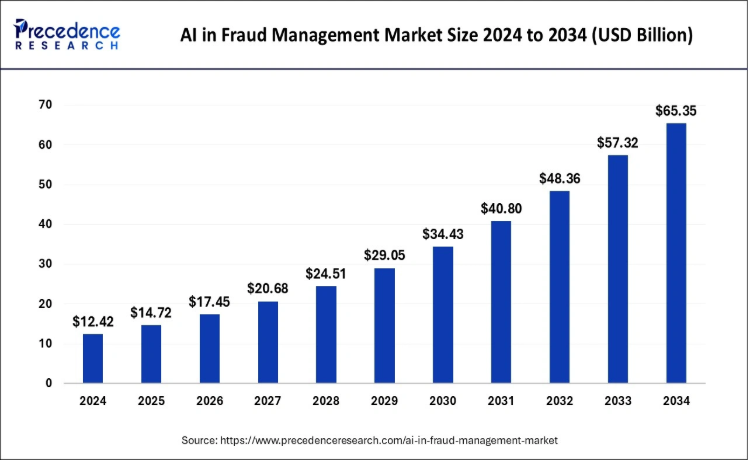

Businesses investing in AI-driven payment fraud detection software are prioritizing revenue protection, scalability, and risk control. As digital transactions accelerate, investors increasingly view AI-led fraud prevention as a core infrastructure decision rather than an operational upgrade.

To understand the opportunity driving the shift, let’s look at the market dynamics that make investing in AI fraud prevention a strategic decision for growth.

For investors, this trajectory signals a clear opportunity to back scalable fraud infrastructure with long-term demand and compounding returns.

Though market growth creates opportunity for the businesses to invest but that opportunity becomes clearer when you look at how AI fraud payments handling works at scale:

| What Happens in Day-to-Day Fraud Handling | What Investing in AI Changes for the Business |

|---|---|

|

Fraud rules must be manually updated as patterns change |

New fraud patterns are identified automatically without constant rule changes |

|

Legitimate transactions are frequently flagged and blocked |

More genuine payments go through, improving approval rates and revenue |

|

Fraud teams review transactions one by one |

Most transactions are cleared instantly, reducing review workload |

|

Staffing grows as transaction volume increases |

Fraud operations scale without adding headcount |

|

Fraud insights are scattered across tools |

Centralized visibility helps teams act on recurring fraud trends |

|

Decisions vary by channel or region |

Fraud decisions stay consistent across all payment channels |

When done right, AI in payment fraud management supports growth instead of adding cost as transaction volumes increase.

Investing in AI payment fraud detection software creates value where businesses feel it most revenue protection, cost control, and scalable growth. The impact appears quickly in daily payment performance and compounds as transaction volumes increase.

Key business outcomes include:

As payment ecosystems mature, delaying fraud modernization quietly creates inefficiencies that are hard to undo later. Investing in payment fraud prevention software development with AI helps businesses scale securely, protect margins, and stay aligned with how transaction volumes continue to grow.

As businesses move from manual checks to intelligent fraud control, feature selection becomes critical. AI payment fraud detection software development is not about packing dashboards or adding generic automation. It’s about building capabilities that can protect transactions, scale decisions, and adapt as fraud patterns evolve.

| Feature | Why This Feature Is Non-Negotiable |

|---|---|

|

Real-Time Transaction Risk Scoring |

Blocks fraudulent payments instantly without adding latency to legitimate transactions |

|

User and Transaction Behavior Baselines |

Flags deviations in spending, device, and location patterns tied to genuine payment behavior |

|

Continuous Fraud Payment Pattern Updating |

Incorporates new fraud signals without manual rule rewrites or system downtime |

|

False Decline Control Mechanisms |

Protects approval rates by preventing legitimate payments from being incorrectly blocked |

|

Cross-Channel Fraud Payment Consistency |

Applies the same risk logic across web, mobile, POS, and international payments |

|

Pre-Chargeback Fraud Payment Detection |

Identifies high-risk transactions before disputes occur, reducing financial penalties |

|

Operational Fraud Payment Visibility |

Gives teams clear insight into alerts, decisions, and recurring fraud trends |

|

Decision Traceability and Audit Logs |

Supports compliance reviews and internal audits with explainable decision records |

These features rely on consistent data flow across payment and risk systems, supported through structured AI integration services. Together, they define the baseline required for AI-driven payment fraud detection platforms to deliver reliable decisions under real transaction conditions.

Replace manual fraud checks with real-time detection that protects revenue and approvals.

Talk to UsAdvanced capabilities define how effectively AI payment fraud detection software operates inside live transaction environments. These capabilities are deliberately planned during AI payment fraud detection software development to handle speed, scale, and adaptive fraud behavior without disrupting genuine payments.

They reflect the same production-grade principles used when teams build AI software designed to operate continuously under high transaction pressure.

| Advanced AI Capability | Practical Differentiation in Live Payments |

|---|---|

|

Real-Time Behavioral Context Scoring |

Evaluates each transaction using user-specific spending behavior rather than static transaction rules. |

|

Adaptive AI Model Learning Without Redeployment |

Updates fraud intelligence continuously without stopping payment flows or redeploying production systems. |

|

Cross-Transaction Pattern Correlation |

Detects coordinated fraud payments by analyzing relationships across users, devices, and payment instruments simultaneously. |

|

Channel-Agnostic Risk Intelligence |

Applies unified fraud logic across cards, wallets, BNPL, and cross-border payment transactions. |

|

Precision False-Decline Suppression Logic |

Allows trusted behavioral signals to override risk flags and protect legitimate transaction approvals. |

|

Transaction-Level Decision Explainability |

Records clear decision reasoning to support audits without slowing real-time payment authorization. |

|

Embedded Fraud Outcome Feedback Loops |

Use chargebacks and confirmations to improve detection accuracy during everyday payment operations. |

|

Scalable AI Model Governance Controls |

Enables controlled testing, monitoring, and rollout of detection logic across growing transaction volumes. |

These capabilities move fraud detection beyond reactive controls. They allow teams to develop AI payment fraud detection software for secure transactions that remain accurate as fraud tactics evolve, payment channels expand, and transaction speed expectations increase.

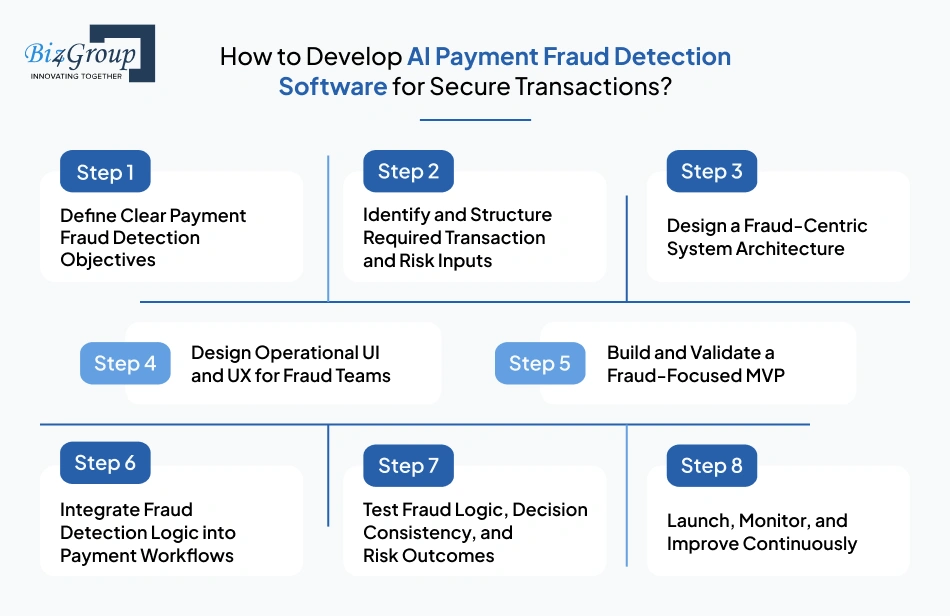

Developing AI payment fraud detection software requires a structured approach that prioritizes real-time risk decisions, consistent fraud controls across payment channels, and long-term reliability as transaction volumes scale within live payment environments.

The following steps outline how teams should approach development, from defining fraud objectives to deploying a detection system that operates reliably inside live payment workflows.

Start by defining what type of payment fraud the system must prevent and where decisions need to happen within transaction flows.

This step ensures the fraud detection system is designed around real payment risk outcomes, not abstract threat models.

AI payment fraud detection software depends on structured inputs across transactions, users, devices, and payment instruments.

Without structured and reliable inputs, fraud decisions become inconsistent and difficult to scale.

The system architecture must support real-time fraud decisions while allowing detection logic to evolve safely.

This stage ensures the fraud detection system remains stable as transaction volumes and fraud complexity increase.

Fraud detection software must support operational clarity without slowing response times inside live payment environments. Effective UI and UX design translate complex risk evaluation into operational views that fraud teams can act confidently during high-volume transaction periods.

Key design considerations include:

Partnering with a skilled UI and UX design company ensures fraud teams focus on decisions, not navigation. This helps in improving response speed and maintaining accuracy as transaction volumes and fraud pressure increase.

Also Read: Top 15 UI/UX Design Companies in USA

An MVP helps confirm whether a fraud detection system identifies real payment risk without disrupting legitimate transactions. In AI payment fraud detection, MVP software development focuses on validating decisions early under controlled conditions.

Key MVP validation activities include:

This approach aligns with how teams use MVP development services to validate detection accuracy early and reduce downstream risk.

Also Read: Top 12+ MVP Development Companies

Fraud detection logic must be embedded directly into payment authorization and settlement flows.

Reliable integration ensures fraud decisions happen before funds move, without disrupting legitimate payments.

Before the launch, the system must be tested as a fraud detection platform, not just as software. The goal is to verify that risk decisions remain consistent across channels, regions, and transaction types.

This step ensures the system produces reliable fraud decisions under real payment conditions, not just technically correct outputs.

Also Read: Software Testing Companies in USA

After the launch, the fraud detection system must evolve as fraud tactics and payment behavior change.

Many teams work with a custom software development company at this stage to support continuous refinement and ensure the system remains reliable as payment volumes and fraud complexity grow.

Following this structured approach helps teams build AI transaction fraud detection tool that integrate directly into payment workflows, deliver consistent risk decisions, and remain reliable as transaction volumes and fraud patterns grow.

You've seen how fraud detection works in real payment environments. Now build it right.

Get in TouchIn AI payment fraud detection software development, selecting the right technology stack comes early in the build process and shapes how fraud detection components interact, process transactions, and support real-time risk decisions within live payment workflows.

| Architecture Layer | Technology Used | Purpose |

|---|---|---|

|

Fraud Operations Frontend |

React / Angular |

Builds internal fraud dashboards through ReactJS development, enabling alert reviews, investigations, overrides, and audit visibility for risk teams. |

|

Backend Service Layer |

Node.js / Java Microservices |

Handles NodeJS development for orchestrating transaction flows, coordinating fraud logic, and managing system interactions at scale. |

|

Transaction Ingestion Layer |

Apache Kafka / AWS Kinesis |

Captures live transactions, device, and behavioral signals using streaming pipelines required for real-time fraud evaluation. |

|

Real-Time Processing Layer |

Apache Flink / Spark Streaming |

Processes transaction events and executes fraud logic before payment authorization completes. |

|

Feature Engineering Layer |

Python / Redis |

Uses Python development to transform raw transaction data into behavioral and risk features during live scoring. |

|

Fraud Detection Engine |

Java |

Executes transaction-level risk scoring and fraud decision logic under strict latency constraints. |

|

AI Model Framework |

TensorFlow / PyTorch |

Trains and serves fraud detection models used for behavioral and pattern-based risk evaluation. |

|

Decision Orchestration Layer |

REST APIs / Microservices |

Supports API development to approve, challenge, or block decisions consistently across payment channels. |

|

Data Storage Layer |

PostgreSQL / BigQuery |

Stores transaction history, fraud outcomes, and audit-ready decision records securely. |

|

Model Management Layer |

MLflow / Kubeflow |

Manages model versions, performance monitoring, and controlled rollout of fraud logic in production. |

|

Security and Compliance Layer |

Encryption / Tokenization |

Protects sensitive payment data and supports regulatory and internal audit requirements. |

A carefully selected stack like this enables teams to create AI driven payment fraud monitoring system that deliver consistent real-time risk decisions, maintain compliance readiness, and remain reliable as transaction volumes and fraud patterns continue to evolve.

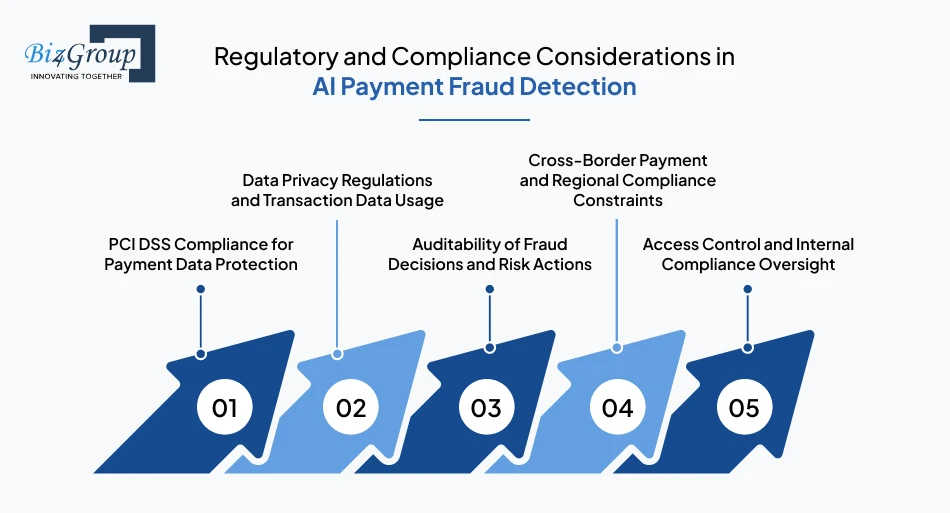

AI payment fraud detection systems operate within regulated financial environments where transaction decisions, data usage, and system access are closely governed. Compliance requirements directly influence how fraud detection systems are designed, deployed, and audited across payment ecosystems.

Below are the core regulatory considerations that shape compliant and defensible AI payment fraud detection systems.

Fraud detection platforms process card and transaction data subject to PCI DSS requirements. This governs how payment information is stored, transmitted, and accessed across eCommerce payment environments.

Failure to meet PCI DSS standards can result in penalties and loss of payment processing privileges.

Payment fraud detection uses transaction and behavioral data that qualifies as personal information, requiring privacy controls defined for implementing an eCommerce solution.

Privacy compliance ensures fraud prevention does not introduce secondary regulatory exposure.

Payment networks, regulators, and acquiring banks require fraud decisions to be reviewable after execution.

Auditability is required to defend fraud decisions during disputes, investigations, and compliance audits.

Fraud detection systems supporting international payments must comply with regional regulatory requirements.

Cross-border compliance failures can result in transaction restrictions or regulatory penalties.

Regulators require controlled access to fraud detection systems handling sensitive payment data.

Access to governance is a mandatory compliance requirement in regulated financial systems.

Regulatory compliance in payment fraud detection is not a parallel effort. It defines how fraud systems operate safely, transparently, and consistently. This shapes the organization’s approach to AI payment fraud detection software development services within regulated payment environments.

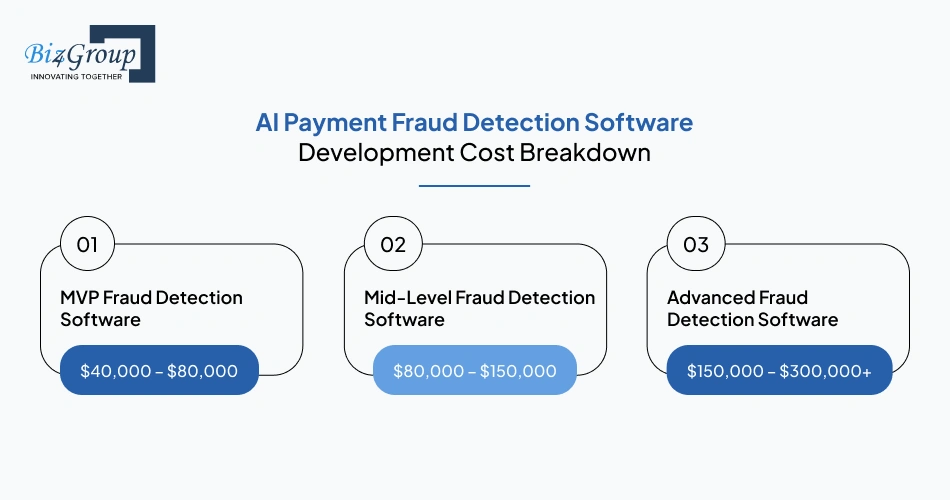

In AI Payment Fraud Detection Software Development, cost is driven by how much real-time risk responsibility the system carries inside live payment flows. In practice, an AI payment fraud detection software development cost estimate typically ranges from $40,000 to $300,000+, depending on detection depth, transaction volume, and scalability requirements.

| Types | Estimated Cost Range | What This Typically Covers |

|---|---|---|

|

MVP Fraud Detection Software |

$40,000 – $80,000 |

Real-time transaction checks, basic risk scoring, limited behavioral analysis, and single-channel payment coverage. |

|

Mid-Level Fraud Detection Software |

$80,000 – $150,000 |

Multi-channel monitoring, stronger behavior profiling, false-decline control, analyst dashboards, and scalable processing. |

|

Advanced Fraud Detection Software |

$150,000 – $300,000+ |

High-volume real-time detection, cross-transaction analysis, audit-ready decision logs, and global payment scalability. |

The cost to develop AI payment fraud detection software increases as the system moves from basic transaction checks to enforcing confident real-time risk decisions across complex payment ecosystems.

The most effective approach is to start with core fraud detection workflows, validate risk accuracy in live payment conditions, and expand intelligence only where it reduces losses or operational friction. Cost should always reflect how much financial risk the system is trusted to manage.

Also Read: AI Software Development Cost

Align fraud detection costs with real transaction risk and growth expectations.

Get a Custom Quote

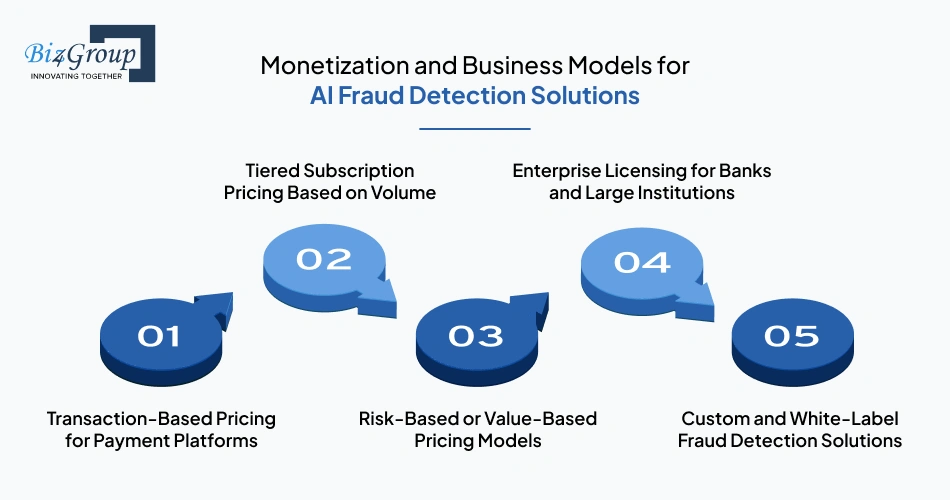

When businesses invest in AI payment fraud detection software development, monetization must match continuous transaction monitoring and real-time risk enforcement. Because fraud systems operate on every payment, pricing models work best when tied to ongoing transaction volume and risk exposure.

Many fraud detection solutions use transaction-based pricing, especially when they protect high-volume payment flows. Businesses pay based on the number of transactions evaluated by the fraud system. Pricing is typically influenced by:

This model aligns cost directly with usage, making it suitable for platforms with fluctuating or seasonal transaction activity.

Some providers offer tiered subscription plans tied to transaction limits. Organizations pay a fixed monthly or annual fee for predefined processing thresholds. Subscription tiers are usually shaped by:

This approach provides predictable costs while supporting steady payment operations.

In certain cases, pricing reflects the level of financial risk the system is trusted to manage rather than raw transaction count. Pricing is influenced by:

This model aligns monetization with business impact, particularly for high-value payment environments.

Large banks and regulated payment institutions typically prefer enterprise licensing agreements. Pricing usually depends on:

Enterprise licensing supports long-term deployments and stable fraud operations.

Some organizations require tailored or white-label fraud detection platforms built around specific payment workflows or regulatory constraints. Revenue in these scenarios comes from:

This model suits enterprises with unique risk profiles or compliance-heavy environments.

AI fraud detection solutions monetize successfully when pricing reflects transaction volume, fraud exposure, and operational dependence. Sustainable revenue comes from aligning business models with how teams create AI fraud detection platforms for payments that manage risk continuously, not from generic software pricing assumptions.

Also Read: 65+ Software Ideas for Entrepreneurs and Small Businesses

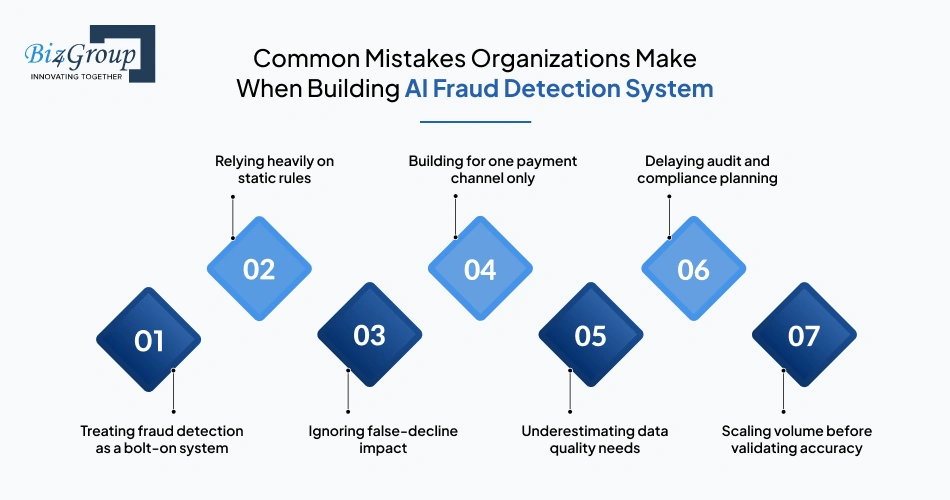

In AI payment fraud detection software development, teams often underestimate how deeply fraud detection must integrate with live payment flows. Small design shortcuts can create accuracy gaps, operational friction, and scalability issues once transaction volumes and fraud pressure increase.

| Common Mistake | How to Avoid It |

|---|---|

|

Treating fraud detection as a bolt-on system |

Design fraud detection as a core payment component that evaluates risk before transaction authorization completes. |

|

Relying heavily on static rules |

Combine rules with behavioral signals that adapt as payment and fraud patterns change. |

|

Ignoring false-decline impact |

Balance fraud prevention with approval optimization to protect legitimate transaction revenue. |

|

Building for one payment channel only |

Ensure detection logic applies consistently across cards, wallets, BNPL, and cross-border payments. |

|

Underestimating data quality needs |

Validate transactions, device, and behavioral data early before building scoring logic. |

|

Delaying audit and compliance planning |

Embed logging and traceability from day one to support regulatory and dispute reviews. |

|

Scaling volume before validating accuracy |

Prove detection performance in live conditions before expanding transaction throughput. |

Avoiding these mistakes helps teams create AI fraud detection platform for payments that remain accurate, compliant, and scalable under real transaction pressure, ensuring fraud prevention strengthens payment performance instead of becoming an operational bottleneck.

Partner with a team that has already fixed them for industry leaders and would do the same (and more) for you.

Talk to Our ExpertsAt Biz4Group LLC, we build secure, scalable payment systems that help businesses operate confidently in high-risk transaction environments. As a USA-based software development company, we support startups, fintech firms, and enterprises in building fraud detection systems that protect revenue and customer trust.

Our expertise lies in combining practical software engineering with real-world payment system knowledge. Across fintech, e-commerce, and regulated digital platforms, we’ve delivered systems that handle live transactions, enforce risk controls, and scale reliably under fraud pressure.

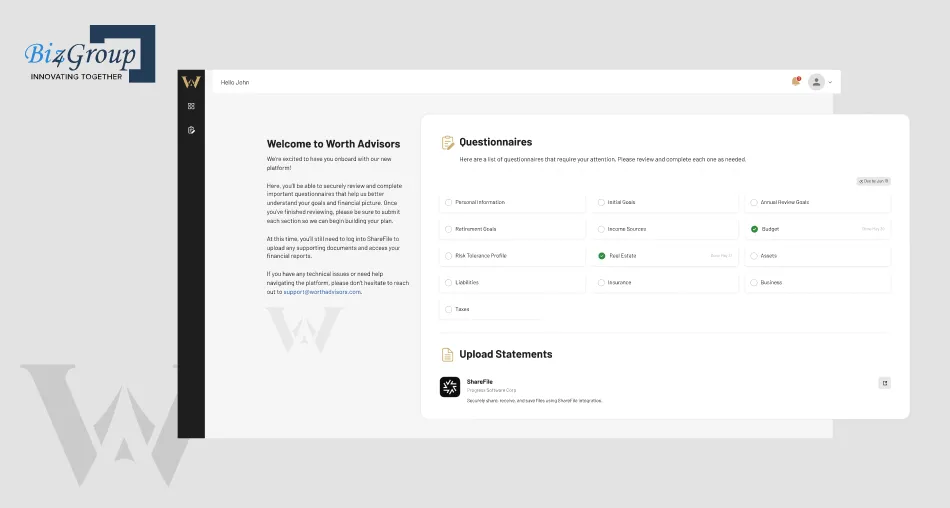

To see how this approach translates into real systems, let's take a look at a platform we’ve already built in a regulated financial environment.

WorthAdvisors: It is a financial planning and advisory platform designed to handle sensitive client data, structured inputs, and complex decision workflows. The system was built around accuracy, traceability, and integrations with external financial tools. These same principles apply when designing payment fraud detection software, where structured data, real-time decisions, and operational reliability directly impact business outcomes.

When it comes to AI payment fraud detection software development, we understand that fraud prevention demands speed, accuracy, and accountability. Thus, every line of code we write reflects that responsibility.

We are a team of builders focused on creating payment fraud detection systems that work reliably in real transaction environments. We have helped U.S.-based businesses reduce fraud risk, protect approvals, and scale securely. If you’re ready to build fraud detection software that performs under pressure and grows with your payments, Biz4Group is ready to help.

Building AI payment fraud detection software is about strengthening the entire payment ecosystem, not just stopping suspicious transactions. From reducing fraud losses and false declines to maintaining compliance and customer trust, the right system helps businesses operate securely at scale as digital payments continue to grow.

The journey from idea to deployment can feel complex. Live transaction flows, risk logic, regulatory expectations, and performance constraints all demand careful planning. But the payoff is clear. A well-built fraud detection system protects revenue, improves approval rates, and allows teams to scale payment volumes without increasing operational overhead. In payments, consistency and speed define long-term success.

At Biz4Group, we deliver custom AI fraud detection development services with the engineering depth expected from a trusted custom software development company, helping banks, fintech firms, and e-commerce platforms build systems that remain accurate, auditable, and scalable as fraud patterns evolve.

If you’re ready to invest in fraud detection software that protects growth and trust, we are ready to partner with you.

AI payment fraud detection software development timelines depend on system scope and transaction complexity. An MVP typically takes 10–14 weeks. However, Biz4Group can deliver an MVP in just 2–3 weeks by using reusable components that significantly reduce development time and cost.

To develop AI payment fraud detection software, teams integrate fraud logic through APIs with gateways and processors. This allows real-time risk evaluation without disrupting authorization, settlement, or reconciliation workflows.

Payment fraud prevention software development with AI analyzes behavioral context alongside transaction data. This approach improves approval accuracy, allowing legitimate payments to pass while still blocking high-risk fraudulent activity.

Yes. Organizations can create AI fraud detection platforms for payments that scale from startups to enterprises. Cloud-based architectures allow fraud controls to grow alongside transaction volume without major infrastructure changes.

An AI payment fraud detection software development cost estimate typically ranges from $40,000 to $300,000+. Cost depends on transaction volume, detection depth, compliance requirements, and long-term scalability needs.

Banks and fintech firms choose custom AI payment fraud detection development services to align detection logic with payment flows, regulatory obligations, and risk tolerance instead of adapting generic fraud tools.

with Biz4Group today!

Our website require some cookies to function properly. Read our privacy policy to know more.