info@biz4group.com

info@biz4group.com

Imagine a digital system that doesn’t wait for instructions but instead, understands your business goals, learns from real-time feedback, and takes independent actions to get the job done.

Read More

Imagine checking out online and not pulling out your card. No long forms, no 16-digit numbers — just a quick “Pay Later” click, and boom, you're done.

That’s the kind of magic Buy Now Pay Later (BNPL) apps like Klarna are pulling off — and guess what? More than a trend, it’s a movement.

According to reports, the global BNPL payment market is expected to grow by 13.7% on annual basis to reach US$560.1 billion in 2025. That’s massive!

If you're a business owner, fintech founder, eCommerce innovator, or even an investor with an eye for disruption, now is your time to act. With the right product strategy, tech stack, and compliance game, you can build a Buy Now Pay Later app that rivals the likes of Klarna, Affirm, or Afterpay, and maybe even outpace them in niche markets.

In this ultimate guide, we’re breaking down:

Basically a step-by-step guide to develop a Buy Now Pay Later app from scratch.

So if you're wondering how to create a Buy Now Pay Later app that’s not just functional but scalable, secure, and profitable — you're exactly where you need to be.

Let’s build something brilliant.

Buy Now Pay Later (BNPL) apps are the fintech world’s version of “treat now, worry later.” These apps let users split their purchases into smaller, manageable payments, often interest-free, while the merchant gets paid upfront.

Think of it like a modern-day installment plan, only smarter, faster, and fully digital.

Here’s how it typically works:

| Component | Function |

|---|---|

|

User Interface |

Simple checkout integration with Pay Later option |

|

Credit Engine |

Soft credit check or AI-based risk assessment |

|

Payment Processor |

Integrates with Stripe, Adyen, or in-house rails |

|

Merchant Portal |

Lets sellers manage transactions, refunds, and analytics |

|

Admin Panel |

Manages fraud detection, dispute resolution, KYC/AML |

|

Repayment System |

Auto-debits user on due dates, sends reminders |

Yes, BNPL is super convenient, but also super addictive (in a good way). And if you're planning to build an app like Klarna, understanding this flow is step one.

Why Should You Build Buy Now Pay Later App in 2025?

Imagine this: your customer is browsing your online store, adds $300 worth of products to their cart, hesitates at checkout… then sees a sleek little button that says, "Buy Now, Pay Later." They click it, make their first payment of just $75, and walk away feeling like they scored a win — no credit card debt, no stress.

Welcome to the Buy Now Pay Later (BNPL) revolution — a movement that’s reshaping how consumers shop and how businesses make money.

And it’s growing fast.

BNPL isn’t just for fashionistas or Gen Z sneakerheads. It’s reshaping transactions across industries.

BNPL increases checkout conversions by removing upfront payment friction.

Popular verticals: Apparel, electronics, home décor, luxury goods, furniture.

BNPL helps patients afford elective or uncovered procedures like:

Enable students to enroll in skill-building programs or certifications without the burden of full upfront payments.

Let travelers split the cost of flights, hotels, and vacation packages, especially popular with millennials.

High adoption in: Booking portals, travel agencies, tourism apps.

Offer flexible payment terms for business users. This is a rising trend in:

Retailers are integrating BNPL at the POS to offer in-store shoppers the same flexible financing — boosting walk-in conversions.

| Benefit | Why It Matters |

|---|---|

|

Increased Conversion Rates |

Shoppers are more likely to complete purchases with flexible payment options. |

|

Boost in AOV (Average Order Value) |

BNPL users tend to spend more per transaction. |

|

Loyalty Through Convenience |

Offering split payments builds repeat usage and brand trust. |

|

Scalable Monetization |

Merchant fees, interest, premium plans — multiple revenue streams. |

|

Appeals to Credit-Wary Consumers |

BNPL is a no-card-needed alternative for digital natives. |

If you’re looking to tap into a high-growth, tech-forward space with clear revenue potential, there’s no better time to develop a Buy Now Pay Later app, especially with the right fintech strategy behind it.

Whether you're validating or scaling, we’ll meet you where you are.

Schedule a Call

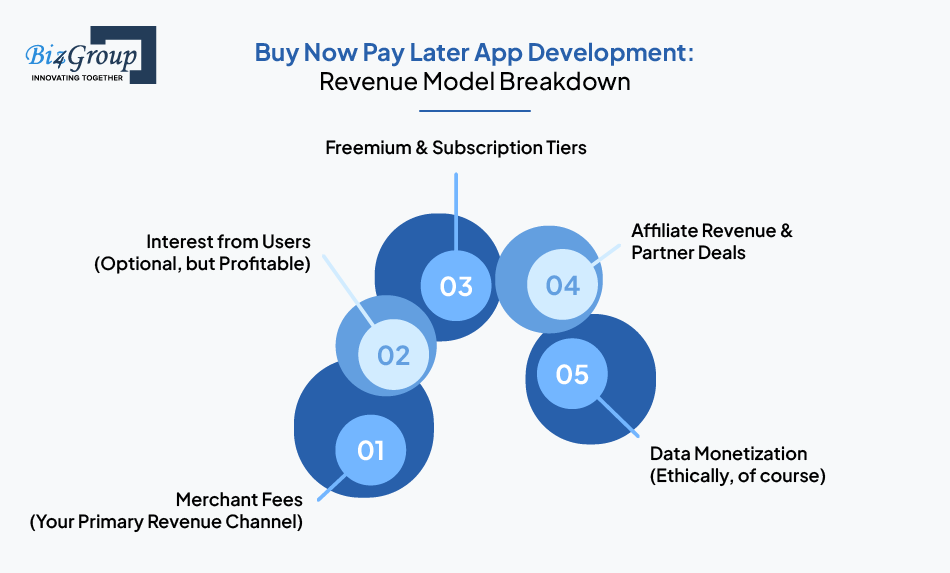

While BNPL apps may seem like financial fairy dust for shoppers, the real magic is in the monetization. Klarna, Affirm, Afterpay — they’re not handing out deferred payments out of goodwill. They’re making serious revenue from a well-orchestrated mix of merchant fees, interest income, and data-backed services.

Here’s how it works — and how you can structure your own revenue model when you build a Buy Now Pay Later app.

Merchants partner with BNPL providers because:

In return, merchants pay a transaction fee, typically:

Klarna generated $1.5B+ in merchant fees alone, making this the primary revenue engine.

Many BNPL models offer:

If you offer longer-term installments, you can:

This opens up recurring revenue and allows you to attract higher-value purchases (think furniture, healthcare, travel).

Some BNPL platforms experiment with:

This adds predictability to your revenue model, especially post-MVP.

BNPL platforms can monetize discovery through:

This turns your app into a shopping discovery engine, not just a payment solution.

If used responsibly and compliantly, anonymized customer data can:

| Monetization Stream | Description | Maturity Stage |

|---|---|---|

|

Late Fees |

Charged when a user misses payment (capped in many regions) |

Short-term |

|

White-Label Licensing |

Offer your BNPL engine as a SaaS tool to other brands |

Post-MVP |

|

Credit-as-a-Service API |

Monetize your scoring model or risk engine |

Growth stage |

Bottom line? When you’re planning Buy Now Pay Later app development, the business model is not just viable — it’s multifaceted, scalable, and investor-friendly.

The key is choosing the right mix of merchant-led revenue, optional user financing, and tech-enabled monetization based on your niche.

Building a Buy Now Pay Later app isn’t just about giving users the illusion of free money — it’s about delivering a seamless, secure, and smart experience that benefits shoppers, merchants, and your bottom line.

The best BNPL platforms like Klarna and Affirm have cracked the formula: mix just enough financial flexibility with slick UX, sprinkle in some fraud protection, and make it all feel effortless.

If you're planning BNPL app development like Klarna, these are the 10 must-have features you can’t afford to miss — unless, of course, you enjoy churn and compliance audits. (No judgment.)

Let’s start with first impressions. A clunky registration process is the digital equivalent of making users fill out a loan application with a quill.

Modern BNPL apps should:

Why it matters: Compliance regulations (like AML laws) require you to verify who’s borrowing money, and users expect it to be fast and intuitive. Bonus points for auto-populating data fields or offering tiered onboarding based on risk level.

Speed is currency. If users need to wait for approval, they’ll bounce faster than your test payment gateway.

A solid BNPL app should:

The engine behind this could leverage credit bureau data, transaction history, or even open banking APIs. This is your conversion gatekeeper — don’t make it a bottleneck.

Building a smarter credit engine? Our AI integration services can help you embed real-time scoring and approval logic with minimal friction.

Whether it’s “Pay in 4” or “Pay monthly over 12 months,” flexibility is the foundation of BNPL.

Your app should offer:

Pro tip: Klarna smartly offers “Pay in 30 days” as a try-before-you-buy tactic — a great way to reduce refund rates and build trust.

Want to break out of the "only-at-partner-stores" bubble? Give users the ability to generate a virtual card they can use anywhere online.

Benefits:

Your system will need to integrate with a card issuer or use embedded finance APIs like Marqeta or Galileo.

Your BNPL platform must be just as user-friendly for merchants. After all, they’re the ones paying you.

The merchant dashboard should:

This makes you a partner in sales growth — not just a payment processor.

Let’s face it — people are crafty. And where there’s credit, there’s risk.

Combat fraud by using:

This isn’t just smart — it’s necessary.

To see how artificial intelligence is transforming digital finance across the board, check out our AI in Fintech: Detailed Overview.

Okay, no one wants to wait 48 hours for a support email to find out when their next installment is due. A smart chatbot can solve that in under 5 seconds, and without the hold music.

Integrating an AI-powered chatbot into your BNPL app transforms the support experience from “ugh” to “oh, that was fast.”

What it should do:

Why it matters:

Want to dive deeper into the power of AI-driven conversations? Read: AI Financial Assistant App Development.

While chatbots handle in-app conversations and support, you still need proactive nudges. Push notifications and email alerts ensure users know when a payment is due, before their bank balance finds out the hard way.

Reminding users of due payments is essential and appreciated. (Unless it’s a text at 3 a.m. Don’t do that.)

Use push notifications, email, or SMS to:

Bonus: Integrate snooze or “remind me later” features to make it feel less aggressive.

Transparency builds trust. Give users:

This is also where they’ll manage settings, linked cards, and account security.

Behind the scenes, your admin panel is the command center.

Admins should be able to:

These features are the pillars of a secure, scalable, and high-performing BNPL platform. Get them right, and you’re building a financial experience users will trust, merchants will love, and investors will believe in.

We turn fintech wishlists into flawless, functional apps — minus the fluff.

Let’s Build It Together

Building a BNPL app isn’t just about slapping a “Pay Later” button onto a checkout screen and calling it fintech. It’s about creating a high-trust, high-tech system that juggles regulations, risk, user experience, and real money — all while trying not to burn through your runway.

Feeling the pressure? Good. That means you care.

Now let’s break it down — step by step.

Start with the “why” and “who.”

Who are you building for — eCommerce stores? Healthcare providers? Millennials who’d rather pay in four than use a credit card?

Research your niche, map competitors like Klarna and Affirm, and identify your edge: is it zero fees? Faster approvals? AI-driven credit scoring? This clarity will shape every decision that follows.

Looking for inspiration from successful BNPL-aligned fintech models? Check out: Build App Like Cleo to see how conversational UX and finance blend seamlessly.

Don’t try to launch with everything under the fintech sun. Your MVP (Minimum Viable Product) should focus on delivering the core BNPL experience:

Save the fancy stuff, like loyalty rewards or AI-powered upselling, for your growth phase.

Need help building a lean prototype? Check out our MVP Development Services.

Nobody wants to feel like they’re applying for a mortgage during checkout.

Design a clean, intuitive interface that builds trust instantly, especially around credit approval, repayment schedules, and balance visibility.

Using interactive prototyping for mobile app development helps you test UX flows before full development.

This isn’t just cosmetic. A seamless experience directly boosts conversion rates and repeat usage.

And yes, custom animations, micro-interactions, and a frictionless layout drive conversions, but they also impact your budget. For a realistic estimate, explore our breakdown of UI/UX Design Cost.

Now your app needs to start doing things. At this stage, plug in the essentials:

If you think “we’ll handle legal later,” you might end up with a lawsuit instead of a launch.

BNPL apps must comply with:

Also, decide early: will you operate under a lending license, or partner with a bank or NBFC?

Move into agile sprints — quick, iterative development cycles that let you test, learn, and optimize.

Focus on:

Go live with a lean version of your app in a controlled market — maybe a single region or pilot group.

Then track what matters:

Let data guide your next move — not assumptions.

P.S. We’re listed among the top-rated MVP development companies for a reason — our clients go to market faster.

Once your MVP works, it’s time to grow and outshine the competition.

You can:

And that’s your roadmap to develop a Buy Now Pay Later app like Klarna — from concept to compliant, scalable reality.

Now, let’s talk money.

So, how much does it actually cost to develop a Buy Now Pay Later app like Klarna?

Well, the short answer is: it depends.

But the long answer? Let’s break it down — with real numbers, real scope, and no sugarcoating.

| Development Stage | Estimated Cost (USD) | Timeline |

|---|---|---|

|

Discovery & Research |

$5,000 – $10,000 |

2–3 weeks |

|

UI/UX Design |

$8,000 – $15,000 |

3–5 weeks |

|

$30,000 – $50,000 |

8–12 weeks |

|

|

Full-Feature Build |

$60,000 – $100,000+ |

4–6 months |

|

Testing & QA |

$5,000 – $10,000 |

Parallel |

|

Compliance & Security |

$10,000 – $25,000 |

Ongoing |

|

Post-Launch Support |

$3,000 – $8,000/month |

Retainer |

Low-End: ~$136,000

High-End: ~$258,000+

This assumes full-feature development and at least 6 months of post-launch support.

For a lean MVP, costs can be significantly lower — roughly $60K–$90K.

The total cost can swing dramatically based on several key factors:

More features = more hours = more budget. Credit scoring engines, chatbots, admin portals, and loyalty programs add cost fast.

Launching globally? You’ll need to build compliance logic for each region — GDPR, PCI-DSS, CCPA, CFPB, and more.

Custom builds cost more than plug-and-play integrations. Also, advanced stacks (like microservices, Kafka, container orchestration) impact cloud and devops costs.

Slick, animated, brand-rich interfaces cost more than simple UI kits. But they also pay off in conversions and retention.

Partnering with a professional UI/UX Design Company can make a world of difference in visual appeal and user engagement.

Rates vary globally:

Marketing dashboards, merchant analytics, or dynamic credit limit engines? All part of scaling — and pricing.

If you’re budget-conscious but want to validate fast, start with an MVP that handles:

For more insight into AI-powered finance projects, see our full breakdown of the Cost to Build a Fintech App Using AI.

Launch lean, iterate fast, and impress your investors.

Contact NowYou guessed it right... no one wants to use a Buy Now Pay Later app that crashes at checkout or delays payment processing like it’s 2006. If you want your app to perform like Klarna and scale like Affirm, you need more than a few trendy frameworks. You need a purpose-built tech stack engineered for speed, security, scalability, and financial compliance.

Whether you’re building from scratch or integrating into existing ecosystems, this tech stack is your foundation. Choose wisely — your platform’s future literally depends on it.

| Layer | Tech Stack Options | Why It Works |

|---|---|---|

|

Frontend |

React, Flutter |

Delivers fast, responsive UIs across web and mobile. Flutter’s cross-platform nature cuts dev time. |

|

Backend |

Scalable, developer-friendly, and secure — essential for processing real-time transactions. |

|

|

Database |

PostgreSQL, MongoDB |

PostgreSQL is great for structured financial data. MongoDB offers flexibility for user/session storage. |

|

Cloud Hosting |

AWS, Azure, GCP |

Scalable infrastructure with built-in security, load balancing, and global availability. |

|

DevOps & CI/CD |

Docker, Kubernetes, GitHub Actions, Jenkins |

Enables continuous integration, smooth deployments, and reliable rollback in case of errors. |

|

Cache & Streaming |

Redis, Kafka |

Redis boosts performance. Kafka handles real-time event processing (great for payment triggers and fraud alerts). |

|

Payment & Credit APIs |

Stripe, Adyen, Marqeta, Visa DPS |

Secure and globally accepted for card issuance and merchant transactions. |

|

KYC/AML Tools |

Onfido, Jumio, Trulioo |

For user identity verification and compliance. Easy to integrate via REST APIs. |

|

Notification System |

Firebase Cloud Messaging (FCM), Twilio, SendGrid |

Powers real-time push, SMS, and email alerts — for reminders, confirmations, and receipts. |

If you plan to future-proof your BNPL platform, consider embedding AI for:

TL;DR:

Choosing the best tech stack isn’t about using the hottest tools — it’s about combining speed, security, and scalability in a way that supports user trust and business growth.

And if you’d rather not make those decisions solo?

We’ve helped brands build fintech platforms from idea to scale. We can help you too.

We’ll help you build faster, scale smarter, and never crash on checkout.

Consult with UsIf BNPL apps were just about clever code and slick design, Klarna would have a thousand clones by now. But the truth is: you’re not just building a payment tool — you’re building a digital lender. And with that comes a regulatory microscope.

Whether you’re processing payments, managing identity verification, or holding customer data, your BNPL platform has to comply with financial regulations and security frameworks — or risk fines, shutdowns, or worse: loss of user trust.

Let’s walk through what matters.

Depending on your target region, here are the must-haves:

Handling financial data is like walking through a cybersecurity minefield. A small misstep can destroy your reputation. So, here’s what your app needs:

Learn more about the security risks that occur when developing a mobile app and how to avoid them.

BNPL apps can operate under two models:

Each has pros and cons, and the right choice depends on your scale, market, and speed-to-launch goals.

Users won’t ask you about PCI-DSS, but they will feel it when:

And investors, banks, and partners will absolutely care how airtight your compliance game is.

Security is non-negotiable — and this applies to mobile banking too. To know more, read: 5 Key Steps to Developing a Secure Mobile Banking App.

We speak fluent PCI-DSS, GDPR, and “No Legal Trouble.”

Talk to Our Fintech Experts

You’ve built your app, your backend hums, and the UI is smoother than your morning espresso. But now comes the big question: how do you get real users and merchants to care?

A brilliant BNPL product is only half the battle. The other half? A laser-focused, conversion-obsessed Go-to-Market (GTM) strategy that gets your app in the hands of the right people — fast.

Here’s how to make that happen without burning your runway on ads no one clicks.

BNPL isn’t one-size-fits-all. Klarna speaks to Gen Z fashion lovers. Affirm courts premium shoppers. You need to define:

Start narrow, dominate a niche, and then scale horizontally.

Merchants are your revenue engine, and they care about one thing: sales.

To attract them:

Incentivize early adopters with:

No one likes interest, but everyone likes “split in 4 with no fees.”

To win users:

Trust is currency in fintech. Feature real reviews and showcase your security certifications front and center.

Deploy a lean, high-ROI strategy using these channels:

| Channel | Why It Works |

|---|---|

|

Content Marketing |

Blogs, videos, and explainers drive SEO and educate skeptical users |

|

Paid Ads |

Use paid search + social to target intent-driven users (e.g., “buy now pay later shoes”) |

|

Affiliate Programs |

Partner with shopping blogs or fintech newsletters |

|

Merchant Co-Branding |

Offer “Powered by [Your App]” on merchant sites for viral visibility |

Example: Klarna’s pink branding isn’t subtle — and that’s the point. Create an identity users remember.

Set KPIs from day one:

Track your funnel ruthlessly and iterate fast. If one merchant category underperforms, pivot. If your ad copy flops, rewrite it. Go-To-Market is where survival meets creativity.

Honestly, building a Buy Now Pay Later app like Klarna isn’t all clean code and high fives. You’re dealing with money, risk, compliance, and customer expectations — all in one place.

Here are the most common BNPL app development challenges we’ve seen (and solved), along with what you can do to stay ahead of the curve.

The Problem:

What happens when users miss payments, or worse — never intend to pay? Unpaid installments can quickly erode profit margins and trust in your system.

Smart Solution:

Build a multi-layered risk engine:

The Problem:

Each market has its own regulatory cocktail. GDPR, PCI-DSS, AML, CFPB, CCPA — you name it. Miss one, and you could be looking at fines or app takedowns.

Smart Solution:

“Compliance by design” is the only path forward.

The Problem:

Getting merchants to integrate your BNPL app can feel like convincing someone to switch email providers. It’s sticky and full of friction.

Smart Solution:

Make it effortless.

The Problem:

Your MVP works great with 1,000 users. But what about 100,000?

Smart Solution:

Architect for scale early:

The Problem:

BNPL isn’t universally understood. Miscommunication about fees, due dates, or approvals can tank trust and user retention.

Smart Solution:

Be proactive.

BNPL is a space where first-mover advantage means nothing if your app isn’t smart, secure, and scalable. Solving these challenges head-on, with a clear plan and a seasoned partner, is how you stand out.

Building a Buy Now Pay Later app like Klarna isn’t a weekend side project. You need a team that understands the intersection of finance, compliance, UX, and scale, and actually knows how to ship great products.

That’s where Biz4Group — a trusted Mobile App Development Company — comes in.

In one line? We build solutions that scale and perform.

We're not just coders — we're consultants, architects, and long-term partners who speak both tech and business.

Here’s why businesses across industries trust Biz4Group to build their next big thing:

We’ve successfully delivered 300+ solutions across:

... and so many more.

We know how to balance domain-specific compliance with cutting-edge tech — and make it user-friendly.

When TekChoice, a leading accounting and finance platform, needed a powerful, intuitive frontend for thousands of users — they called us.

TekChoice wanted a modern, user-first interface to match its reputation as a trusted accounting tool. The goal:

All without breaking what was already working under the hood.

We focused on front-end performance, user flows, and interaction logic. Using React and custom RPC logic, we built a sleek dashboard that loads fast and scales easily — while giving users total control over their financial data.

A sleek, responsive web experience that enhanced user engagement, reduced bounce rates, and helped TekChoice position itself as a serious contender in the digital finance space.

Ready to build a Klarna-level BNPL app — with the team that actually knows how?

Let Biz4Group help you go from concept to launch — and beyond.

Buy Now Pay Later is a financial revolution reshaping how consumers shop and how businesses convert. Klarna, Affirm, Afterpay — they’ve all tapped into something powerful: the desire for flexibility, trust, and simplicity.

But here’s the thing…

You don’t have to be Klarna to compete with Klarna.

With the right idea, tech stack, compliance foundation, and go-to-market plan — you can carve out your space in this booming market.

And you don’t have to do it alone.

At Biz4Group, we help ambitious brands build secure, scalable, and user-first fintech solutions — from MVP to full product launches. Whether you're a startup founder with a vision or an enterprise looking to modernize your payments, we’ve got the expertise, the process, and the team to make it happen.

So… ready to build your own BNPL app that users trust — and investors love?

It typically takes 4–6 months to build a robust MVP of a BNPL app, depending on complexity, features, and compliance scope. A fully scaled version with advanced features like AI-based credit scoring or partner APIs may take longer, especially if you’re operating across multiple regions.

Not necessarily. You can either partner with a licensed financial institution (banking-as-a-service model) or pursue a lending license yourself. The first option is faster to launch; the second gives you more control but comes with regulatory complexity.

Yes, and they should be. Most successful BNPL apps offer ready-made plugins or SDKs for platforms like Shopify, Magento, WooCommerce, etc., making integration frictionless for merchants.

The biggest risks involve payment data exposure, identity theft, and fraudulent transactions. That’s why implementing strong encryption, secure authentication, and fraud detection systems is absolutely essential.

Absolutely. Many BNPL platforms start as mobile-first apps, offering virtual cards or in-app payment options. Just ensure your mobile UX is seamless and secure, especially during onboarding and checkout.

Yes, AI can supercharge your BNPL app through real-time credit scoring, fraud detection, user behavior analysis, and personalized offers. It’s one of the smartest ways to reduce default risk while improving the user experience.

with Biz4Group today!

Our website require some cookies to function properly. Read our privacy policy to know more.